Form 3468 Investment Credit

Introduction

Form 3468, Investment Credit, allows businesses and tax-exempt organizations to claim credits for certain qualifying investments, including those in renewable energy, rehabilitation, and historic preservation projects. This form allows you to claim investment credits that may reduce your UBIT liability.

For tax-exempt organizations filing 990-T, investment tax credits are first calculated using Form 3468, reported through Form 3800, and can ultimately be used to offset unrelated business income tax (UBIT). When filed alongside Form 990-T, this form supports organizations and businesses in maximizing their tax benefits while encouraging investments in socially and economically beneficial projects.

In this resource guide, we'll delve into the filing purpose of Form 3468, identify the entities required to file, who must file, and address common questions.

What’s New in Form 3468

The latest updates to Form 3468 mainly introduce new compliance steps and some changes to how certain credits work. A key update is the addition of Form 7220, which is now required if you’re claiming a higher credit amount under Sections 48, 48C, or 48E by meeting prevailing wage and apprenticeship (PWA) rules. You’ll need to file this form separately for each project.

There are also small updates to Part I, including new fields like a DOE control number. On the credit side, the advanced manufacturing credit (Part IV) now allows up to 35% for certain investments, while the clean electricity (Part V) and energy credit (Part VI) have added restrictions, especially related to foreign entities and some energy properties. In addition, the transition rule for the rehabilitation credit (Part VII) has been removed.

Table of Contents

What is Form 3468?

Form 3468 is used to claim a credit for each investment property and any unused investment credit amount from cooperatives. The purpose of the form is to help taxpayers offset the cost of qualified investments through tax credits, thereby reducing their overall tax liability.

These credits can be claimed for various investments, such as energy property, new equipment, and qualified rehabilitation expenditures. They not only reduce tax liability but also encourage businesses and organizations to invest in sustainable and economically positive initiatives.

Who must file Form 3468?

Generally, any organization that is subject to UBIT and has claimed investment credits must file Form 3468. This includes

- Businesses and Organizations: Entities that invest in qualifying rehabilitation, renewable energy, or advanced energy projects.

- Tax-Exempt Organizations with UBIT: Tax-exempt organizations filing Form 990-T can file Form 3468 if they have unrelated business income and meet the requirements for investment credits.

- Partnerships and Corporations: Partnerships, S-corporations, and corporations investing in qualifying projects must file Form 3468 to claim their investment credits.

Choose TaxZerone to complete your Form 4562 filing requirements.

Your journey to staying tax-compliant starts here!

How to file Form 3468

When completing Form 3468, the top section requires basic identification details to link the form with your main tax return.

- Name(s) shown on return

Enter the exact name as it appears on your primary tax return. This could be your individual name, business name, or organization name. The name must match your main filing to ensure proper processing. - Identifying number

Enter your tax identification number such as an SSN for individuals or an EIN for businesses and tax-exempt organizations. This number is used by the IRS to correctly associate the form with your account.

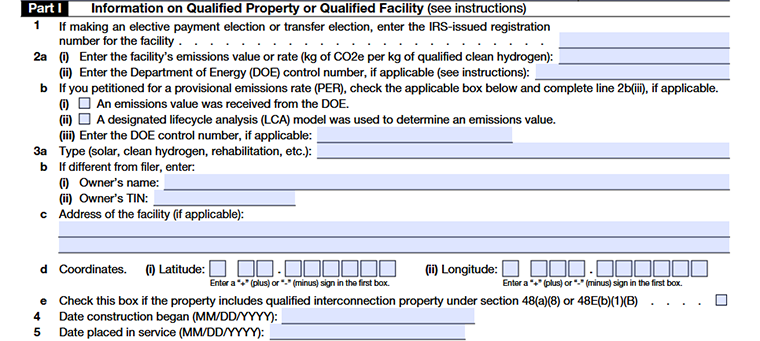

Part I-Information on Qualified Property or Qualified Facility

Line 1

- Enter the IRS-issued registration number for the facility or property received through the pre-filing registration process, required under Sections 48D, 6417, or 6418.

- For Part IV, enter the registration number of the facility if you are the owner, or the qualified investment if you are not the owner.

Line 2a(i)

Enter the emissions rate of the facility (kg of CO₂e per kg of hydrogen produced).

Line 2a(ii)

Enter the DOE control number received from the Department of Energy

Line 2b(i)

Check this box if you receive an emissions value from the Department of Energy (DOE).

Line 2b(ii)

Check this box if you used an IRS-approved Lifecycle Analysis (LCA) model to determine the emissions value.

Line 2b(iii)

Enter the DOE control number, to support your emissions data.

Line 3a

- Enter the type of facility or property for which you are claiming the credit (for example, solar, clean hydrogen, or rehabilitation).

- If you received unused credits from a cooperative, enter: “Unused Investment Credit from Cooperatives.”

Line 3b

If the owner of the facility is different from the filer,provide the following details:

- Enter Owner’s name

- Enter Owner’s taxpayer identification number (TIN)

Line 3c

Enter the address of the facility or property, if applicable.

Line 3d

Provide the location coordinates of the facility ie., Latitude and Longitude.

Line 3e

Check this box if the project includes qualified interconnection property under Sections 48(a)(8) or 48E(b)(1)(B).

Line 4

Enter the date when construction of the facility or property started. This helps determine eligibility for certain credits.

Line 5

Enter the date when the facility or property was ready and available for use. This is important for calculating and claiming the credit.

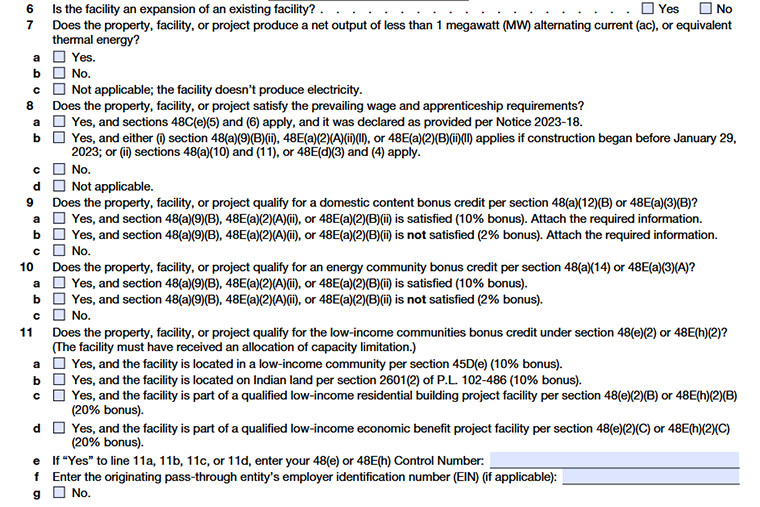

Line 6

- Indicate whether the facility is an expansion of an existing facility.

- Select “Yes” if the project adds to or upgrades an existing setup; otherwise, select “No.”

Line 7

Indicate whether the facility produces electricity.

- If “Yes” Select if the facility generates electricity.

- If “No” Select if the facility does not generate electricity.

- If “not applicable” Select if this question does not apply to your facility or project.

Line 8

Indicate whether your project meets the prevailing wage and apprenticeship requirements, which determine eligibility for the increased credit amount.

Line 8a

- In Special allocation cases select “Yes” if PWA requirements are met and specific rules under sections 48C(e)(5) and (6) apply, including allocations declared under IRS guidance (such as Notice 2023-18).

Line 8b

- For General compliance select “Yes” if PWA requirements are met under general rules, either because:

- If construction began before January 29, 2023, or

- The project complies with applicable PWA provisions under Sections 48(a)(10) and (11), or 48E(d)(3) and (4).

Line 8c

Select “No” if the project does not meet PWA requirements (only the base credit may apply).

Line 8d

Select “Not applicable” if PWA requirements do not apply to your project.

Line 9

This section helps you establish whether your project qualifies for an increased credit amount or adjustment through particular eligibility criteria.

Line 9a

If your project complies with the eligibility criteria under sections 48 and 48E and qualifies for the bonus credit of 10%, check here.

Line 9b

Select this if your project qualifies for a reduced 2% bonus credit but does not fully meet the required conditions. Supporting documents must still be attached.

Line 9c

Select "No” if your project does not qualify for any bonus credit under these provisions.

