Form 990 Schedule N

Introduction

Schedule N is necessary for organizations striving to maintain transparency and compliance with the IRS. It is generally filed by tax-exempt organizations to report going out of existence or disposing of more than 25% of its net assets through sale, exchange, or other disposition.

In this resource guide, we'll delve into the filing purpose of Schedule N, identify the entities required to file, outline the filing requirements, and address common questions.

Table of Contents

What is Schedule N?

Schedule N, Liquidation, Termination, Dissolution, or Significant Disposition of Assets is a supplementary schedule that accompanies the standard Form 990/Form 990-EZ and is filed annually by tax-exempt and nonprofits.

Any organization that files IRS Form 990 or IRS Form 990-EZ and is going out of existence or disposing of more than 25% of its net assets through sale, exchange, or other disposition must complete and attach Schedule E along with their annual information return.

Who must file Schedule N?

Any exempt organization that answered “Yes” to Form 990, Part IV, Checklist of Required Schedules, line 31 or 32, or Form 990-EZ, line 36, must complete and attach Schedule N attachment to Form 990/990-EZ, as applicable.

Choose TaxZerone to complete your Schedule N filing requirements.

Your journey to staying tax-compliant starts here!

Schedule N Filing Requirements

All Section 501(c)(3) organizations that file Form 990/990-EZ must complete and attach Schedule N and their 990-EZ return.

Below, we have provided Schedule N filing requirements for each part.

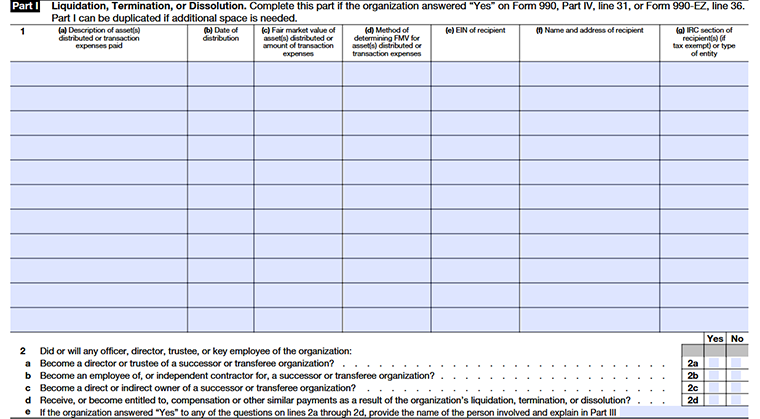

Part I - Liquidation, Termination, or Dissolution

Line 1

List any property, money, or items your organization gave away when it closed, merged, or combined with another group. Include each type of asset, and if you paid for professional services like lawyers or accountants to help with the process, list those expenses too.

Column (a)

Group assets by type and describe them. List big professional fees (over $10,000) separately, like lawyer or accountant fees. Don’t include broker fees here.

Column (b)

Date the asset was given, or the fee was paid.

Column (c)

Enter how much the asset is worth or how much you paid for the professional service. Keep it simple, just the dollar amount.

Column (d)

Explain how you figured out that value.

Column (e & f)

Name, address, and EIN of the recipient. You don’t need to list members individually group them if it’s a membership organization.

Column (g)

The IRS code showing the recipient is tax-exempt (like 501(c)(3)) or notes if it’s a government agency or other type of organization.

Line 2

If any of your current leaders or key staff like officers, directors, trustees, or important employees will have a role in the organization receiving your assets, you need to report it. This includes:

Line 2a

If they are on board or act as trustees.

Line 2b

If they work, there as an employee or contractor.

Line 2c

Own a part of the organization, directly or indirectly.

Line 2d

Receive any payment or benefit because of the transfer, like severance or “change of control” payments.

Line 2e

If the organization answered “Yes” to any of the questions in lines 2a through 2d, list the name of the person involved and provide a brief explanation in Part III.

Line 3

Check “Yes” if your organization gave out its assets exactly the way its own rules say it should.

Line 4a

Check “Yes” if the law requires your organization to tell the state (like the attorney general) that it plans to close or shut down.

Line 4b

Mark “Yes” if the organization let the state know it is closing or ending its operations.

Line 5

Check “Yes” if your organization has paid off all its bills and obligations before closing, following state rules.

Line 6a

Mark “Yes” if your organization had any tax-exempt bonds during the year.

Line 6b

Mark “Yes” if all those bonds were fully paid off, canceled, or otherwise resolved during the year. Leave blank if you don’t have bonds.

Line 6c

If you answered “Yes” on 6b, explain in Part III how the bonds were settled. Include details if anything wasn’t handled according to the law, or if bonds were avoided by transferring assets to another nonprofit including recipient names, bond IDs (CUSIP), and a short description of the arrangement.

