Form 2220, Underpayment of Estimated Tax

by Corporations

Introduction

Form 2220, Underpayment of Estimated Tax by Corporations, is used by corporations, tax-exempt organizations, and private foundations to calculate and report any underpayment of estimated taxes. For corporations that have underestimated their tax liability, Form 2220 is necessary to determine if a penalty is due.

In this resource guide, we aim to brief on Form 2220, providing valuable insights into its purpose, the entities obligated to file, the filing requirements, and addressing common queries.

Table of Contents

What is Form 2220?

Form 2220 is a tax form used to calculate any underpayment of estimated tax by corporations. Corporations are required to pay their taxes throughout the year in quarterly installments. If these payments are not made on time or in the correct amounts, an underpayment penalty may apply, and Form 2220 helps determine the amount of this penalty.

This form is commonly used with Form 990-T, which tax-exempt organizations file to report unrelated business taxable income, and Form 990-PF, which private foundations file to report their annual financial activity.

Who must file Form 2220?

Corporations, tax-exempt organizations, and private foundations that underpay their estimated taxes are required to file Form 2220. This includes:

- Corporations: Any corporation that did not pay enough estimated tax throughout the year must file Form 2220 to calculate the underpayment penalty.

- Tax-Exempt Organizations: Organizations that file Form 990-T to report unrelated business taxable income (UBTI) and fail to make timely estimated tax payments must file Form 2220 to compute the penalty for underpayment.

- Private Foundations: Foundations that file Form 990-PF must also use Form 2220 if they underpay their estimated tax obligations.

Corporations or organizations may not need to file the form if they qualify for an exception to the penalty, such as meeting the safe harbor rule or if their total tax liability is below a certain threshold.

Choose TaxZerone for a seamless e-filing experience and stay compliant with the IRS.

Your journey to stress-free tax filing starts here!

How to file Form 2220?

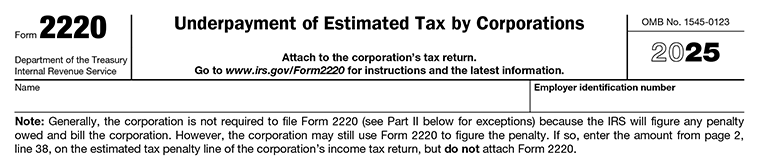

Form 2220, Underpayment of Estimated Tax by Corporations contains the organization’s basic identification details and an important IRS filing note.

Name

Enter the legal name of the corporation or exempt organization exactly as shown on the related tax return, such as IRS Form 990-T or 990-PF.

Employer Identification Number (EIN)

Enter the organization’s 9-digit EIN used for IRS tax filings. The EIN on Form 2220 should match the EIN entered on the related return.

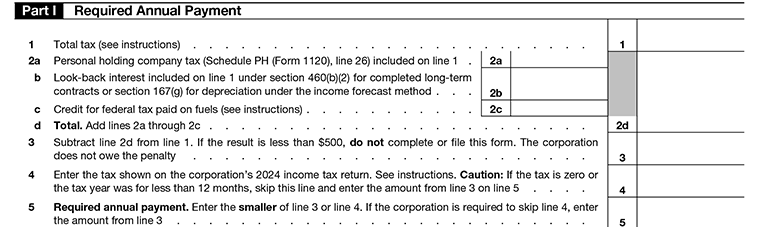

Part I-Required Annual Payment

Line 1

- Organizations filing Form 990-T should generally enter the total tax amount from the applicable tax return line used to report income tax liability. If the reported tax includes Corporate Alternative Minimum Tax (CAMT), do not include the CAMT amount on line 1 of Form 2220. Instead, write “CAMT” and show the amount in brackets on the dotted line beside line 1.

- For exempt organizations and other entities, refer to the applicable return instructions, including Form 990-T and Form 990-PF, to determine the correct total tax amount for estimated tax purposes.

Line 2a

Enter any personal holding company tax included in line 1. Use the amount reported on Schedule PH (Form 1120), line 26.

Line 2b

Enter any look-back interest included in line 1 under section 460(b)(2) for completed long-term contracts or under section 167(g) for depreciation calculated using the income forecast method.

Line 2c

Enter the Corporate Alternative Minimum Tax (CAMT) amount reported on the applicable income tax return, including Form 990-T.

Line 2d

Add the amounts from lines 2a through 2c and enter the total on line 2d.

Line 3

Subtract line 2d from line 1. If the result is less than $500, the organization is not required to complete or file Form 2220 because no underpayment penalty applies.