Line 10

Indicate whether your project qualifies for any additional bonus credit based on specific eligibility criteria

Line 10a

Check this if your project meets the requirements under Section 48(a)(9)(B), Section 48E(a)(2)(A)(ii), or Section 48E(a)(2)(B)(ii) to qualify for the full 10% bonus credit.

Line 10b

Check this if your project qualifies under the same sections—Section 48(a)(9)(B), Section 48E(a)(2)(A)(ii), or Section 48E(a)(2)(B)(ii)—but does not fully meet the conditions, resulting in a reduced 2% bonus credit.

Line 10c

Select this if your project does not meet the requirements under these sections and is not eligible for any bonus credit.

Line 11

- Indicate whether the property, facility, or project qualifies for the low-income communities bonus credit under Section 48(e)(2) or Section 48E(h)(2).

- This applies only if the project has received an official capacity limitation allocation.

Line 11a

Select this if the facility is located in a low-income community as defined under Section 45D(e). This qualifies for a 10% bonus credit.

Line 11b

Select this if the facility is located on Indian land, as defined under Section 2601(2) of Public Law 102-486. This also qualifies for a 10% bonus credit.

Line 11c

Select this if the facility is part of a qualified low-income residential building project under Section 48(e)(2)(B) or Section 48E(h)(2)(B). This qualifies for a 20% bonus credit.

Line 11d

Select this if the facility is part of a qualified low-income economic benefit project under Section 48(e)(2)(C) or Section 48E(h)(2)(C). This qualifies for a 20% bonus credit.

Line 11e

If you selected “Yes” for any of the above (11a–11d), enter your Section 48(e) or 48E(h) control number received for the allocation.

Line 11f

Enter the EIN of the originating pass-through entity, if the credit is being claimed through another entity

Line 11g

Select this if the project does not qualify for the low-income community's bonus credit under these sections.

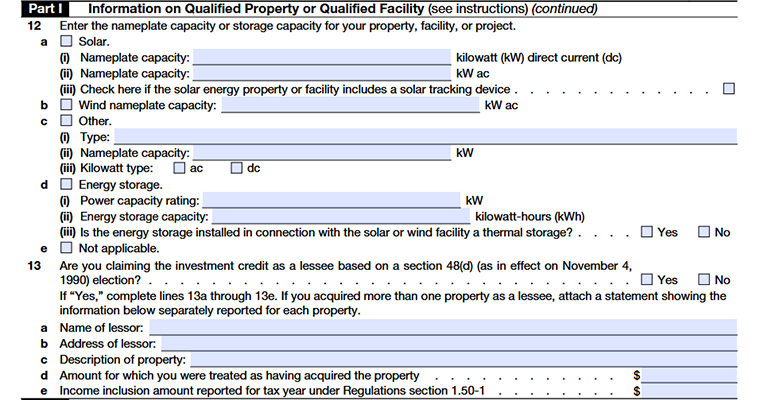

Line 12

Provide the capacity details of your facility, depending on the type of property.

Line 12a(i)

Enter the nameplate capacity in kilowatts (kW) measured in direct current (DC).

Line 12a(ii)

Enter the nameplate capacity in kilowatts (kW) measured in alternating current (AC).

Line 12a(iii)

Check the box if the solar property includes a solar tracking device.

Line 12b

Enter the nameplate capacity in kilowatts (kW) for the wind facility typically measured in AC.

Line 12c(i)

Specify the type of property (if it is not solar or wind).

Line 12c(ii)

Enter the nameplate capacity in kilowatts (kW).

Line 12c(iii)

Check whether the capacity is measured in AC or DC by selecting the appropriate option.

Line 12d(i)

Enter the power capacity rating in kilowatts (kW).

Line 12d(ii)

Enter the energy storage capacity in kilowatt-hours (kWh)

Line 12d(iii)

Check whether the storage system is installed with a solar or wind facility as thermal storage by selecting “Yes” or “No.”

Line 13

Indicate whether you are claiming the investment credit as a lessee under Section 48(d).

- Select “Yes” if the lessor has passed the credit to you, then complete Lines 13a-13e. If you have multiple leased properties, provide details separately for each.

- Select “No” if not applicable.

Line 13a

Enter the full name of the lessor (owner of the property).

Line 13b

Enter the lessor’s business address.

Line 13c

Provide a short description of the leased property.

Line 13d

Enter the amount considered as the purchase value for calculating the credit.

Line 13e

Enter the income the lessor must report related to passing the credit to you.

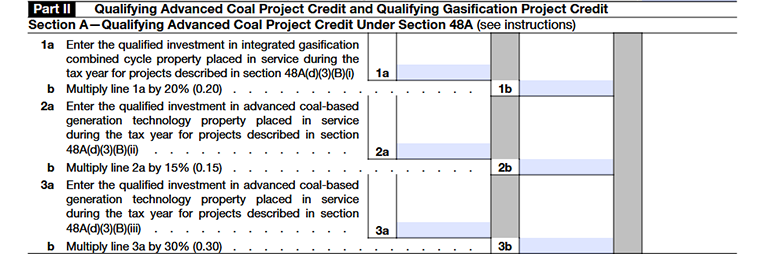

Part II-Qualifying Advanced Coal Project Credit and Qualifying Gasification Project Credit

Section A-Qualifying Advanced Coal Project Credit Under Section 48A

Line 1a

Enter the qualified investment amount for projects using integrated gasification combined cycle technology under Section 48A(d)(3)(B)(i). This includes property used to convert coal into gas for electricity generation.

Line 1b

Multiply the amount on Line 1a by 20% (0.20) to calculate the credit amount.

Line 2a

Enter the qualified investment amount for advanced coal-based generation projects under Section 48A(d)(3)(B)(ii) that do not use gasification technology.

Line 2b

Calculate the credit amount by multiplying the figure from Line 2a by 15 percent (0.15).

Line 3a

Enter the investment amount that qualifies for projects covered under Section 48A(d)(3)(B)(iii), which incorporates carbon capture equipment to limit greenhouse gas emissions (generally 65 percent or more).

Line 3b

The credit amount is calculated by multiplying the figure from Line 3a by 30 percent (0.30).

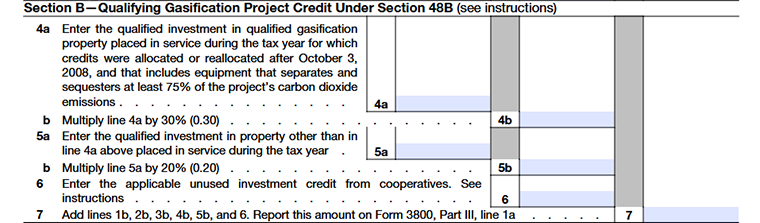

Section B-Qualifying Gasification Project Credit Under Section 48B

Line 4a

- Enter the qualified investment amount in qualifying gasification project property placed in service in the tax year under Section 48B.

- The property must be related to gasification technology capable of separating and capturing no less than 75 percent of carbon dioxide (CO2) emissions.

Line 4b

Calculate the credit amount by multiplying the amount entered in Line 4a by 30 percent (0.30) in relation to the qualifying gasification project under Section 48B.

Line 5a

Enter the qualified investment amount in qualifying gasification project property placed in service during the tax year, except for any amount included in Line 4a.

Line 5b

Multiply the amount on Line 5a by 20% (0.20) to calculate the credit amount.

Line 6

- If you are a patron of a cooperative, enter any unused investment credit allocated to you from a qualifying advanced coal project or gasification project.

- If you are a cooperative, follow the instructions under Form 3800 to allocate credits to your patrons.

Line 7

- Add the amounts from Lines 1b, 2b, 3b, 4b, 5b, and 6 to calculate your total investment credit for these projects.

- Report this total on Form 3800, Part III, line 1a.

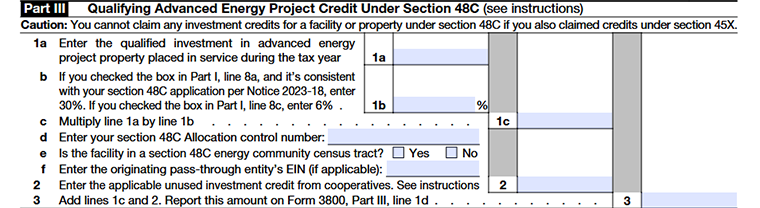

Part III-Qualifying Advanced Energy Project Credit Under Section 48C

Line 1a

Enter the qualified investment amount in a qualifying advanced energy project under. This is the cost (basis) of eligible property placed in service during the tax year.

