Form 1099-INT Instructions

Form 1099-INT at a Glance

- Form 1099-INT is used to report interest income paid to individuals or businesses. Banks, credit unions, investment firms, and other financial institutions that pay $10 or more in interest during the tax year may be required to file this form.

- Recipient copies must be furnished by January 31, and the form must be filed with the IRS by February 28 if filing on paper or March 31 if filing electronically.

- Late filing penalties increase based on how late the form is filed, ranging from $60 to $680 per return

- This article covers line-by-line instructions for Form 1099-INT, including payer and recipient details, Boxes 1–4 for interest income and withholding, Boxes 5–13 for foreign tax, tax-exempt interest, and bond premiums, and Boxes 14–17 for state reporting.

- Penalties: Form 1099-INT late filing penalties range from $60 to $680per return, based on the filing delay and intentional disregard of IRS filing requirements.

- Extensions: File Form 8809 to request an automatic filing extension. File Form 15397 to request the full 30-day extension for furnishing recipient copies.

What is IRS Form 1099-INT?

IRS Form 1099-INT is a tax return filed by financial institutions and other organizations that pay interest income to individuals or businesses. Its purpose is to report the total amount of interest earned by the recipient from various sources throughout the tax year.

1099 int form serves as an official record of interest income paid to a taxpayer, enabling them to properly declare this income and pay any taxes owed on the interest earned during the tax year.

Who can file Form 1099-INT?

Any individual, business, or entity that pays interest totaling $10 or more to another person or entity during the tax year is required to file Form 1099-INT. This form is used to report the interest payments made.

The types of organizations that must file Form 1099-INT include:

- Banks

- Credit unions

- Investment firms

- Other financial institutions

- Businesses that pay interest on loans or deposits they receive

Essentially, any payer of interest income must report those payments using Form 1099-INT if the total interest paid to a single recipient equals or exceeds $10 for the tax year.

When is the Form 1099-INT due date?

There are two key deadlines related to Form 1099-INT that payers must be aware of:

1. Filing deadline with IRS

The deadline for payers to file Form 1099-INT with the IRS depends on the filing method:

- E-filing deadline: March 31, 2026

If you're e-filing the Form 1099-INT to the IRS, the deadline is March 31st of the year following the tax year for which the form is being issued. - Paper filing deadline: February 28, 2026*

If you're filing Form 1099-INT with the IRS using traditional paper filing methods, the deadline is earlier — February 28th of the year following the tax year for which the form is being issued.

Avoid the last-minute 1099-INT deadline stress

E-file with TaxZerone now for easy IRS compliance and peace of mind.

2. Recipient copies deadline: January 31, 2026*

Payers are required to provide copies of Form 1099-INT to the recipients (individuals or entities that received interest payments) by January 31 of the year following the tax year for which the form is being issued. This ensures that recipients have the necessary information to accurately report their interest income when filing their tax returns.

It is crucial for payers to meet these deadlines to avoid potential penalties from the IRS for failure to file Form 1099-INT accurately and on time. Penalties may be imposed for late filing, failure to provide recipient copies, or reporting incorrect information on the form.

Form 1099-INT penalty

If you miss filing Form 1099-INT within the deadline, the IRS will impose a penalty for each missed return. Below is the breakdown of Form 1099-INT penalties:

| Days late | Penalty per return |

|---|---|

| Up to 30 days | $60 |

| 31 days late through August 1 | $130 |

| After August 1 or not filed | $340 |

| Intentional disregard | $680 |

Why risk penalties?

Choose TaxZerone to e-file your 1099-INT forms ahead of the deadline.

Form 1099-INT Instructions - How to fill out?

Let's see line-by-line instructions on how to fill out Form 1099-INT.

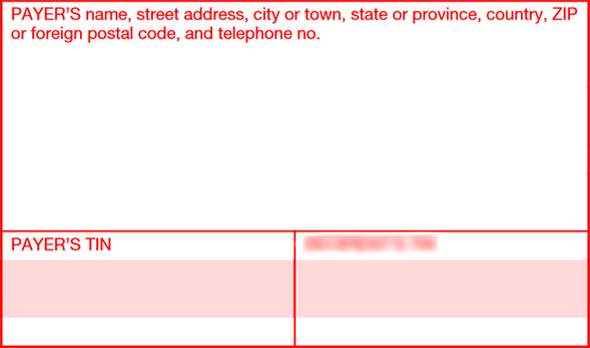

Payer details

Enter your name or business name, complete address, and TIN (SSN if you're an individual; EIN if you're a business)

