Form 1041 Schedule D

Introduction

Schedule D (Form 1041) is used by estates and trusts to report capital gains and losses. This form is an essential part of Form 1041, the U.S. Income Tax Return for Estates and Trusts, and helps the IRS assess the tax liabilities associated with the sale or exchange of capital assets.

When an estate or trust has unrelated business taxable income (UBTI), as reported on

Form 990-T, any capital gains or losses must be accounted for to determine the total taxable income. Schedule D provides the necessary details on capital gains and losses, which are then included in the calculation of UBTI on Form 990-T.

In this resource guide, we will learn about the key aspects of Schedule D (Form 1041), from its purpose to filing requirements and commonly asked questions.

Table of Contents

What is Schedule D (Form 1041)?

Schedule D (Form 1041) is a supplemental form that estates and trusts use to detail their capital gains and losses from transactions involving capital assets. The form requires a breakdown of each transaction, including the description of the asset, date of acquisition, date of sale, sales price, and cost or other basis.

These assets can include stocks, bonds, real estate, and other investment holdings. The schedule separates transactions into short-term (held for one year or less) and long-term (held for more than one year) categories, ultimately calculating the net capital gain or loss for each.

Embark on a Smooth Schedule D Filing Journey with TaxZerone

Complete your Schedule D filing requirements with ease!

Who must file Schedule D (Form 1041)?

Any estate or trust that has realized capital gains or losses from the sale or exchange of capital assets during the tax year must file Schedule D (Form 1041) along with Form 990-T return

This includes:

- Estates with income from the sale or exchange of capital assets.

- Trusts that have realized capital gains or losses from investments.

- Any estate or trust with capital gain distributions from mutual funds or other regulated investment companies.

Schedule D (Form 1041) filing Requirements

This Schedule D (Form 1041) is used to report and calculate the capital gains and losses of an estate or trust from the sale or exchange of capital assets.

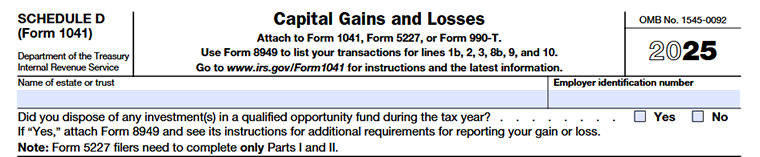

Name of estate or trust

Enter the name of the estate or trust filing the return.

Employer Identification Number

Enter its Employer Identification Number (EIN)

- Indicate Yes or No if the estate or trust sold or disposed of any investment in a Qualified Opportunity Fund during the tax year.

- If “Yes,” attach Form 8949 and follow its instructions to properly report the capital gain or loss from that transaction.

Below, we have provided Schedule D (Form 1041) filing requirements for each part.

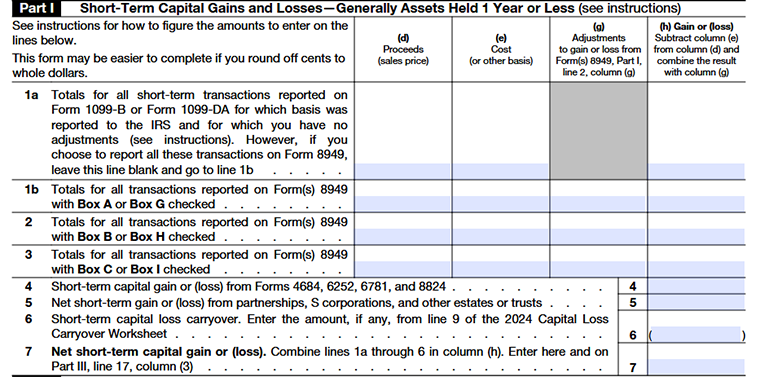

Part I-Short-Term Capital Gains and Losses Generally Assets held 1 year or less

Column (d)

This is the total amount you received when you sold the asset.

Column (e)

This is what you originally paid for the asset, including certain fees.

Column (g)

This includes any corrections or special adjustments from Form 8949 that change your gain or loss amount.

For example, wash sales or other IRS-required changes.

Column (h)

This is your final result

Formula:

Column(d)-Column(e) = result

Combine the result with Column(g)

Line 1a

Enter totals for short-term transactions reported on Form 1099-B or 1099-DA where:

- The IRS already received your cost basis, AND

- You have no adjustments to make.

If you report everything on Form 8949 instead, leave this line blank.

Line 1b

Enter totals from Form 8949 where Box A or Box G is checked. These usually involve transactions where basis was reported to the IRS, but adjustments may apply.

Line 2

Enter totals from Form 8949 where Box B or Box H is checked. These are usually transactions where the cost basis was not reported to the IRS.

Line 3

Enter totals from Form 8949 where Box C or Box I is checked. These are transactions that were not reported on Form 1099-B.

Line 4

Short-term gain from installment sales (from Form 6252, 4684, 6781, 8824). If you’re receiving payments over time from a sale, the short-term portion goes here.