Line 4

Enter the tax reported on the organization’s 2024 income tax return, figured in the same manner as line 3. For Form 990-T filers, use the applicable tax amount from the prior-year return.

Line 5

Enter the smaller of line 3 or line 4 as the required annual payment. If line 4 was skipped, enter the amount from line 3.

Part II-Reasons for Filing

Line 6

Check this box if the organization is using the adjusted seasonal installment method to calculate estimated tax payments. This method may help reduce underpayment penalties when income is earned unevenly during the year.

Line 7

Check this box if the organization is using the annualized income installment method to calculate estimated tax payments based on income earned during specific periods of the year.

Line 8

Check this box if the organization qualifies as a large corporation and is calculating its first required installment using the prior year’s tax amount. Generally, a large corporation is one that had a taxable income of $1 million or more during any of the previous three tax years.

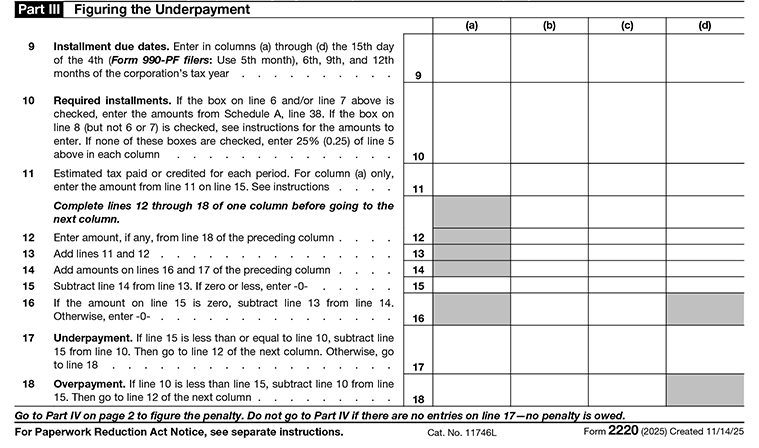

Part III-Figuring the Underpayment

Line 9

Enter the installment due dates for the organization’s tax year. Generally, estimated tax installments are due on the 15th day of the 4th, 6th, 9th, and 12th months of the tax year. Form 990-PF filers should use the 5th month instead of the 4th month for the first installment.

Line 10

- Enter the organization’s required installment amounts. If the adjusted seasonal installment method or annualized income installment method is used, enter the amounts from Schedule A, line 38.

- Large corporations may have special calculation rules for determining installment amounts based on the prior year’s tax liability.

Line 11

Enter all estimated tax payments made for the tax year, including any overpayment from the prior year’s return that was applied to the current year’s estimated tax.

- In column (a), include payments made by the first installment due date.

- In columns (b), (c), and (d), include payments made between the due dates for each installment period.

If a due date falls on a weekend or legal holiday, payments made on the next business day are treated as timely.

Line 12

Enter any overpayment amount from line 18 of the previous column.

Line 13

Add the amounts from lines 11 and 12 and enter the total.

Line 14

Enter the combined total of lines 16 and 17 from the previous column.

Line 15

Subtract line 14 from line 13. If the result is zero or less, enter “0.”

Line 16

If line 15 is zero, subtract line 13 from line 14 and enter the result. Otherwise, enter “0.”

Line 17

If any column in line 17 shows an underpayment amount, complete Part IV to calculate the underpayment penalty.

Line 18

If line 15 is greater than line 10, subtract line 10 from line 15 and enter the overpayment amount. Carry this amount to line 12 of the next column.