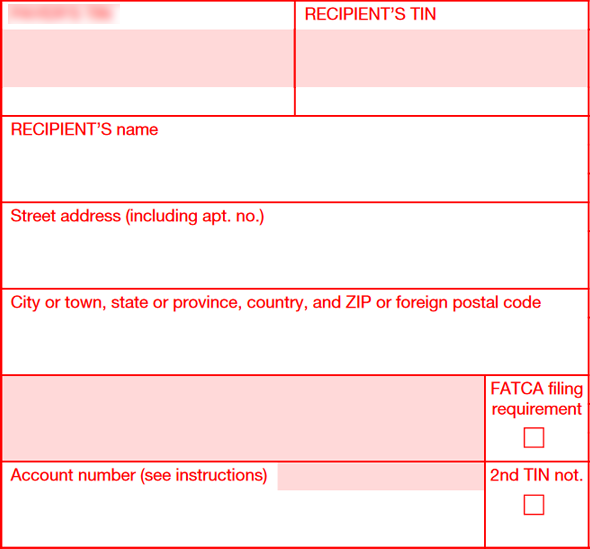

Recipient details

Enter the recipient's name, complete address, and TIN (SSN for an individual; EIN for a business).

- Account number: You must provide the account number in these two situations:

- You have multiple accounts for the same recipient, and you are filing more than one Form 1099-INT for that recipient.

- You checked the "FATCA filing requirement" box.

- 2nd TIN not:If the IRS has notified you two times within the last 3 years that the payee provided an incorrect TIN, you can enter an "X" in this box. By doing so, the IRS will stop sending you further notices about this account's TIN.

FATCA Filing Requirement Checkbox

Check this box if you are

- a U.S. payer that is reporting on Form(s) 1099 (including reporting payments in boxes 1, 3, 8, 9, and 10 on this Form 1099-INT) as part of satisfying your requirement to report with respect to a U.S. account for chapter 4 purposes, as described in Regulations section 1.1471-4(d)(2)(iii)(A).

- a foreign financial institution (FFI) reporting payments to a U.S. account pursuant to an election described in Regulations section 1.1471-4(d)(5)(i)(A).

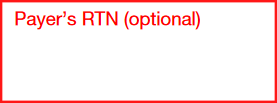

Payer's RTN (optional)

If you are a financial institution and wish to participate in the program for direct deposit of refunds, enter your routing transit number (RTN).

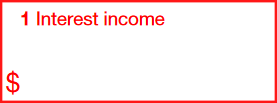

Box 1: Interest Income

Enter the taxable interest income not included in box 3.

Box 2: Early Withdrawal Penalty

Enter the amount of interest or principal you had to forfeit due to an early withdrawal from a time deposit account, such as a certificate of deposit (CD). This forfeited amount is deductible from your gross income by the recipient.

DO NOT subtract the forfeited amount from the interest income reported in Box 1. Report the full interest income amount in Box 1 and the early withdrawal penalty separately in Box 2.

Box 3: Interest on U.S. Savings Bonds and Treasury Obligations

Enter interest on U.S. Savings Bonds, Treasury bills, Treasury notes, and Treasury bonds. DO NOT include in box 1.

Box 4: Federal Income Tax Withheld

Enter any federal income tax that was withheld from the payments reported in Boxes 1, 3, and 8.

Box 5: Investment Expenses

This box is only relevant for single-class real estate mortgage investment conduits (REMICs). See the instructions under "Rules for REMICs, FASITs, and Issuers of CDOs" for information about reporting investment expenses in Box 5 for single-class REMICs.

Box 6: Foreign Tax Paid

Enter any foreign tax paid on interest. Report the amount in U.S. dollars.

Box 7: Foreign Country or U.S. Territory

Enter the name of the foreign country or U.S. territory for which the foreign tax was paid. Only applicable if you have reported in box 6.

Box 8: Tax-Exempt Interest

Enter any tax-exempt interest of $10 or more (not including tax-exempt original issue discount) that was paid or credited to the person's account. This includes interest from obligations issued by

- a state, the District of Columbia, a U.S. territory, an Indian tribal government, or their political subdivisions (such as port authorities, toll road commissions, utility services authorities, community redevelopment agencies, etc.)

- qualified volunteer fire departments to finance eligible expenditures.

Box 9: Specified Private Activity Bond Interest

Enter interest of $10 or more from specified private activity bonds.

Specified private activity bond means any private activity bond defined in section 141 and issued after August 7, 1986.

Box 10: Market Discount

If the recipient notified you that they made an election under section 1278(b) for a covered security acquired with a market discount, enter the amount of market discount that accrued on that debt instrument during the tax year, if the amount is $10 or more.

Box 11: Bond Premium

If a taxable bond was purchased above par value (at a premium), report the portion of that premium amount that can be amortized against the interest paid that year, unless the bondholder instructed you they did not want to amortize the premium.

Box 12. Bond Premium on Treasury Obligations

If a U.S. Treasury security was purchased above par value (at a premium), report the portion of that premium amount that can be amortized against the interest paid that year, unless the holder instructed you they did not want to amortize the premium.