Line 5

This line is used to report the total short-term capital gain or loss the estate or trust received from other entities, such as partnerships, S corporations, or another estate or trust.

Line 6

Enter any unused short-term capital loss from the previous year. This amount comes from line 9 of the 2024 Capital Loss Carryover Worksheet.

Line 7

Add everything from lines 1a through 6 and enter in column h.

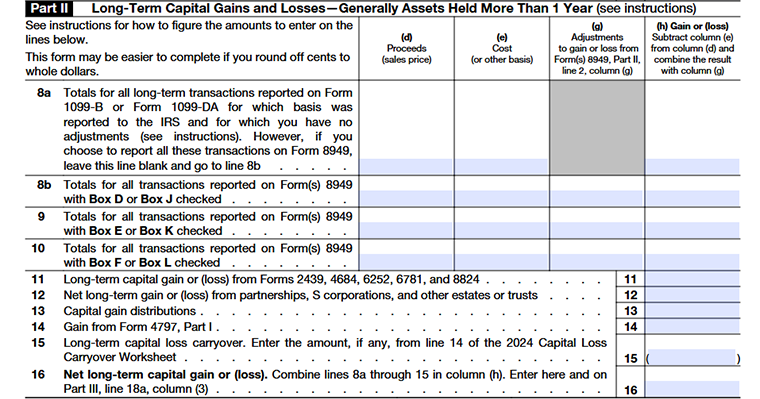

Part II-Long-term Capital Gains and Losses-Generally Assets held more than 1 year

The columns(d-h) in Part II are the same as the columns explained earlier in Part I, they follow the same meaning and calculation method described above.

Line 8a

Use this line to report the total of long-term sales shown on Form 1099-B or Form 1099-DA when the cost basis was already reported to the IRS and no adjustments are needed. Instead of listing each transaction on Form 8949, the corporation can combine them and report the totals directly here.

Line 8b

This line is used to transfer the total amounts from Form 8949 for long-term transactions where Box D or Box J is checked. These transactions were already detailed on Form 8949, so here you simply enter the combined totals.

Line 9

Enter the total of long-term transactions from Form 8949 where Box E or Box K is checked. These usually represent transactions where the cost basis was not reported to the IRS, so they must first be reported on Form 8949 before being summarized here.

Line 10

Use this line to report the totals from Form 8949 for transactions with Box F or Box L checked. These are long-term sales that were not reported on a Form 1099, so they must be listed on Form 8949 and then summarized on this line.

Line 11

Enter any long-term gain or loss reported on Forms 2439, 4684, 6252, 6781, or 8824 from certain transactions during the year.

Line 12

Report the long-term capital gain or loss received from partnerships, S corporations, or other estates or trusts. This amount usually comes from Schedule K-1.

Line 13

If the estate or trust received any capital gain payouts from investments, such as mutual funds or similar investment funds, report the total amount on this line.

Line 14

If there was a profit from selling certain business property, the gain reported on Form 4797, Part I should be entered here.

Line 15

If some long-term capital losses from last year couldn’t be used, the remaining amount that was carried forward should be entered on this line.

Line 16

Add together the amounts from lines 8a through 15 to find the total long-term capital gain or loss for the year and report the result here.

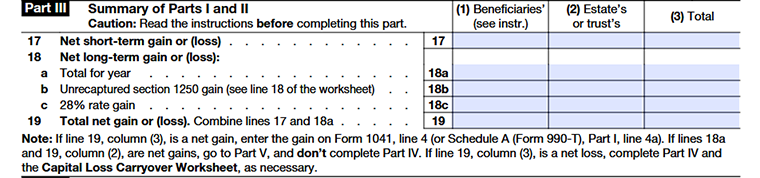

Part III-Summary of Parts I and II

Column (1)

The portion of the gain/loss that is passed through to the heirs.

Column (2)

The portion of the estate or trust kept will pay taxes directly.

Column (3)

The sum of both. This is the total performance for the year.

Line 17

The result of all assets held for one year or less. This is usually taxed at higher, ordinary income rates.

Line 18a

The final result of all assets held for more than a year. These usually get a break with lower tax rates.

Line 18b

A specific tax on profit from selling real estate that was previously depreciated.

Line 18c

Profits from collectibles (like art, coins, or antiques) or specific small business stock. These are taxed at a flat 28%.

Line 19

The Bottom Line. You add your short-term and long-term results together here to see if you made or lost money overall

Part IV-Capital Loss Limitation

Line 20

If a trust files Schedule D with Form 990-T and has more than one unrelated trade or business, it must calculate the taxable income for each business separately. The amount for each business should then be reported on line 4c of Part I of Schedule A (Form 990-T) for that specific activity.