Line 1b

Enter the applicable credit rate:

- 30% if you meet the prevailing wage and apprenticeship (PWA) requirements and the project was certified accordingly under Section 48C(e) (per IRS guidance).

- Otherwise, enter 6%.

Line 1c

Multiply the qualified investment (Line 1a) by the applicable percentage (Line 1b) to calculate the credit amount.

Line 1d

Enter the Section 48C allocation control number received for the qualifying project.

Line 1e

Indicate whether the facility is located in a Section 48C energy community census tract.

- Select “Yes” if the project is located in a qualifying energy community area.

- Select “No” if it is not.

Line 1f

If the TIN reported in Part I, Line 3b(ii) is different from the originating pass-through entity’s EIN,enter that EIN. Otherwise, leave this line blank.

Line 2

- If you are a patron of a cooperative, enter any unused investment credit from a qualifying advanced energy project (Section 48C) that was allocated to you.

- If you are a cooperative, follow Form 3800 instructions to allocate credits to your patrons.

Line 3

If you are a partnership or S corporation and choose to transfer the credit under Section 6418(c), enter the total credit amount here.

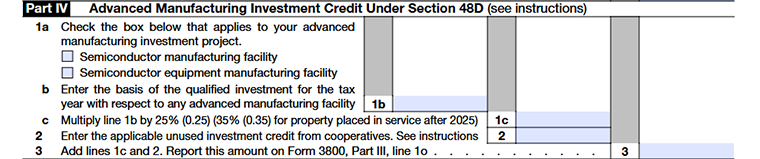

Part IV-Advanced Manufacturing Investment Credit Under Section 48D

Line 1a

Select the type of advanced manufacturing project you are claiming the credit for:

- Semiconductor manufacturing facility, or

- Semiconductor equipment manufacturing facility

Line 1b

Enter the total basis of your qualified investment in the advanced manufacturing facility placed in service during the tax year.

Line 1c

Calculate the credit based on when the property was placed in service:

- 25% (0.25): If placed in service before 2026

- 35% (0.35): If placed in service after 2025 (generally for fiscal-year filers ending in 2026)

Line 2

- If you are a patron of a cooperative, enter any unused advanced manufacturing investment credit (Section 48D) allocated to you.

- If you are a cooperative, follow Form 3800, Part III, line 1o to allocate credits to your patrons.

Line 3

- If you are a partnership or S corporation electing to receive a direct payment of the credit under Section 48D(d)(2)(A), enter the credit amount here.

- Also report this amount on Form 3800, Part III, line 1o.

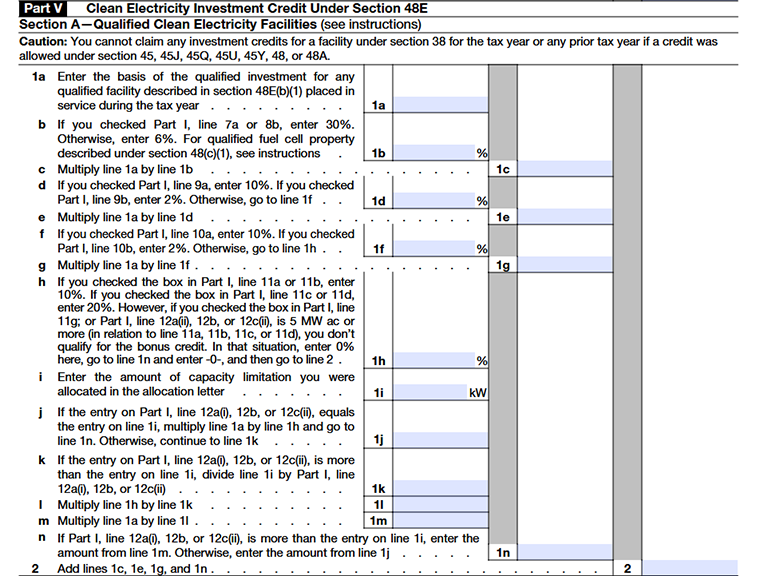

Part V-Clean Electricity Investment Credit Under Section 48E

Section A-Qualified Clean Electricity Facilities

Line 1a

Enter the total investment in a qualified facility under Section 48E(b)(1) that was placed in service during the tax year.

Line 1b

Enter the credit percentage based on eligibility (see increased credit rules).

- For qualified fuel cell property under Section 48(c)(1)(used to generate electricity and with construction beginning after 2026), enter 30%.

Line 1c

Multiply Line 1a by Line 1b to calculate the credit amount.

Line 1d

- Enter the domestic content bonus percentage if your project meets the requirements.

- If not eligible, leave it blank and skip to Line 1f.

Line 1f

Multiply Line 1a by Line 1d to calculate the domestic content bonus credit amount.

Line 1f

- Enter the energy community bonus percentage if the facility is located in a qualifying area.

- If not applicable, leave it blank and skip to Line 1h.

Line 1g

Multiply Line 1a by Line 1f to calculate the energy community bonus credit amount.

Line 1h

Enter the low-income communities bonus percentage if your project qualifies.

You cannot claim this bonus if:

- You selected “No” in Part I, Line 11g, or

- Your project capacity is 5 MW AC or more.

- If not eligible, enter 0 on Lines 1h and 1n, then go to Line 2.

Line 1i

Enter the capacity (in kW) that was officially allocated to your project in the allocation letter.

Line 1j

- If your project’s total capacity (from Part I, Line 12) is equal to the allocated capacity (Line 1i)

- Multiply Line 1a by Line 1h and go directly to Line 1n.

Line 1k

- If your project capacity is greater than the allocated capacity

- Divide Line 1i by the total project capacity (Part I, Line 12) to get the eligible proportion.

Line 1l

Multiply the low-income bonus percentage (Line 1h) by the proportion from Line 1k.

Line 1m

Multiply Line 1a by Line 1l to calculate the adjusted bonus credit amount.

Line 1n

- If your project capacity is greater than the allocated capacity, enter the amount from Line 1m.

- Otherwise, enter the amount from Line 1j.

Line 2

Add the amounts from Lines 1c, 1e, 1g, and 1n to calculate the total credit amount for this section.

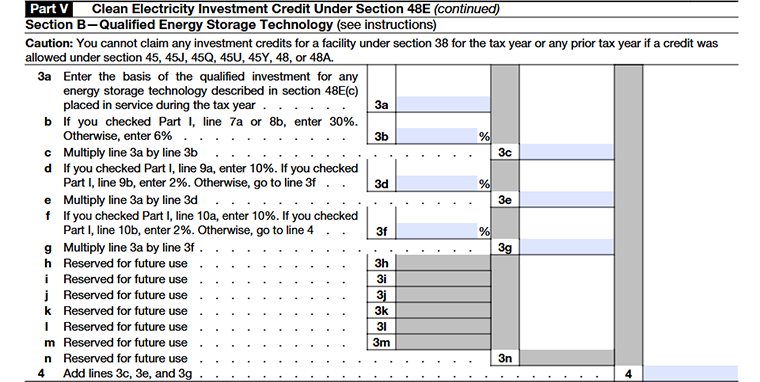

Section B-Qualified Energy Storage Technology

Line 3a

Enter the total investment (basis) in energy storage technology under Section 48E(c) that was placed in service during the tax year.

Line 3b

Enter the credit percentage based on eligibility .

Line 3c

Multiply Line 3a by Line 3b to calculate the base credit amount.

Line 3d

- Enter the domestic content bonus percentage if the energy storage project meets the requirements.

- If not eligible, leave blank, skip Line 3e, and go to Line 3f.

Line 3e

Multiply Line 3a by Line 3d to calculate the domestic content bonus credit.

Line 3f

- Enter the energy community bonus percentage if the project is located in a qualifying area.

- If not applicable, leave blank, skip Line 3g, and go to Line 4.

Line 3g

Multiply Line 3a by Line 3f to calculate the energy community bonus credit amount.

Lines 3h – 3n

These lines are reserved for future use. No entry is required for these lines.

Lines 4

Add the amounts from Lines 3c, 3e, and 3g to calculate the total credit for energy storage technology.

