Form 8911 Alternative Fuel Vehicle Refueling

Property Credit

Introduction

Form 8911, Alternative Fuel Vehicle Refueling Property Credit, allows businesses, individuals, and certain tax-exempt organizations to claim tax credits for installing refueling equipment for alternative fuel vehicles.

For tax-exempt organizations filing Form 990-T, Form 8911 provides an opportunity to offset unrelated business income tax (UBIT) through credits on eligible alternative fuel refueling property investments.

This resource article will help you understand more about Form 8911 by clarifying who must file, the filing requirements, and addressing commonly asked questions.

Table of Contents

What's New?

Termination Date Updated

The One Big Beautiful Bill Act (P.L. 119-21) revised the expiration date for the Alternative Fuel Vehicle Refueling Property Credit under Section 30C. As a result, the credit is now scheduled to terminate on June 30, 2026, instead of December 31, 2032. Taxpayers generally cannot claim the credit for qualified alternative fuel vehicle refueling property placed in service after June 30, 2026.

New Reporting for Item A

Beginning with tax years that start after 2024, taxpayers must report the total number of qualified alternative fuel vehicle refueling properties on Item A of Form 8911. This change provides the IRS with additional information regarding the properties for which the credit is being claimed.

Form 7220 - Increased Credit Claims

Taxpayers claiming the increased credit amount based on compliance with the Prevailing Wage and Apprenticeship (PWA)requirements must file Form 7220, Prevailing Wage and Apprenticeship (PWA) Verification and Corrections. A separate Form 7220 is required for each qualified property for which the increased credit amount is claimed.

What Is Form 8911?

Form 8911, Alternative Fuel Vehicle Refueling Property Credit, is used to calculate and claim a tax credit for qualified alternative fuel vehicle refueling property placed in service during the tax year. The credit helps offset eligible installation costs and encourages investment in alternative fuel vehicle infrastructure.

Qualifying Property for Form 8911

The credit may be available for qualified refueling property, including:

- Electric vehicle (EV) charging equipment

- Hydrogen refueling equipment

- Natural gas refueling property

- Propane refueling property

To qualify, the property must be placed in service during the tax year and meet applicable IRS requirements.

Who must file Form 8911?

Generally, any organization that is subject to UBIT and has invested in alternative fuel vehicle refueling property must file Form 8911.

- Individuals and Businesses: Those who have invested in alternative fuel vehicle refueling property at their home or business.

- Partnerships and S corporations: They must file this form to claim the credit.

Choose TaxZerone for a filing experience that goes beyond expectations.

Empower your tax compliance journey with us today!

Applicable Entities and Elective Payment Election (EPE)

Certain organizations may qualify as applicable entities under Section 6417 and elect to receive the Alternative Fuel Vehicle Refueling Property Credit as a payment from the IRS through an Elective Payment Election (EPE), also known as Direct Pay.

Eligible Applicable Entities

- Tax-exempt organizations

- State and local governments

- Indian tribal governments

- Alaska Native Corporations

- Rural electric cooperatives

- Certain U.S. territories and their political subdivisions

Required Forms

Organizations making an EPE generally must file:

- Form 8911

- Schedule A (Form 8911)

- Form 3800

- Form 990-T or another applicable tax return

Pre-Filing Registration

Before filing the tax return, organizations intending to make an EPE or transfer election must complete the IRS pre-filing registration process for each qualified property or project associated with the credit. Upon successful registration, the IRS issues a registration number that must be included on the applicable tax forms when claiming the credit.

Form 8911: Line-by-Line Instruction

Before completing the credit calculation section, taxpayers must provide basic identifying information.

Name(s) Shown on Return

Enter the taxpayer's name exactly as it appears on the federal tax return to which Form 8911 is attached. The name entered on Form 8911 should match the name reported on the corresponding tax return.

Identifying Number

Identifying Number Enter the taxpayer's identifying number.

- Individuals should enter their Social Security Number (SSN).

- Businesses and tax-exempt organizations should enter their Employer Identification Number (EIN).

Item A – Total Number of Qualified Refueling Properties

Enter the total number of qualified alternative fuel vehicle refueling properties for which you are claiming the credit during the tax year.

- A separate Schedule A (Form 8911) must be completed and attached for each qualified property placed in service. The number entered on Item A should equal the total number of Schedule A forms filed with Form 8911. If the only credit being claimed is a pass-through credit received from a partnership or S corporation and reported on Line 2, enter 0 on Item A because no qualified refueling property was directly placed in service by the taxpayer.

