Form 990 Schedule I

Introduction

Schedule I, Grants and Other Assistance to Organizations, Governments, and Individuals in the United States focuses on providing information on grants and other forms of assistance provided by tax-exempt organizations to other entities or individuals within the United States. This schedule is crucial for providing transparency regarding charitable giving and community support activities.

In this resource guide, we will learn about the key aspects of Schedule I, from its purpose to filing requirements and commonly asked questions.

Table of Contents

What is Schedule I?

Schedule I, is a supplementary form attached to Form 990, Return of Organization Exempt from Income Tax. It is designed to gather information about grants and other forms of assistance provided by tax-exempt organizations during the tax year to domestic organizations, domestic governments, and domestic individuals.

It focuses specifically on detailing an organization's grantmaking activities and any other financial assistance they offer. This includes cash grants, scholarships, stipends, non-cash contributions, and similar support provided to domestic organizations, governments, and individuals.

Who must file Schedule I?

An organization filing IRS Form 990 must complete Schedule I if they answer "Yes" to either of the following questions on Part IV, Checklist of Required Schedules of the main Form 990:

- Line 21: Made grants or other assistance to domestic charitable organizations

- Line 22: Made grants or other assistance to domestic individuals

Even if an organization is not required to file Form 990, if they choose to do so voluntarily, they must also complete and submit all required schedules, including Schedule I.

Embark on a Smooth Schedule I Filing Journey with TaxZerone

Complete your Schedule I filing requirements with ease!

Schedule I Filing Requirements

All Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) must complete and attach Schedule I

Below, we have provided Schedule I filing requirements for each part.

Part I - General Information on Grants and Assistance

If the organization answered “Yes” on Form 990, Part IV, line 21 or 22, it must complete Part I of Schedule I.

Line 1

Indicate “Yes” or “No” to confirm whether the organization keeps proper records that support the grant amounts given, the eligibility of recipients, and the criteria used to select them.

Line 2

Use Part IV-Supplemental Information to provide a written explanation or additional details related to the organization’s response for line 2.

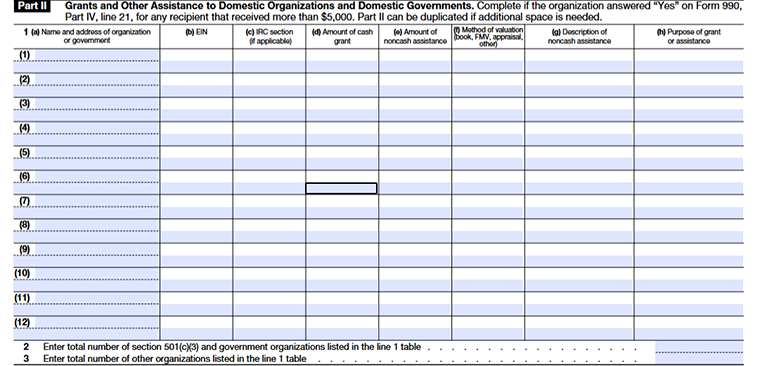

Part II - Grants and Other Assistance to Domestic Organizations and Domestic Governments

Line 1

Complete Line 1 only if the organization answered “Yes” on Form 990, Part IV, line 21, which means it provided more than $5,000 in grants or assistance during the tax year. Report each U.S. organization or government entity that received over $5,000 in total assistance on a separate line in Part II. If more space is needed, attach additional copies of Part II and number for each page. Use Part IV if extra explanation space is required.

Column(a)

Enter the recipient’s full legal name and mailing address.

Column(b)

Provide the recipient’s EIN.

Column(c)

Enter the tax-exempt code section (if applicable) or government entity name; leave blank if neither applies.

Column(d)

Report the total cash grants given during the year.

Column(e)

Enter the total amount of noncash assistance received during the year.

Column(f)

Enter the fair market value of noncash items and explain how the value was determined.

Column(g)

Describe the noncash assistance provided (such as medical supplies, books, or equipment).

Column(h)

Clearly explain the specific purpose or use of the grant or assistance.