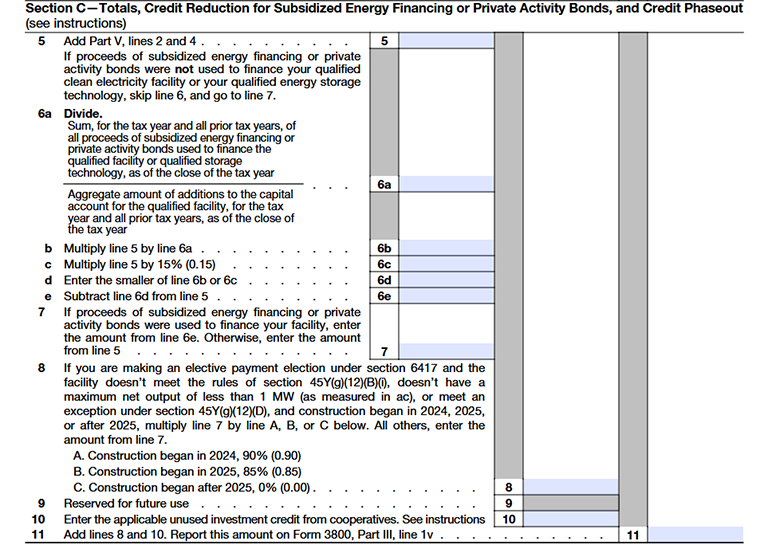

Section C-Totals, Credit Reduction for Subsidized Energy Financing or Private Activity Bonds, and Credit Phaseout

Lines 5

Add the amounts from Part V, Lines 2 and 4 to get the total clean electricity and energy storage credit.

Line 6a

Divide:

- Total subsidized financing or bond proceeds used (current + prior years) by, Total capital investment in the project (current + prior years)

Line 6b

Multiply Line 5 by Line 6a.

Line 6c

Multiply Line 5 by 15% (0.15).

Line 6d

Enter the smaller, Line 6b or Line 6c.

Line 6e

Subtract Line 6d from Line 5.

Line 7

- If your project used subsidized energy financing or private activity bonds, enter the amount from Line 6e.

- Otherwise, enter the amount from Line 5.

Line 8

This line applies if you are choosing an elective payment (direct payment) under Section 6417 and your project does not meet certain requirements (like domestic content or size limits).

If applicable, reduce your credit (Line 7) using:

- 90% if construction began in 2024

- 85% if construction began in 2025

- 0% if construction began after 2025

If not applicable, simply enter the amount from Line 7.

Line 9

This line is reserved for future use.

Line 10

- Enter any unused clean electricity investment credit(Section 48E) received from a cooperative.

- If you are a cooperative, follow Form 3800, Part III, line 1v to allocate credits to your patrons.

Line 11

- Add Lines 8 and 10 to calculate the total credit amount.

- Report this amount on Form 3800, Part III, line 1v.

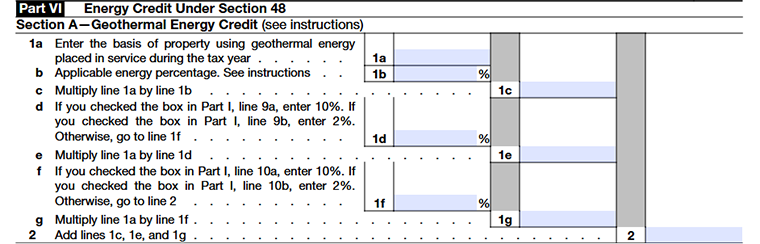

Part VI-Energy Credit Under Section 48

Section A-Geothermal Energy Credit

Line 1a

Enter the total basis of geothermal energy property placed in service during the tax year.

Line 1b

Enter the credit percentage based on:

- When construction began, and

- Whether PWA (prevailing wage & apprenticeship) requirements are met

Line 1c

Multiply Line 1a by Line 1b to calculate the base credit amount.

Line 1d

Enter the applicable domestic content bonus percentage for your project

Line 1e

Multiply Line 1a by Line 1d to calculate the domestic content bonus credit.

Line 1f

- Enter the applicable energy community bonus percentage (see energy community bonus rules).

- If the project is not located in a qualifying energy community, leave this line blank, skip Line 1g, and go to Line 2.

Line 1g

Multiply Line 1a by Line 1f to calculate the energy community bonus credit amount.

Line 2

Add the amounts from Lines 1c, 1e, and 1g to calculate the total geothermal energy credit.

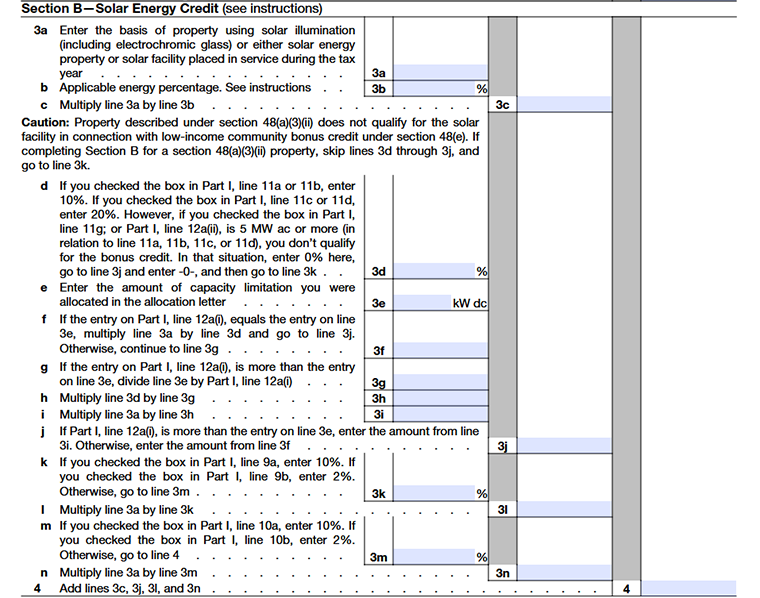

Section B-Solar Energy Credit

Line 3a

- Enter the total basis of solar energy property placed in service during the tax year.

- Includes solar equipment, solar facilities, and electrochromic glass.

Line 3b

Enter the credit percentage based on:

- When construction began, and

- Whether PWA requirements are met

Line 3c

Multiply Line 3a by Line 3b to calculate the base credit.

Line 3d

Enter the applicable low-income communities bonus percentage for your solar project.

However, you do not qualify for this bonus if:

- You selected “No” in Part I, Line 11g, or

- Your project capacity is 5 MW AC or more (based on Part I, Line 12a(ii)).

- If not eligible, enter 0% on Lines 3d and 3j, and continue to Line 3k.

Line 3e

Enter the allocated capacity (kW DC) from your allocation letter.

Line 3f

If your project capacity = allocated capacity, Multiply Line 3a by Line 3d and go to Line 3j.

Line 3g

If your project capacity is higher, Divide allocated capacity (3e) by total capacity (Part I, Line 12a(i)).

Line 3h

Multiply Line 3d by Line 3g to adjust the bonus percentage.

Line 3i

Multiply Line 3a by Line 3h to calculate the adjusted bonus credit.

Line 3j

- If capacity exceeds allocation on Line 3e, enter the amount in Line 3i.

- Otherwise, enter Line 3f.

Line 3k

- Enter the applicable domestic content bonus percentage for your solar project.

- If the project does not meet the requirements, leave this line blank, skip Line 3l, and continue to Line 3m.

Line 3l

Multiply Line 3a by Line 3k to calculate the domestic content bonus credit.

Line 3m

- Enter the applicable energy community bonus percentage.

- If the project is not located in a qualifying energy community, leave this line blank, skip Line 3n, and go toLine 4.

Line 3n

Multiply Line 3a by Line 3m to calculate the energy community bonus credit.

Line 4

Add Lines 3c, 3j, 3l, and 3n to calculate the total solar energy credit.

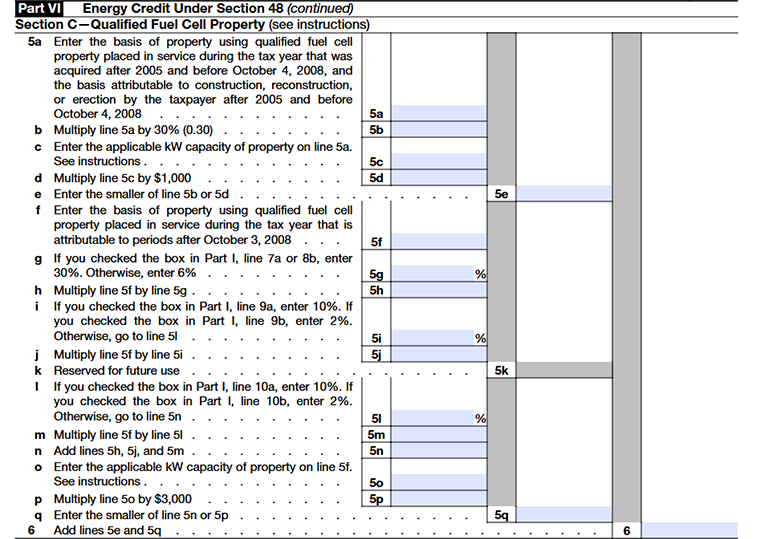

Section C-Qualified Fuel Cell Property

Line 5a

Enter the basis of qualified fuel cell property tied to periods after 2005 and before October 4, 2008, placed in service during the tax year.