Part I - Credit for Business/Investment Use Part of Refueling Property

Line 1 - Credit From Schedule A (Form 8911)

Enter the total credit amount from Part II of all Schedule A (Form 8911) forms attached to the return. This amount represents the total credit calculated for qualified alternative fuel vehicle refueling property placed in service during the tax year.

Line 2 - Pass-Through Credits

Enter any Alternative Fuel Vehicle Refueling Property Credits received from a partnership or S corporation.

These credits are reported on:

- Schedule K-1 (Form 1065),

- Schedule K-1 (Form 1120-S) ,

Partnerships and S corporations must report passed-through credits on this line. Other taxpayers claiming the credit on Form 8911 should also include any eligible pass-through credits received during the tax year.

If your only Alternative Fuel Vehicle Refueling Property Credit is a pass-through credit received from a partnership or S corporation, you may report the credit directly on Form 3800, Part III, Line 1s, instead of filing Form 8911.

Line 3 - Partnerships and S Corporations

Partnerships and S corporations that elect to transfer all or a portion of their Alternative Fuel Vehicle Refueling Property Credit under Section 6418 must report the total credit on Form 3800, Part III, Line 1s.

In these cases, the credit is reported on Form 3800 rather than being passed through to partners or shareholders on Schedule K.

Part II - Credit for Personal Use Part of Refueling Property

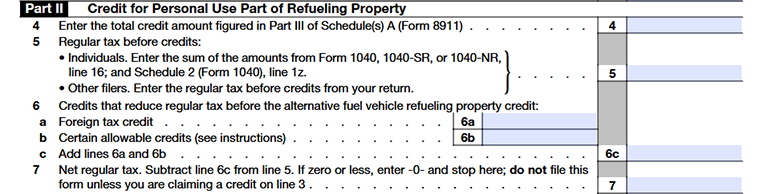

Line 4 - Credit of Schedule A (Form 8911)

Enter the total credit amount from Part III of all Schedule A (Form 8911) forms attached to the return. This amount represents the credit calculated for qualified alternative fuel vehicle refueling property reported in Part III of Schedule A.

Line 5 - Regular Tax Before Credits

Enter your regular tax liability before applying any credits.

- Individuals should enter the total of Form 1040, Form 1040-SR, or Form 1040-NR, Line 16, plus Schedule 2 (Form 1040), Line 1z.

- All other filers must enter the regular tax before credits as reported on their applicable tax return.

Line 6 - Tax-Reducing Credits

Line 6 is used to report certain credits that reduce your regular tax liability before the Alternative Fuel Vehicle Refueling Property Credit is applied.

Line 6a - Foreign Tax Credit

Enter the foreign tax credit claimed for the tax year. This is the amount used to reduce your regular tax liability before calculating the Alternative Fuel Vehicle Refueling Property Credit.

Line 6b - Certain Allowable Credits

Enter the total of other eligible credits that reduce your regular tax before applying the Alternative Fuel Vehicle Refueling Property Credit.

- Individuals filing Form 1040, Form 1040-SR, or Form 1040-NRshould include the total of any credits or adjustments reported on Line 19 of their return, along with the applicable credits reported on Schedule 3 (Form 1040), Lines 2 through 5 and Line 7.

- Estates and trusts filing Form 1041 should enter eligible write-in credits reported on Schedule G, Line 2e.

- Do not include any amounts already reported as a general business credit, prior-year minimum tax credit, or credit to holders of tax credit bonds when calculating Line 6b.

Line 6c - Total Credits

Add the amounts on Lines 6a and 6b and enter the result on Line 6c. This represents the total credits that reduce regular tax before the Alternative Fuel Vehicle Refueling Property Credit is applied.

Line 7 - Net Regular Tax

- Subtract Line 6c from Line 5 and enter the result on Line 7. This amount represents your net regular tax after applying the credits reported on Line 6.

- If the result is zero or less, enter 0 on Line 7. Generally, no further calculations are required, and Form 8911 does not need to be filed unless you are claiming a credit reported on Line 3.

Line 8 - Tentative Minimum Tax (TMT)

- Enter your Tentative Minimum Tax (TMT) on Line 8. Even if you do not owe the Alternative Minimum Tax (AMT), you must still calculate the TMT to determine the allowable “Alternative Fuel Vehicle Refueling Property Credit.”