Line 2

Add up the number of recipient organizations listed in Schedule I, Part II, line 1 that are IRS-recognized 501(c)(3) tax-exempt organizations, churches or other houses of worship, church-related organizations, or U.S. government entities, and enter the total here.

Line 3

Add the number of recipient organizations listed in Schedule I, Part II, line 1 that don’t fall under the categories reported on line 2. This includes organizations that are not tax-exempt as well as those that are tax-exempt under another section of 501(c) but not 501(c)(3).

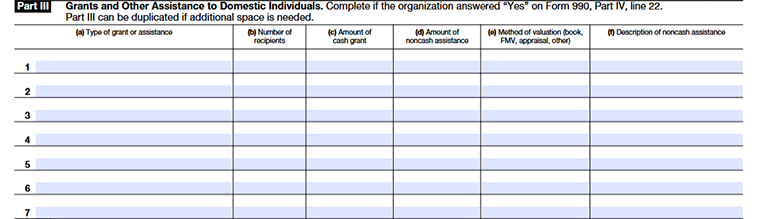

Part III - Grants and Other Assistance to Domestic Individuals

If the organization answered “Yes” on Form 990, Part IV, line 22, it must complete Part III of Schedule I.

A “Yes” response indicates that the organization reported more than $5,000 on Form 990, Part IX, line 2, column (A).

Provide the following details for every individual.

Column(a)

Type of grant or assistance

Column(b)

Number of recipients

Column(c)

Amount of cash grant

Column(d)

Amount of noncash assistance

Column(e)

Method of valuation (book, FMV, appraisal, other)

Column(f)

Description of noncash assistance

Part III can be duplicated if additional space is needed.

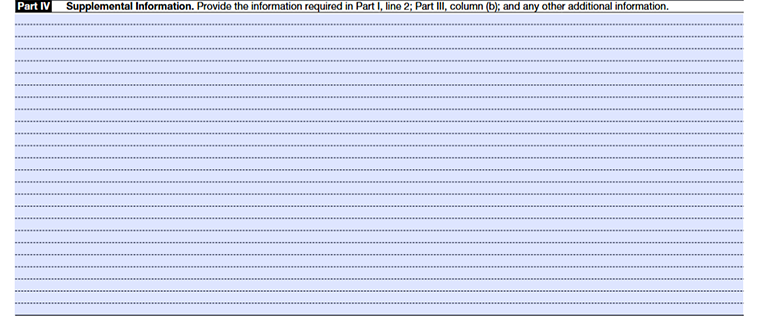

Part IV - Supplemental Information

Schedule I Part IV can be used to provide narrative information required in Part I, line 2, regarding monitoring of funds, and in Part III, column (b), regarding how the organization estimated the number of recipients for each type of grant or assistance.

Also, use Part IV to provide other narrative explanations and descriptions, as needed. Identify the specific part and line(s) that the response supports.

Choose TaxZerone to complete your Schedule I filing

We at TaxZerone help to revolutionize your tax filing experience, making it as simple and stress-free as possible. Our intuitive platform guides you seamlessly through every step of the Form 990 process, making it a seamless experience.

Here’s how your Form 990 return with Schedule I attachment is transmitted to the IRS in 3 simple steps!

- Provide Organization Details - Choose the tax year for which you want to file a return, and provide your organization’s details.

- Preview the Return - Complete Schedule I and preview the information provided in the return for accuracy before transmitting.

- Transmit to the IRS - Transmit Schedule I and your 990 return to the IRS and get the acceptance in just a few hours.

In the unlikely event of an IRS rejection, we'll help you identify and correct any errors in your Form 990 information return, ensuring a swift and cost-free resubmission.

Streamline Your 990 Filing with TaxZerone!

Make your e-filing process simple by clicking the button below.

Commonly Asked Questions

1. What is the purpose of filing Schedule I?

2. What records should be maintained for completing Schedule I?

- Grant application materials and recipient selection processes

- Grant agreements outlining the purpose and allowable uses of the funds

- Documentation of how the use of funds is monitored