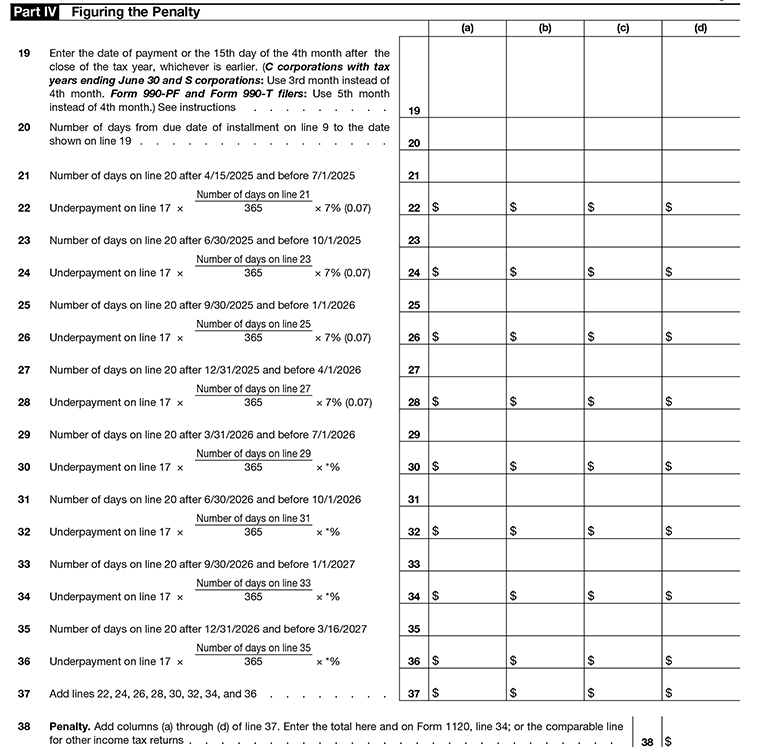

Part IV-Figuring the Penalty

Line 19

Enter the earliest of either the payment date or the 15th day of the fourth month of the following year from the close of the tax year. Special rules apply to certain filers.

- C corporations with tax years ending June 30 and

- S corporations use the 3rd month instead of the 4th month.

- Form 990-T and Form 990-PF filers use the 5th month after the end of the tax year.

Line 20

Enter the number of days from the installment due date shown on line 9 to the ending date entered on line 19.

Line 21

Enter the number of days in line 20 that fall after 4/15/2025 and before 7/1/2025.

Line 22

Calculate the penalty for the period shown on line 21 using the applicable IRS underpayment interest rate.

Line 23

Enter the number of days in line 20 that fall after 6/30/2025 and before 10/1/2025.

Line 24

Calculate the penalty for the period shown on line 23 using the applicable IRS interest rate.

Line 25

Enter the number of days in line 20 that fall after 9/30/2025 and before 1/1/2026.

Line 26

Calculate the penalty for the period shown on line 25 using the applicable IRS interest rate.

Line 27

Enter the number of days in line 20 that fall after 12/31/2025 and before 4/1/2026.

Line 28

Calculate the penalty for the period shown on line 27 using the applicable IRS interest rate.

Line 29

Enter the number of days in line 20 that fall after 3/31/2026 and before 7/1/2026.

Line 30

Calculate the penalty for the period shown on line 29 using the applicable IRS interest rate.

Line 31

Enter the number of days in line 20 that fall after 6/30/2026 and before 10/1/2026.

Line 32

Calculate the penalty for the period shown on line 31 using the applicable IRS interest rate.

Line 33

Enter the number of days in line 20 that fall after 9/30/2026 and before 1/1/2

Line 34

Calculate the penalty for the period shown on line 33 using the applicable IRS interest rate.

Line 35

Enter the number of days in line 20 that fall after 12/31/2026 and before 3/16/2027.

Line 36

Calculate the penalty for the period shown on line 35 using the applicable IRS interest rate.

Line 37

Add the penalty amounts from lines 22, 24, 26, 28, 30, 32, 34, and 36.

Line 38

Enter the total penalty amount from line 37. Report this amount on the applicable penalty line of the organization’s return, such as Form 990-T or Form 990-PF.

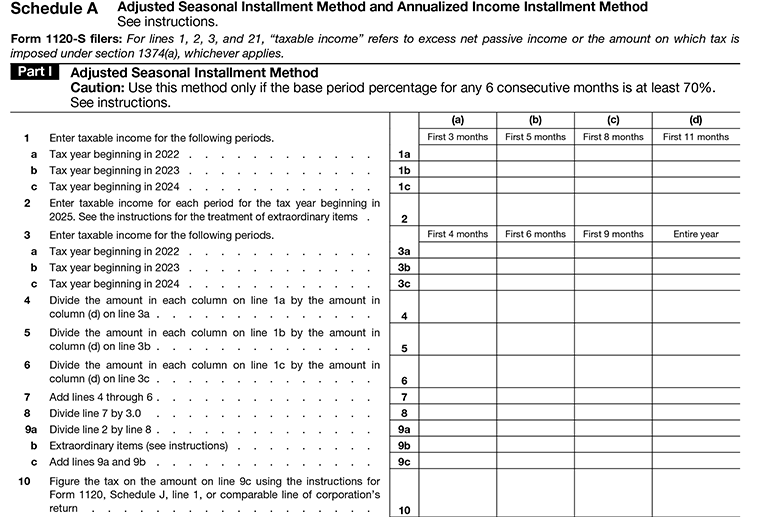

Schedule A-Adjusted Seasonal Installment Method and Annualized Income Installment Method

Part I-Adjusted Seasonal Installment Method

A business entity is eligible to make use of this adjustment only when the six consecutive months base-period percentage is 70 percent or more in relation to the tax year. The base-period percentage of six consecutive months is calculated based on the average of the percentages of taxable incomes in those six months over the last three tax years.