Line 5b

Multiply Line 5a by 30% (0.30) to calculate the initial credit amount based on your investment.

Line 5c

Enter the total capacity (in kilowatts) related to the amount in Line 5a. Must be a whole number.

Line 5d

Multiply Line 5c by $1,000 to determine the maximum credit allowed based on capacity.

Line 5e

Enter the smaller Line 5b or Line 5d. This ensures your credit does not exceed the per-kilowatt limit.

Line 5f

Enter the basis of qualified fuel cell property tied to periods after October 3, 2008, where:

- Construction began before 2021 or after 2022, and

- The property was placed in service during the tax year.

Line 5g

Enter the applicable energy credit percentage based on eligibility.

Line 5h

Multiply Line 5f by Line 5g

Line 5i

- Enter the applicable domestic content bonus percentage for the project.

- If the project does not meet the requirements, leave this line blank, skip Line 5j, and continue to Line 5l.

Line 5j

Multiply Line 5f by Line 5i.

Line 5k

This line is reserved for future use. No entry is required.

Line 5l

- Enter the applicable energy community bonus percentage for the project.

- If the project is not located in a qualifying energy community, leave this line blank, skip Line 5m, and go toLine 5n.

Line 5m

Multiply Line 5f by Line 5l.

Line 5n

Add Lines 5h, 5j, and 5m.

Line 5o – Capacity (kW)

Enter the total kilowatt capacity related to the investment reported on Line 5f.

Line 5p

Multiply Line 5o by $3,000.

Line 5q

Enter the smaller of Line 5n or Line 5p.

Line 6

Add Lines 5e and 5q to calculate the total fuel cell credit.

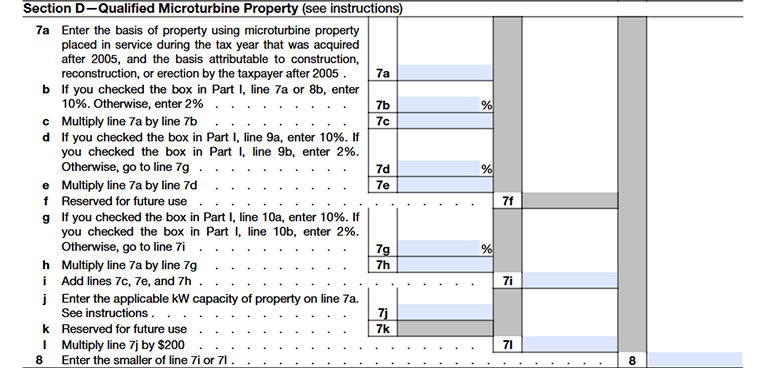

Section D-Qualified Microturbine Property

Line 7a

Enter the total basis of qualified microturbine property placed in service during the tax year. Include amounts related to periods after 2005.

Line 7b

Enter the applicable energy credit percentage based on eligibility.

Line 7c

Multiply Line 7a by Line 7b to calculate the base credit amount.

Line 7d

- Enter the applicable domestic content bonus percentage for the project.

- If the project does not meet the requirements, leave this line blank, skip Line 7e, and continue to Line 7g.

Line 7e

Multiply Line 7a by Line 7d.

Line 7f

This line is reserved for future use.

Line 7g

- Enter the applicable energy community bonus percentage.

- If the project is not located in a qualifying energy community, leave this line blank, skip Line 7h, and go toLine 7i.

Line 7h

Multiply Line 7a by Line 7g

Line 7i

Add Lines 7c, 7e, and 7h to determine the total microturbine credit.

Line 7j

Enter the total kilowatt capacity related to the investment reported on Line 7a.

Line 7k

This line is reserved for future use.

Line 7l

Multiply Line 7j by $200 to calculate the maximum credit allowed based on capacity.

Line 8

Enter the smaller of Line 7i or Line 7l.

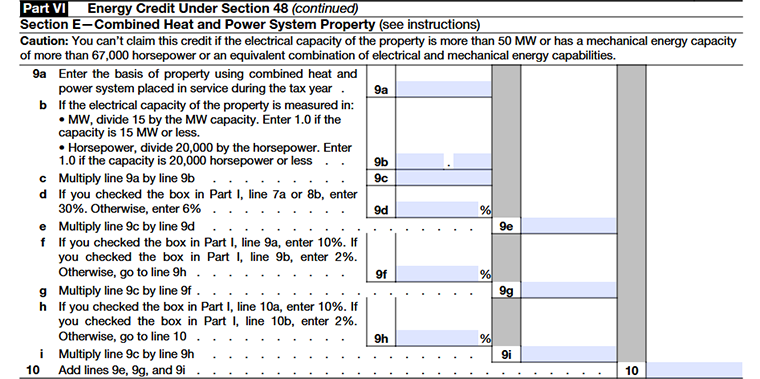

Section E-Combined Heat and Power System Property

Line 9a

Enter the basis of property using Combined heat and power (CHP) system placed in service during the tax year.

Line 9b

Calculate the capacity adjustment factor:

- If electrical capacity is in MW: divide 15 by MW capacity (enter 1.0 if ≤ 15 MW)

- If capacity is in horsepower: divide 20,000 by horsepower (enter 1.0 if ≤ 20,000 hp)

Line 9c

Multiply Line 9a by Line 9b.

Line 9d

Enter the applicable energy percentage for the project.

Line 9e

Multiply Line 9c by Line 9d.

Line 9f

Enter the applicable domestic content bonus credit percentage.

Line 9g

Multiply Line 9c by Line 9f to calculate the domestic content bonus credit.

Line 9h

Enter the applicable energy community bonus credit percentage.

Line 9i

Multiply Line 9c by Line 9h .

Line 10

Add Lines 9e, 9g, and 9i to determine the total Combined Heat and Power (CHP) system credit.

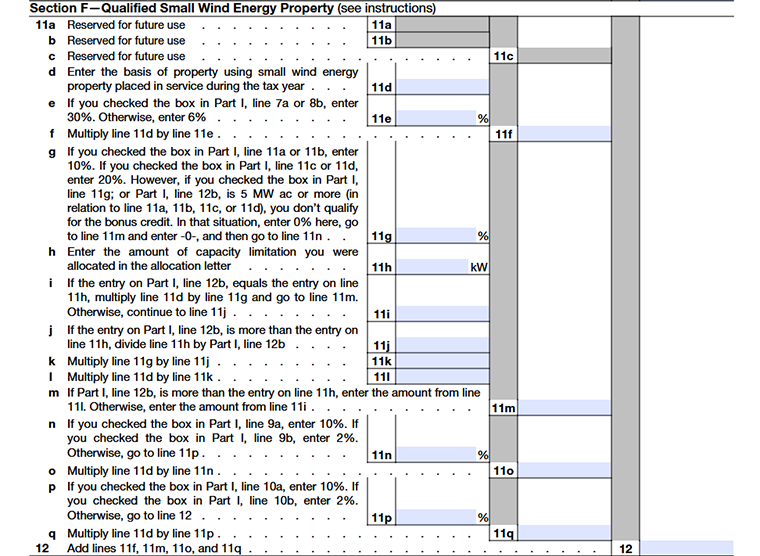

Section F-Qualified Small Wind Energy Property

Line 11a-11c

This line is reserved for future use.

Line 11d

Enter the basis of qualified small wind energy property placed in service during the tax year.

This applies only if:

- Acquired the property, or

- Constructed, reconstructed, or erected it yourself.

Line 11e

Enter the applicable energy percentage for the project.

Line 11f

Multiply Line 11d by Line 11e

Line 11g

Enter the applicable low-income communities bonus credit percentage for the small wind energy facility.

Line 11h

Enter the capacity limitation allocated to you as stated in the allocation letter.