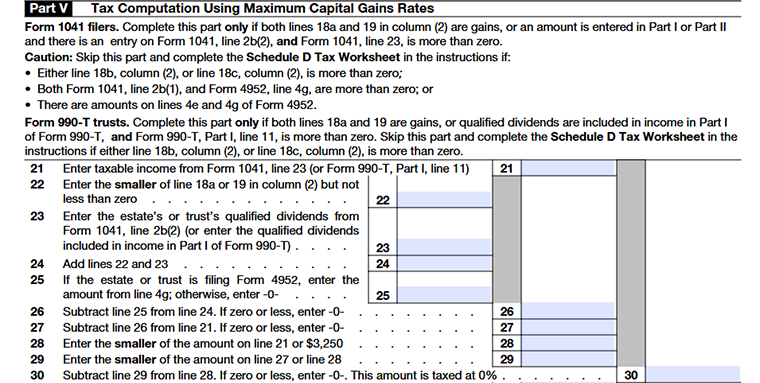

Part V-Tax Computation using Maximum Capital Gains Rates

Line 21

Enter the taxable income of the estate or trust from Form 1041 (line 23). This is the starting point for the tax calculation.

Line 22

Enter the smaller amount between line 18a and line 19 (column 2), but it cannot be less than zero. This helps determine the portion of income related to capital gains.

Line 23

Enter the qualified dividends received by the estate or trust from Form 1041 (line 2b(2)). These dividends may be taxed at special capital gain rates.

Line 24

Add line 22 and line 23. This gives the total amount of income that may qualify for the special tax rates.

Line 25

If the estate or trust is filing Form 4952, enter the amount from line 4g of that form. Otherwise, enter 0.

Line 26

Subtract line 25 from line 24. If the result is negative, enter 0.

Line 27

Subtract line 26 from line 21. If the result is negative, enter 0.

Line 28

Enter the smaller amount between line 21 or $3,250.

Line 29

Enter the smaller amount between line 27 or line 28.

Line 30

Subtract line 29 from line 28. If the result is zero or less, enter 0.This amount represents the portion of income taxed at the 0% capital gains rate.

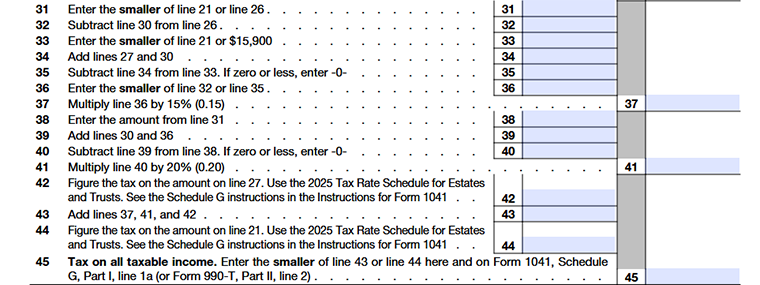

Line 31

Compare the numbers on line 21 and line 26. Take whichever is smaller and write it here.

Line 32

Take the number on line 26 and see what’s left after taking away line 30. Think of it like what’s remaining after you’ve already used some of it

Line 33

Compare line 21 with $15,900. Write the smaller amount. It’s basically setting a cap at $15,900.

Line 34

Simply combine the amounts from lines 27 and 30. This gives you the total of these two parts together.

Line 35

- Subtract line 34 from line 33. If zero or less, enter 0

- Take line 33 and subtract what you got in line 34. If the result is negative or zero, just write 0. This ensures you don’t carry a negative amount forward.

Line 36

- Enter the smaller of line 32 or line 35.

- Look at the numbers in lines 32 and 35. Pick the smaller number. This limits the next calculation to the lower of the two amounts.

Line 37

- Multiply line 36 by 15% (0.15).

- Take the number from line 36 and calculate 15% of it. This gives one portion of the tax you owe.

Line 38

- Enter the amount from line 31.

- Just copy the number you got in line 31. No calculation here.

Line 39

- Add lines 30 and 36.

- Add together the amounts from lines 30 and 36. This is another subtotal used for the next step.

Line 40

- Subtract line 39 from line 38. If zero or less, enter 0.

- Take line 38 and subtract line 39. If the result is negative or zero, write 0. Again, this avoids negative numbers in tax calculation.

Line 41

Take the result from line 40 and calculate 20% of it. This is another piece of the tax calculation.

Line 42

Use the 2025 Tax Rate Schedule for Estates and Trusts to calculate the tax owed on the amount from line 27. This follows official IRS tax tables.

Line 43

Add up the three calculated amounts from lines 37, 41, and 42. This gives a combined total tax based on the special calculations above.

Line 44

Use the 2025 Tax Rate Schedule for Estates and Trusts again but now calculate the tax on the number from line 21.

Line 45

Compare line 43 and line 44. Take the smaller number. This ensures you’re paying the correct, lower tax and then put it on Form 1041, Schedule G, line 1a (or Form 990-T, Part II, line 2).

Streamline Your 990-T Filing with TaxZerone!

Make your e-filing process simple by clicking the button below.

E-File Form 990-TCommonly Asked Questions

1. What information do I need to complete Schedule D?

2. Can estates and trusts offset capital gains with capital losses?

Yes, estates and trusts can offset capital gains with capital losses. If capital losses exceed capital gains, the excess loss can be carried forward to future tax years.