- Complete and attach the applicable AMT form or schedule and enter the calculated TMT amount on this line.

Line 9 - Net Tax After TMT

- Subtract Line 8 from Line 7 and enter the result on Line 9. This amount is used to determine the credit that may be claimed on Form 8911.

- If the result is zero or less, enter 0 on Line 9. Generally, you do not need to continue filing Form 8911 unless you are claiming a credit reported on Line 3.

Line 10 - Credit Allowed After Tax Liability Limit

- Line 10 is used to determine the portion of the credit that can be claimed after applying the tax liability limitations. Any unused portion of the personal credit that cannot be claimed because of the tax liability limit is lost. The unused credit cannot be carried back to a prior tax year or carried forward to a future tax year.

Schedule A (Form 8911) - Alternative Fuel Vehicle Refueling Property

Schedule A (Form 8911) is used to calculate the “Alternative Fuel Vehicle Refueling Property” Credit for each qualified refueling property placed in service during the tax year. The information reported on Schedule A is used to determine the credit that flows to Form 8911.

A separate Schedule A must be completed for each qualified alternative fuel vehicle refueling property for which the credit is claimed. Taxpayers with multiple qualifying properties must attach a separate Schedule A for each property.

Schedule A also includes information about the property's

- Location,

- Qualified installation costs

- Eligibility requirements, and

- The calculation of the allowable credit amount.

How to Complete Schedule A (Form 8911): Line-by-Line Instructions

Name(s) Shown on Return

Enter the taxpayer's name exactly as it appears on the federal tax return to which Schedule A (Form 8911) is attached.

Identifying Number

Enter the taxpayer's identifying number.

- Individuals should enter their Social Security Number (SSN).

- Businesses and tax-exempt organizations should enter their Employer Identification Number (EIN).

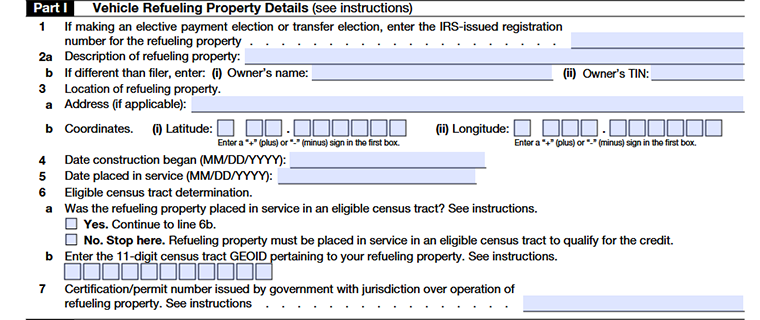

Part I - Vehicle Refueling Property Details

Line 1 - Registration Number

Enter the IRS-issued registration number if you are:

- An applicable entity making an Elective Payment Election (EPE), or

- An eligible taxpayer, partnership, or S corporation electing to transfer all or a portion of the credit.

The registration number is obtained by completing the IRS pre-filing registration proces for each qualified refueling property for which the credit is claimed.

If you are not making an Elective Payment Election (EPE) or a transfer election, you are not required to enter a registration number on Line 1.

Line 2a - Description of Refueling Property

Briefly describe the nature of your qualified refueling property. For instance, indicate whether the property installed in service refers to electric vehicle charging stations or other related refueling properties.

Line 2b - Property Owner Information

Complete this section if the owner of the refueling property is different from the taxpayer claiming the credit.

Line 2b(i) – Owner's Name

Line 2b(i) – Owner's Name Specify the actual legal name of the property owner.

Line 2b(ii) – Owner's TIN

Provide the Taxpayer Identification Number (TIN) of the property owner.

Line 3 is used to report the location of the qualified refueling property.

Line 3 is used to report the location of the qualified refueling property.

Line 3a - Property Address

Report the actual physical location or address of the property, if applicable.

Line 3b - Geographic Coordinates

Enter the geographic coordinates of the property's location.

Line 3b(i) - Latitude

Provide the latitude coordinates. Include plus (+) or minus (-) sign in the first box depending on the coordinates' value.

Line 3b(ii) - Longitude

State the longitude coordinates. Include plus (+) or minus (-) sign in the first box, as applicable.

Line 4 - Date Construction Began

Enter the date construction of the qualified refueling property began. The construction start date must be determined using one of the IRS-approved methods for establishing the beginning of construction.