The seasonal installment method is often favorable for businesses with seasonal revenues. This is because this adjustment will help decrease penalties for underpayment of taxes.

Line 1a–1c

Enter the organization’s taxable income for the specified periods for each tax year beginning in 2022, 2023, and 2024. Use the income amounts for the first 3, 5, 8, and 11 months of each tax year.

Line 2

If the organization has extraordinary items, special calculation rules may apply. Do not include any de minimis items that are reported on line 9b.

Line 3a–3c

Enter the organization’s taxable income for the specified periods for tax years beginning in 2022, 2023, and 2024. Use the income amounts for the first 4, 6, and 9 months, and for the entire tax year.

Line 4

Divide each amount entered on line 1a by the amount in column (d) of line 3a and enter the results in the applicable columns.

Line 5

Divide each amount entered on line 1b by the amount in column (d) of line 3b and enter the results in the applicable columns.

Line 6

Divide each amount entered on line 1c by the amount in column (d) of line 3c and enter the results in the applicable columns.

Line 7

Add the amounts from lines 4 through 6 and enter the total for each column.

Line 8

Divide the amount on line 7 by 3 and enter the result.

Line 9b

Enter any extraordinary items, net operating loss deductions, or section 481(a) adjustments for the applicable period. Also include any de minimis items the organization chooses to exclude from line 2.

Line 10

Figure the tax on the amount entered on line 9c using the applicable tax calculation instructions for the organization’s return, such as Form 990-T or Form 990-PF.

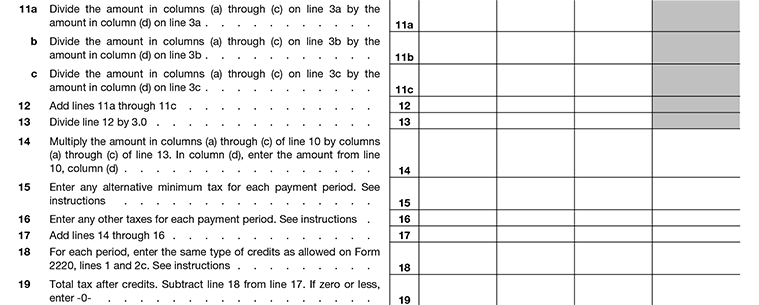

Line 11a

Divide the amounts in columns (a) through (c) on line 3a by the amount in column (d) on line 3a.

Line 11b

Divide the amounts in columns (a) through (c) on line 3b by the amount in column (d) on line 3b.

Line 11c

Divide the amounts in columns (a) through (c) on line 3c by the amount in column (d) on line 3c.

Line 12

Add the amounts from lines 11a through 11c for each column.

Line 13

Divide the amount on line 12 by 3 and enter the result.

Line 14

Multiply the amount in each column of line 10 by the corresponding amount on line 13. In column (d), enter the amount from line 10, column (d).

Line 15

Enter any alternative minimum tax (AMT) for each payment period, if applicable. Form 990-T trust filers should calculate AMT using Schedule I (Form 1041).

Line 16

Enter any other taxes owed for each payment period. Include the same taxes used to calculate Form 2220, Part I, line 1, such as base erosion minimum tax, if applicable.

Line 17

Add the amounts from lines 14 through 16 and enter the total.

Line 18

Enter the credits allowed for each payment period. Use the same types of credits reported on Form 2220, Part I, lines 1 and 2c.

Line 19

Subtract line 18 from line 17. If the result is zero or less, enter “0.”