Line 11i

- If Part I, Line 12b equals Line 11h, then Multiply Line 11d by Line 11g, this becomes your bonus credit amount. Then skip to Line 11m.

- If not equal, proceed to Line 11j.

Line 11j

If Part I, Line 12b is greater than Line 11h, calculate:

Divide Line 11h by Part I, Line 12b. This gives a proportional allocation factor.

Line 11k

Multiply Line 11g by Line 11j.

Line 11l

Multiply Line 11d by Line 11k.

Line 11m

Final determination of the bonus credit:

- If Part I, Line 12b is greater than Line 11h, enter the amount from Line 11l

- Otherwise, enter the amount from Line 11i.

Line 11n

Enter the applicable domestic content bonus credit percentage. If the project does not meet domestic content requirements, then:

- Leave Line 11n blank

- Skip Line 11o

- Proceed directly to Line 11p

Line 11n

Multiply Line 11d by Line 11n

Line 11p

Enter the applicable energy community bonus credit percentage. If the project is not located in a qualifying energy community, then:

- Leave Line 11p blank

- Skip Line 11q

- Proceed to Line 12

Line 11q

Multiply Line 11d by Line 11p.

Line 12

Add Lines 11f, 11m, 11o, and 11q to determine the total credit for the small wind energy property.

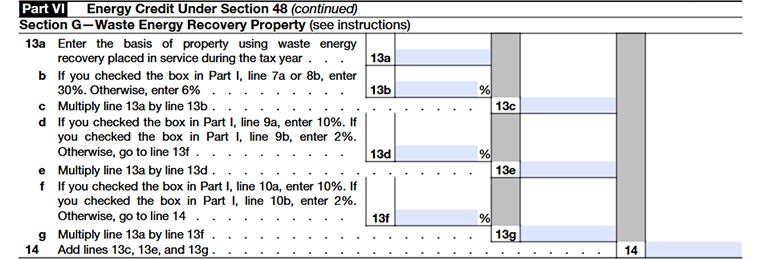

Section G-Waste Energy Recovery Property

Line 13a

Enter the basis of waste energy recovery property placed in service during the tax year.

Line 13b

Enter the applicable energy percentage for the project.

Line 13c

Multiply Line 13a by Line 13b.

Line 13d

Enter the applicable domestic content bonus credit percentage. If the project does not meet the domestic content requirements, then:

- Leave Line 13d blank

- Skip Line 13e

- Proceed to Line 13f

Line 13e

Multiply Line 13a by Line 13d.

Line 13f

Enter the applicable energy community bonus credit percentage. If the project is not located in a qualifying energy community, then:

- Leave Line 13f blank

- Skip Line 13g

- Proceed to Line 14

Line 13g

Multiply Line 13a by Line 13f.

Line 14

Add Lines 13c, 13e, and 13g to determine the total waste energy recovery property credit.

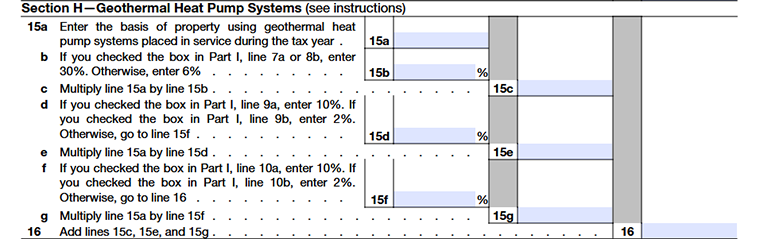

Section H-Geothermal Heat Pump Systems

Line 15a

Enter the basis of property using geothermal heat pump systems placed in service during the tax year.

Line 15b

Enter the applicable energy percentage for the project.

Line 15c

Multiply Line 15a by Line 15b to calculate the base credit amount.

Line 15d

Enter the applicable domestic content bonus credit percentage. If the project does not meet domestic content requirements, then:

- Leave Line 15d blank

- Skip Line 15e

- Proceed to Line 15f

Line 15e

Multiply Line 15a by Line 15d to calculate the domestic content bonus credit amount.

Line 15f

Enter the applicable energy community bonus credit percentage. If the project is not located in a qualifying energy community, then:

- Leave Line 15f blank

- Skip Line 15g

- Proceed to Line 16

Line 15g

Multiply Line 15a by Line 15f to calculate the energy community bonus credit amount.

Line 16

Add Lines 15c, 15e, and 15g to determine the total geothermal heat pump system credit.

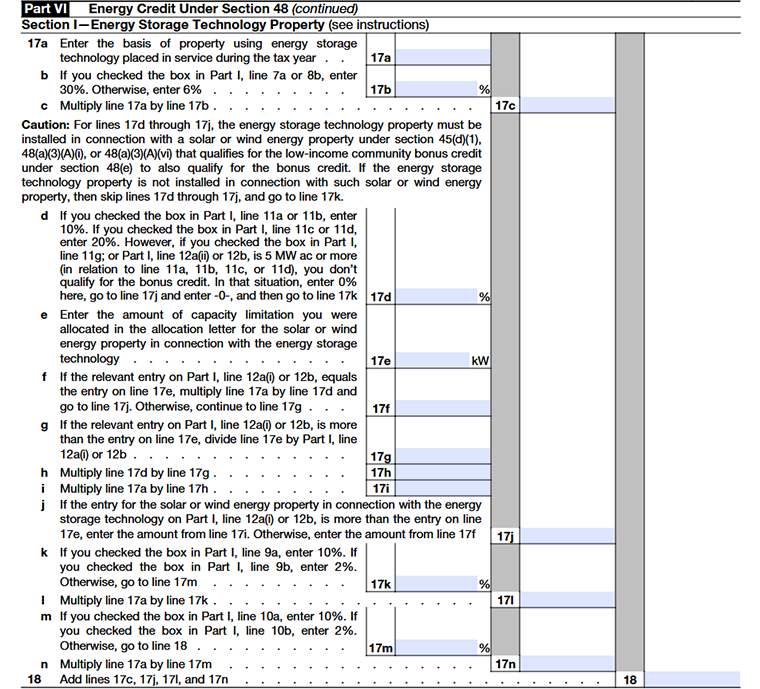

Section I-Energy Storage Technology Property

Line 17a

Enter the basis of energy storage technology property placed in service during the tax year. This includes only the portion of cost attributable to construction, reconstruction, or erection by the taxpayer.

Line 17b

Enter the applicable energy percentage.

Line 17c

Multiply Line 17a by Line 17b to calculate the base energy storage credit amount.

Line 17d

Enter the applicable low-income communities bonus credit percentage

However, you are not eligible for this bonus if either of the following applies:

- You checked the box in Part I, Line 11g, or

- Part I, Line 12a(ii) or 12b is 5 MW AC or more

If either condition applies:

- Enter 0 on Lines 17d and 17j

- Skip to Line 17k

Line 17e

Enter the capacity limitation allocated to you for the solar or wind energy property associated with the energy storage system.

Line 17f

- If the value in Part I, Line 12a(i) or 12b equals Line 17e, then: Multiply Line 17a by Line 17d, Enter the result here, then skip to Line 17j

- If not equal, continue to Line 17g.

Line 17g

If Part I, Line 12a(i) or 12b is greater than Line 17e, calculate: Line 17e divided by Part I, Line 12a(i) or 12b

Line 17h

Multiply Line 17d by Line 17g to calculate the adjusted bonus percentage.

Line 17i

Multiply Line 17a by Line 17h to calculate the adjusted low-income communities bonus credit amount.

Line 17i

Final determination:

- If Part I, Line 12a(i) or 12b is greater than Line 17e, enter the amount from Line 17i

- Otherwise, enter the amount from Line 17f

Line 17k

Enter the applicable domestic content bonus credit percentage. If the project does not meet domestic content requirements, then:

- Leave Line 17k blank

- Skip Line 17l

- Proceed to Line 17m

Line 17l

Multiply Line 17a by Line 17k to calculate the domestic content bonus credit amount.

Line 17m

Enter the applicable energy community bonus credit percentage. If the project is not located in a qualifying energy community, then:

- Leave Line 17m blank

- Skip Line 17n

- Proceed to Line 18

Line 17n

Multiply Line 17a by Line 17m.

Line 18

Add Lines 17c, 17j, 17l, and 17n to determine the total energy storage technology credit.