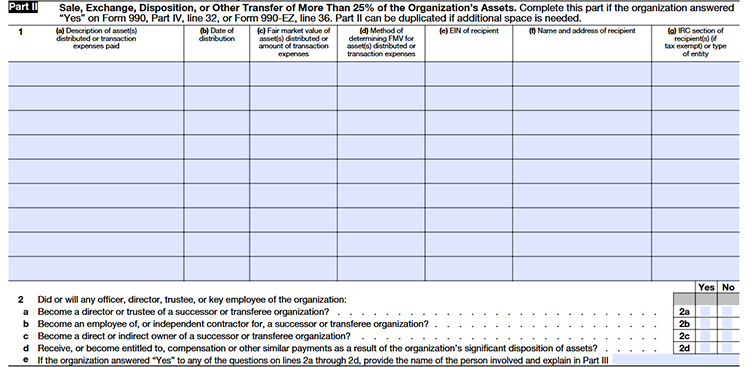

Part II - Sale, Exchange, Disposition, or Other Transfer of More Than 25% of the Organization's Assets

Line 1

- List any property, money, or items your organization gave away when it closed, merged, or combined with another group. Include each type of asset, and if you paid for professional services like lawyers or accountants to help with the process, list those expenses too.

- Line 1, columns (a) through (g) in Part II have already been explained in Part I, so kindly refer to that section for the details.

Line 2

If any of your current leaders or key staff like officers, directors, trustees, or important employees will have a role in the organization receiving your assets, you need to report it. This includes:

Line 2a

If they are on board or act as trustees.

Line 2b

If they work, there as an employee or contractor.

Line 2c

Own a part of the organization, directly or indirectly.

Line 2d

State whether any officer, director, trustee, or key employee received or became eligible to receive compensation or similar payments as a result of the organization’s significant transfer or sale of assets.

Line 2e

If the organization answered “Yes” to any of the questions in lines 2a through 2d, list the name of the person involved and provide a brief explanation in Part III.

- Date of distribution

- The fair market value of the asset(s) distributed or the amount of transaction expenses

- Method of determining FMV for asset distributed or transaction expenses

- EIN of recipient

- Name and address of the recipient

- IRC section of recipient or type of entity

In need of additional space for reporting information, Part II of the schedule can be duplicated based on the requirement.

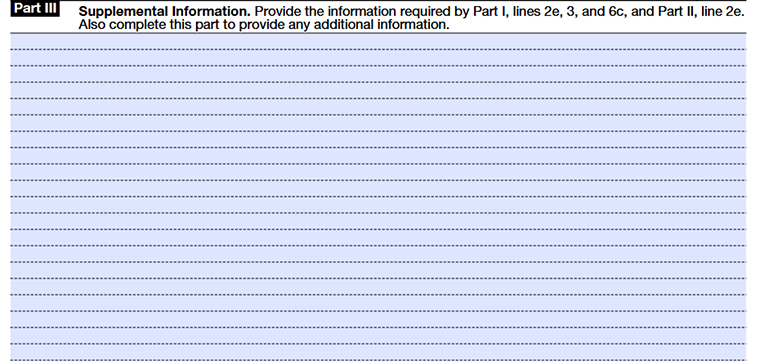

Part III - Supplemental Information

This part can be used by the organization to provide the required explanation on lines 2e, 3, and 6c of Part I, Liquidation, Termination, or Dissolution and line 2e of Part II, Sale, Exchange, Disposition, or Other Transfer of More Than 25% of the Organization’s Assets.

The part can also be duplicated by the 990 and 990-EZ filers if more space is needed to provide additional information.

Choose TaxZerone to complete your Schedule N filing

TaxZerone is an IRS-authorized e-file service provider; meaning you get instant updates on your 990/990-EZ return filing status. We ensure help is available at every step to provide you with an easy e-filing experience!

At TaxZerone, we go beyond just filing – we're here to make your entire experience seamless and stress-free.

Here's how your Form 990/990-EZ return with Schedule N attachment is transmitted to the IRS - just 3 simple steps!

- Provide Organization Details -Choose the tax year for which you want to file a return, and provide your organization's details.

- Preview the Return - Complete Schedule N and preview the information provided in the return for accuracy before transmitting.

- Transmit to the IRS - Transmit Schedule N along with your 990/990-EZ return to the IRS and get the acceptance in just a few hours.

Even if the IRS rejects your exempt information return for any reason, you can correct and retransmit it to the IRS for free!

Ready to attach Schedule N along with your 990/990-EZ return with TaxZerone?

Make the e-filing process simple by clicking the button below.

Commonly Asked Questions

1. What are the two parts of Schedule N?

Schedule N consists of two parts:

- Part I: This part is for organizations that have completely liquidated, terminated, or dissolved and ceased operations during the tax year.

- Part II: This part is for organizations that are still in the process of winding up their affairs at the end of the tax year, but have not yet completely liquidated, terminated, or dissolved and ceased operations.

The schedule also has another part (Supplemental Information) that can be used by the organization to provide additional explanations on questions answered in Parts I and II.