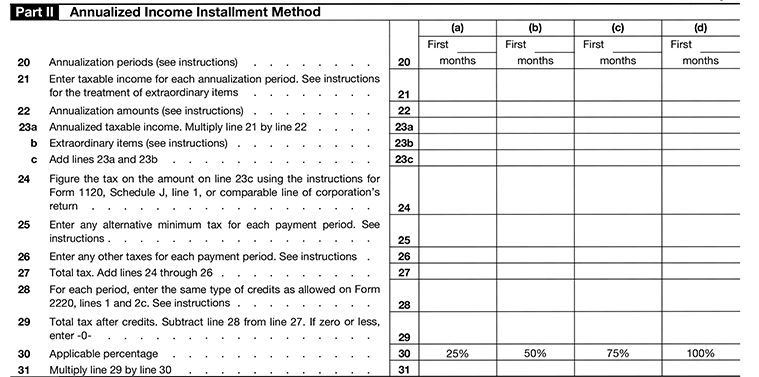

Part II-Annualized Income Installment Method

Line 20

Enter the annualization periods for columns (a) through(d) based on the option selected in the Form 2220 instructions. For example, organizations using Option 1 should enter 2, 4, 7, and 10 in columns (a) through (d).

Line 21

Enter the taxable income received during each annualization period listed on line 20. Do not include de minimis extraordinary items that will be reported on line 23b.

Line 22

Enter the annualization amounts for each column based on the option used for line 20, as provided in the Form 2220 instructions.

Line 23a

Multiply the taxable income on line 21 by the annualization amount on line 22.

Line 23b

Enter any extraordinary items, net operating loss deductions, or section 481(a) adjustments applicable to the annualization period. Also include any de minimis extraordinary items excluded from line 21.

Line 23c

Add lines 23a and 23b and enter the total.

Line 24

Figure the tax on the amount entered on line 23c using the applicable tax instructions for the organization’s return, such as Form 990-T or Form 990-PF.

Line 25

Enter any alternative minimum tax (AMT) for each annualization period, if applicable. Form 990-T trust filers should calculate AMT using Schedule I (Form 1041).

Line 26

Enter any other taxes owed for each annualization period. Include the same taxes used to calculate Form 2220, Part I, line 1, such as base erosion minimum tax, if applicable.

Line 27

Add the amounts from lines 24 through 26 and enter the total tax.

Line 28

Enter the credits allowed for each annualization period. Do not annualize the credits themselves, but annualize any income or deductions used to calculate those credits.

Line 29

Subtract line 28 from line 27. If the result is zero or less, enter “0.”

Line 30

Enter the applicable percentage for each installment period.

Line 31

Multiply line 29 by line 30 and enter the result.

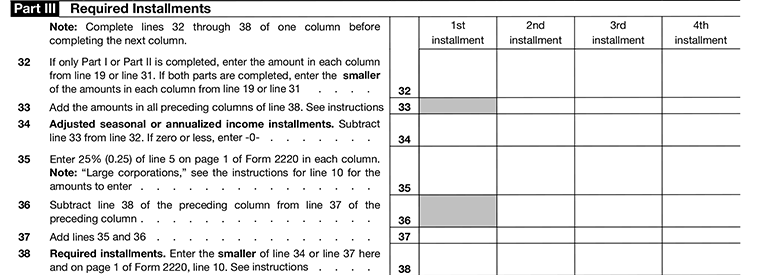

Part III-Required Installments

Line 32

If only Part I or Part II was completed, enter the amount from line 19 or line 31 for each column. If both parts were completed, enter the smaller amount from line 19 or line 31.

Line 33

Add the amounts from all previous columns of line 38 before completing the current column.

Line 34

Subtract line 33 from line 32. If the result is zero or less, enter “0.”

Line 35

Enter 25% of the amount from Form 2220, page 1, line 5, in each column. Large corporations may need to use special rules when figuring this amount.

Line 36

Subtract line 38 of the previous column from line 37 of the previous column.

Line 37

Add lines 35 and 36 and enter the total.

Line 38

Enter the smaller of line 34 or line 37 as the required installment amount. Also enter this amount on Form 2220, page 1, line 10.

Embrace the Future of Tax Filing – Choose TaxZerone Today!

Make your e-filing process simple by clicking the button below.

Start E-filing NowCommonly Asked Questions

1. When is a tax-exempt organization required to file Form 2220?

Tax-exempt organizations that file Form 990-T to report unrelated business income must file

Form 2220 if they underpay their estimated taxes. This form helps calculate the penalty for any underpayment of taxes related to unrelated business income.

2. How do estimated tax payments work for corporations and tax-exempt organizations?

Corporations and tax-exempt organizations are required to make quarterly estimated tax payments throughout the year. If these payments are not made on time or in the correct amount, the IRS may impose an underpayment penalty, which is calculated using Form 2220.