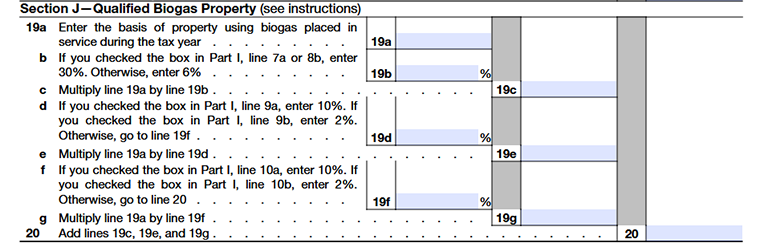

Section J-Qualified Biogas Property

Line 19a

- Enter the basis of qualified biogas energy property placed in service during the tax year.

- Include only the portion of the cost attributable to construction, reconstruction, or erection by the taxpayer.

Line 19b

Enter the applicable energy percentage.

Line 19c

Multiply Line 19a by Line 19b to calculate the base biogas energy credit amount.

Line 19d

Enter the applicable domestic content bonus credit percentage.

If the project does not meet domestic content requirements, then: leave Line 19d blank, skip Line 19e and proceed to Line 19f .

Line 19e

Multiply Line 19a by Line 19d.

Line 19f

Enter the applicable energy community bonus credit percentage.

If the project is not placed in service within an energy community, then: leave Line 19f blank, skip Line 19g and proceed to Line 20.

Line 19g

Multiply Line 19a by Line 19f.

Line 20

Add Lines 19c, 19e, and 19g to determine the total qualified biogas energy property credit.

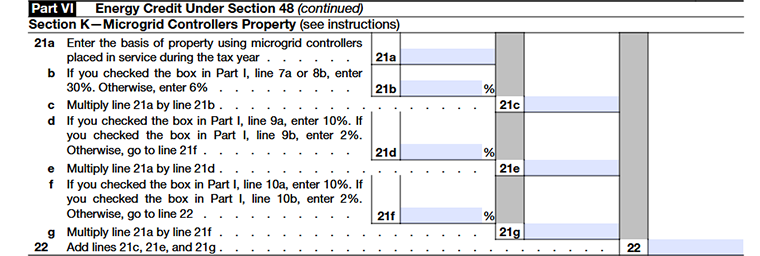

Section K-Microgrid Controllers Property

Line 21a

- Enter the basis of qualified microgrid controller property placed in service during the tax year.

- Include the portion of the cost attributable to construction, reconstruction, or erection by the taxpayer.

Line 21b

Enter the applicable energy percentage.

Line 21c

Multiply Line 21a by Line 21b to calculate the base microgrid controller credit amount.

Line 21d

- Enter the applicable domestic content bonus credit percentage.

- If the project does not meet domestic content requirements, then: leave Line 21d blank, skip Line 21e and proceed to Line 21f.

Line 21e

Multiply Line 21a by Line 21d.

Line 21f

- Enter the applicable energy community bonus credit percentage.

- If the project is not located in a qualifying energy community, then: leave Line 21f blank, skip Line 21g and proceed to Line 22

Line 21g

Multiply Line 21a by Line 21f to calculate the energy community bonus credit amount.

Line 22

Add Lines 21c, 21e, and 21g to determine the total qualified microgrid controller property credit.

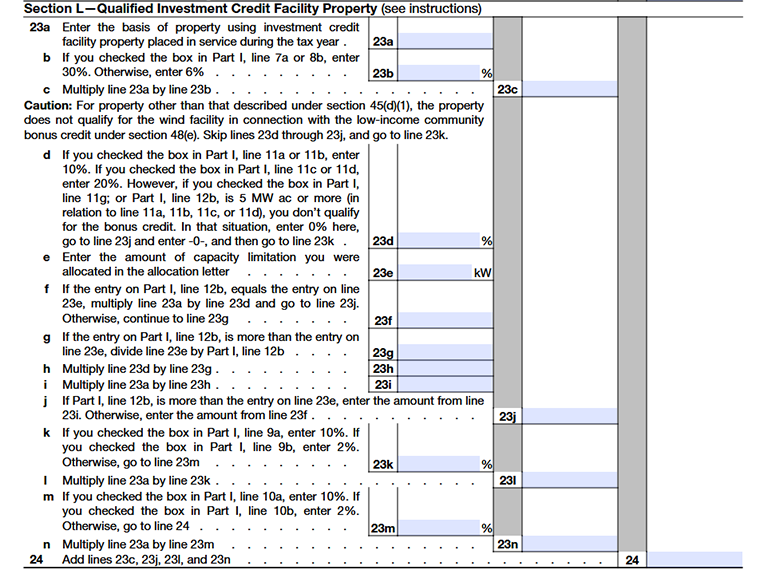

Section L-Qualified Investment Credit Facility Property

Line 23a

Enter the basis of investment credit facility property placed in service during the tax year.

Line 23b

Enter the applicable base credit percentage:

- Enter 30% if you checked the box in Part I, Line 7a or 8b

- Otherwise, enter 6%

Line 23c

Multiply Line 23a by Line 23b.

Line 23d

Enter the applicable low-income communities bonus credit percentage for the wind energy facility.

- You do not qualify for this bonus if you checked the box in Part I, Line 11g, or if Part I, Line 12b is 5 MW AC or more

- If either condition applies, enter 0 on Lines 23d and 23j

- Skip the remaining steps in this section and proceed to Line 23k.

Line 23e

Enter the capacity limitation allocated to you as per the allocation letter.

Line 23f

- If Part I, Line 12b equals Line 23e, then: Multiply Line 23a by Line 23d, enter the result here, then skip to Line 23j.

- If not equal, continue to Line 23g.

Line 23g

If Part I, Line 12b is greater than Line 23e, divide Line 23e by Part I, Line 12b.

Line 23h

Multiply Line 23d by Line 23g to calculate the adjusted low-income bonus percentage.

Line 23i

Multiply Line 23a by Line 23h to calculate the adjusted low-income communities bonus credit amount.

Line 23j

Determine the final low-income bonus credit amount:

- If Part I, Line 12b is greater than Line 23e, enter the amount from Line 23i

- Otherwise, enter the amount from Line 23f.

Line 23k

Enter the applicable domestic content bonus credit percentage.

- If the project does not meet the requirements, leave Line 23k blank

- Skip Line 23l and proceed to Line 23m

Line 23l

Multiply Line 23a by Line 23k.

Line 23m

Enter the applicable energy community bonus credit percentage.

- If the project is not located in a qualifying energy community, leave Line 23m blank

- Skip Line 23n and proceed to Line 24

Line 23n

Multiply Line 23a by Line 23m.

Line24

Add Lines 23c, 23j, 23l, and 23n to determine the total investment credit facility property credit.

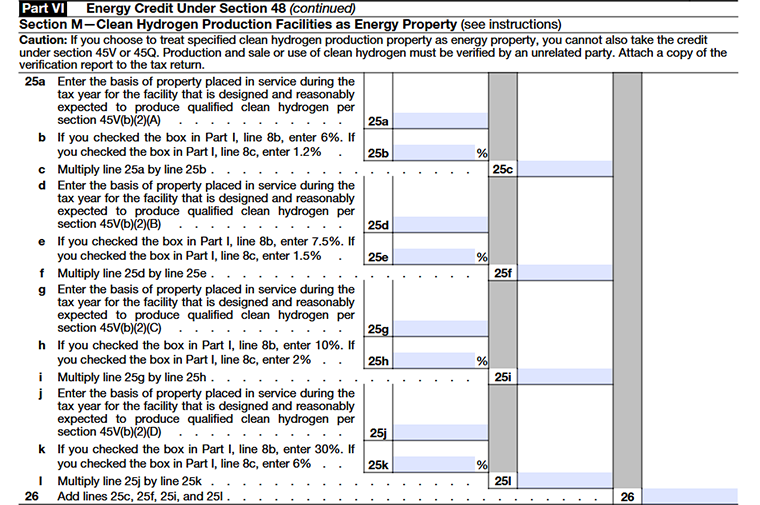

Section M-Clean Hydrogen Production Facilities as Energy Property

Line 25a

- Enter the basis of property placed in service during the tax year for a facility designed to produce qualified clean hydrogen.

- The process must result in a lifecycle greenhouse gas emission rate of no more than 4 kg of CO₂e per kg of hydrogen, and not less than 2.5 kg.

Line 25b

Enter the applicable energy percentage:

- Enter 6% if you checked the box in Part I, Line 8b

- Enter 1.2% if you checked the box in Part I, Line 8c

Line 25c

Multiply Line 25a by Line 25b.