Box 13: Bond Premium on Tax-Exempt Bond

If a tax-exempt bond was purchased above par value (at a premium), report the portion of that premium amount that can be amortized against the interest paid that year.

Box 14: Tax-Exempt and Tax Credit Bond CUSIP No.

- If reporting on a single tax-exempt bond, enter its CUSIP in Box 14

- If reporting on a single tax credit bond, enter its CUSIP in Box 14

- If aggregating interest/credits from multiple bonds, enter "various"

Boxes 15-17: State information

- Box 15: Enter the 2-letter state abbreviation for the state

- Box 16: Enter the state identification number

- Box 17: Report any state income tax withheld from the payment

How to file Form 1099-INT?

Form 1099-INT can be filed electronically or by postal mail.

Form 1099-INT electronic filing (E-filing)

The IRS recommends e-filing Form 1099-INT as the process is efficient and straightforward. E-filing offers the advantage of receiving notifications promptly after the IRS processes your submission.

With TaxZerone, the e-filing process is streamlined and can be completed within minutes. You simply need to fill out the form, review the information, transmit it to the IRS electronically, and provide the recipient's copy.

Paper filing

If you prefer to file Form 1099-INT via traditional paper methods, here are the steps to follow:

- Download and print Form 1099-INT from the IRS website.

- Complete the required fields, including the recipient's name, address, TIN, and interest amount. Also, provide your business name, address, and TIN.

- Mail the completed paper form to the IRS at the address specified in the 1099 instructions.

- Send a copy of the 1099-INT to the recipient by January 31st for their tax reporting purposes.

Important considerations for paper filing:

- Mail the forms several weeks before the deadline to ensure timely arrival at the IRS.

- You are required to provide a copy of the 1099-INT to the recipient for accurate tax reporting on their part.

- Paper filing involves printing, mailing, and tracking forms. As an alternative, you can choose to file 1099-INT forms electronically for faster processing and delivery.

Where to send Form 1099-INT - Mailing address

If you prefer paper filing, the mailing address for Form 1099-INT varies depending on your business location. Below is a table summarizing the mailing address for form 1099-int:

| If your business operates in or your legal residence is… | Mail Form 1099-INT to… |

|---|---|

| Alabama, Arizona, Arkansas, Delaware, Florida, Georgia, Kentucky, Maine, Massachusetts, Mississippi, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Ohio, Texas, Vermont, Virginia | Internal Revenue Service Austin Submission Processing Center P.O. Box 149213 Austin, TX 78714 |

| Alaska, Colorado, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Montana, Nebraska, Nevada, North Dakota, Oklahoma, Oregon, South Carolina, South Dakota, Tennessee, Utah, Washington, Wisconsin, Wyoming | Department of the Treasury IRS Submission Processing Center P.O. Box 219256 Kansas City, MO 64121-9256 |

| California, Connecticut, District of Columbia, Louisiana, Maryland, Pennsylvania, Rhode Island, West Virginia | Department of the Treasury IRS Submission Processing Center 1973 North Rulon White Blvd. Ogden, UT 84201 |

| Outside the United States | Internal Revenue Service, Austin Submission Processing Center, P.O. Box 149213, Austin, TX 78714 |

How to e-file Form 1099-INT with TaxZerone

Before initiating the e-filing process for Form 1099-INT, it's essential to have all the necessary information ready to ensure a smooth and efficient filing experience. Here's what you'll need:

Required information for filing Form 1099-INT:

- Business details

- Recipient details

- Interest income

- Early withdrawal penalty

- Amounts of bonds or treasury obligations

- Investment expenses

Once you have gathered all the required information, you can proceed with the e-filing process using TaxZerone in three simple steps:

Step 1: Complete Form 1099-INT

Fill out the form with the necessary details, including payer and recipient information, interest paid, and any federal income tax withheld.

Step 2: Review and transmit the return

Carefully review the information entered to ensure accuracy, and then transmit the completed Form 1099-INT to the IRS electronically.

Step 3: Provide the recipient copy

After transmitting the form to the IRS, send a copy of the completed Form 1099-INT to the recipient for their tax reporting purposes.

Benefits of e-filing Form 1099-INT with TaxZerone

When you choose to e-file Form 1099-INT with TaxZerone, you can enjoy the following advantages:

- IRS form validations: Ensure accuracy by checking your returns for potential errors or missing information.

- Email recipient copies: Conveniently send recipient copies via email.

- Secure portal access (ZeroneVault): Provide recipients with secure access to their return copies anytime, anywhere, through the ZeroneVault portal.

- Competitive pricing: Enjoy industry-leading pricing, with rates as low as $0.59 per form.

By leveraging TaxZerone's e-filing solution, you can streamline the Form 1099-INT filing process, ensuring accuracy, efficiency, and compliance with IRS requirements.