Line 25d

- Enter the basis of property for a facility designed to produce qualified clean hydrogen with a lower emission range.

- The process must result in emissions less than 2.5 kg of CO₂e per kg of hydrogen, and not less than 1.5 kg.

Line 25e

Enter the applicable energy percentage:

- Enter 6% if you checked the box in Part I, Line 8b

- Enter 1.2% if you checked the box in Part I, Line 8c

Line 25f

Multiply Line 25d by Line 25e.

Line 25g

- Enter the basis of property placed in service during the tax year for a facility designed to produce qualified clean hydrogen.

- The process must result in emissions less than 1.5 kg of CO₂e per kg of hydrogen, but not less than 0.45 kg.

Line 25h

Enter the applicable energy percentage:

- Enter 10% if you checked the box in Part I, Line 8b

- Enter 2% if you checked the box in Part I, Line 8c

Line 25i

Multiply Line 25g by Line 25h.

Line 25j

Enter the basis of property for a facility designed to produce qualified clean hydrogen with the lowest emission range.

- The process must result in emissions less than 0.45 kg of CO₂e per kg of hydrogen

Line 25k

Enter the applicable energy percentage:

- Enter 30% if you checked the box in Part I, Line 8b

- Enter 6% if you checked the box in Part I, Line 8c

Line 25l

Multiply Line 25j by Line 25k to calculate the credit amount for this category.

Line 26

Add Lines 25c, 25f, 25i, and 25l to determine the total clean hydrogen property credit.

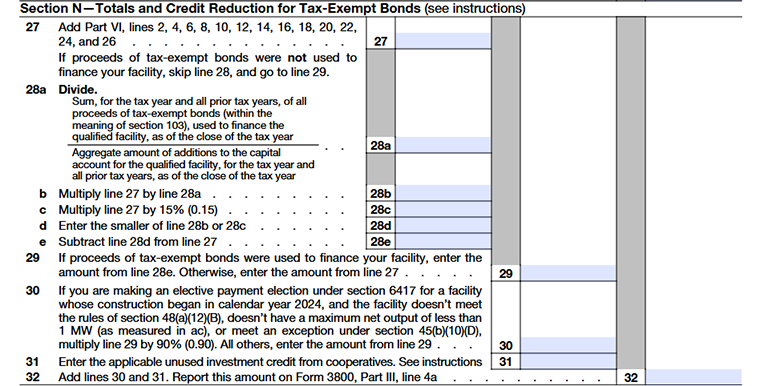

Section N-Totals and Credit Reduction for Tax-Exempt Bonds

Line 27

Add Part VI Lines 2, 4, 6, 8, 10, 12, 14, 16, 18, 20, 22, 24, and 26 to calculate the total energy credit.

Line 28

If tax-exempt bond proceeds were not used to finance the facility:

- Skip Line 28

- Proceed directly to Line 29

Line 28a

Calculate the tax-exempt bond financing ratio:

- Divide the total tax-exempt bond proceeds used (current + prior years)

- By the total capital additions to the facility (current + prior years)

Line 28b

Multiply Line 27 by Line 28a to determine the credit reduction based on bond financing.

Line 28c

Multiply Line 27 by 15% (0.15).

Line 28d

Enter the smaller of Line 28b or Line 28c.

Line 28e

Subtract Line 28d from Line 27 to determine the adjusted total energy credit after limitation.

Line 29

Enter the appropriate credit amount:

- If tax-exempt bond proceeds were used, enter the amount from Line 28e

- Otherwise, enter the amount from Line 27

Line 30

Determine if a reduction applies under section 6417:

- If you are making an elective payment election for a facility whose construction began in 2024, and it does not meet certain requirements, multiply Line 29 by 90% (0.90)

- Otherwise, enter the amount from Line 29 without any adjustment .

Line 31

Enter the unused investment credit from cooperatives.

Line 32

Add Lines 30 and 31 to calculate the final credit amount. Report this amount on Form 3800, Part III, Line 4a.

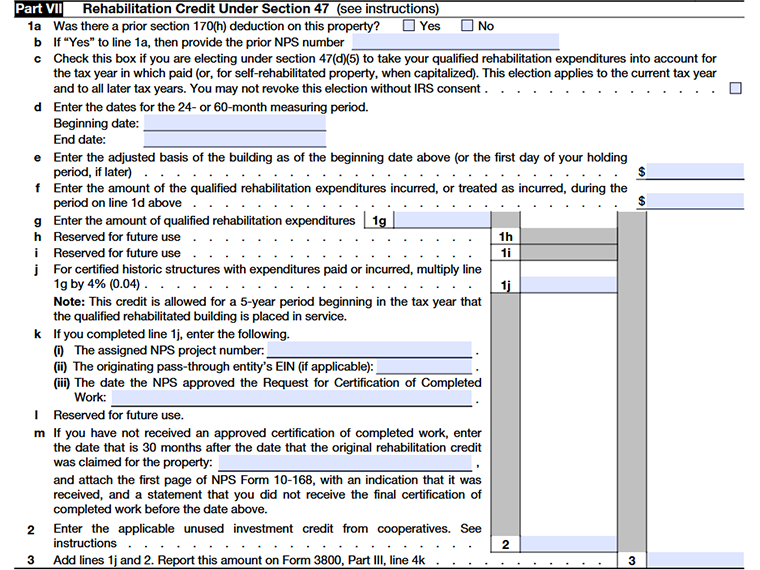

Part VII-Rehabilitation Credit Under Section 47

Line 1a

Check whether a charitable conservation contribution deduction under section 170(h) was claimed for the property. This applies only if you are claiming a credit for a certified historic structure

Line 1b

If you selected “Yes” on Line 1a, enter the NPS project number.

- This number is assigned by the National Park Service (NPS) to:

- A certified historic structure

- A building individually listed in the National Register of Historic Places

- A building located within a qualified historic district

- If the property is a single building individually listed, enter “00000”

- For more details, refer to:

- Instructions for Form 8283 (Noncash Charitable Contributions)

- Publication 526 (Charitable Contributions)

Line 1c

Indicate how you want to claim rehabilitation expenditures for credit purposes.

- Generally, expenses are claimed in the year the building is placed in service

- However, you may elect to claim them in the year they are paid or incurred if:

- The rehabilitation period is at least 2 years, and

- It is reasonable to expect the building will qualify when placed in service

- To make this election, check the box on Line 1c.

Line 1d

Enter the 24-month or 60-month measuring period for the rehabilitation project. Provide both the beginning date andending date.

Line 1e

Enter the adjusted basis of the building as of the beginning date entered on Line 1d. If your holding period begins later, use the first day of your holding period instead.

Line 1f

Enter the qualified rehabilitation expenditures (QREs) incurred or treated as incurred during the period specified on Line 1d.

Line 1g

Enter the total qualified rehabilitation expenditures.

Line 1h-1i

This line is reserved for future use.

Line 1j

Calculate the rehabilitation credit amount for qualified expenditures paid or incurred after 2017. The total credit is 20% of qualified rehabilitation expenditures, claimed over 5 years

Line 1k

Provide additional details if claiming a credit for a certified historic structure:

Line 1k(i)

Enter the NPS project number

Line 1k(ii)

Enter the EIN of the pass-through entity

Line 1k(iii)

Enter the date of final certification of completed work

Line 1l

This line is reserved for future use.

Line 1m

If final certification of completed work has not been received at the time of filing:

- Enter the date that is 30 months after the original credit claim date

- Attach:

- First page of NPS Form 10-168 (Part 2)

- Proof that the building is a certified historic structure (or that status was requested)

After receiving final certification:

- File Form 3468 with the next tax return

- Enter the NPS project number and certification date

- Attach an explanation and include prior claimed credit amounts

If certification is not received within 30 months:

- Submit a written statement to the IRS before the 30-month deadline

- You may need to agree to extend the assessment period under section 6501(c)(4)

Line 2

Enter any unused rehabilitation investment credit received from cooperatives.

Line 3

- Add Lines 1j and 2 to calculate the total rehabilitation credit.

- Report this amount on Form 3800, Part III, Line 4k

Commonly Asked Questions

1. What types of investments qualify for credit on Form 3468?

Form 3468 includes credits for rehabilitation, renewable energy investments, advanced energy projects, and much more.

2. When is the deadline for filing Form 3468?

The deadline for filing Form 3468 is typically the same as the deadline for filing Form 990-T.