- The Physical Work Test

- The Five Percent Safe Harbor method

Line 5 - Date Placed in Service

- Enter the date the refueling property was placed in service.

- Generally, property is considered placed in service when it is ready and available for its intended use, regardless of whether it is actively being used on that date.

Line 6 - Eligible Census Tract Information

Line 6 is used to determine whether the refueling property is located in an eligible census tract.

Line 6a - Eligible Census Tract

Check the appropriate box to indicate whether the property is located in an eligible census tract.

To determine eligibility, use the property's address or geographic coordinates to identify its census tract and verify that the tract is included in the IRS list of eligible census tracts.

Line 6b - Census Tract GEOID

If the property is located in an eligible census tract, enter the applicable 11-digit census tract GEOID.

Line 7 - Certification or Permit Number

Enter the certification number, permit number, or both, issued by a state or local government for the refueling property, if applicable.

This information helps verify that the property complies with applicable state or local safety requirements. If no certification or permit number is required for the property, leave Line 7 blank.

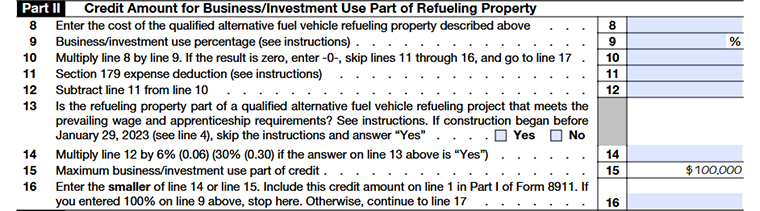

Part II - Credit Amount for Business/Investment Use Part of Refueling Property

Line 8 - Cost of Qualified Refueling Property

Enter the total cost of the qualified alternative fuel vehicle refueling property described on Schedule A.

Line 9 - Business/Investment Use Percentage

Enter the percentage of business or investment use for the refueling property.

- Enter 100% if the property is used entirely for business or investment purposes.

- If the property is used for both business and personal purposes, enter only the percentage attributable to business or investment use.

If the property's use changes during the tax year from personal use to business/investment use, or vice versa, determine the business/investment use percentage based on the portion of the year the property was used for business or income-producing activities.

Line 10 - Business/Investment Use Cost

- Multiply Line 8 by Line 9 and enter the result on Line 10. This amount represents the portion of the property's cost attributable to business or investment use.

- If the result is zero, enter 0 on Line 10, skip Lines 11 through 16, and proceed directly to Line 17.

Line 11 - Section 179 Expense Deduction

Enter any Section 179 expense deduction claimed for the qualified refueling property on Form 4562, Part I.

Line 12 - Adjusted Property Cost

Subtract Line 11 from Line 10 and enter the result on Line 12.

Line 13 - Prevailing Wage and Apprenticeship (PWA) Requirements

- Indicate whether the qualified alternative fuel vehicle refueling project meets the applicable Prevailing Wage and Apprenticeship (PWA) requirements by checking “Yes” or “No.”

- Projects that satisfy the PWA requirements may qualify for an increased credit rate.

- If construction of the refueling property began before January 29, 2023, check Yes on Line 13 without applying the PWA requirements.

- Taxpayers claiming the increased credit amount based on compliance with the PWA requirements must file a separate Form 7220, Prevailing Wage and Apprenticeship (PWA) Verification and Corrections, for each qualified refueling property.

Line 14 - Credit Calculation

Multiply Line 12 by:

- 6% (0.06) if the property does not meet the PWA requirements, or

- 30% (0.30) if the property meets the PWA requirements.

Enter the result on Line 14.

Line 15 - Maximum Credit Limit

The maximum credit allowed for the business or investment-use portion of a qualified refueling property is $100,000.

Line 16 - Allowed Business/Investment Use Credit

- Enter the smaller value between Line 14 and Line 15. Include this amount on Line 1 of Form 8911.

- If you enter 100% on Line 9, stop here. Otherwise, continue to Line 17.

Part III - Credit Amount for Personal Use Part of Refueling Property

Line 17 - Property Installed at Your Main Home

Indicate whether the qualified refueling property was installed on property used as your main home.

- Select “Yes” if the property was installed at your main residence and continue to Line 18.

- Select “No” if the property was not installed at your main residence.

Refueling property that is not installed on property used as your main home does not qualify for the personal-use portion of the credit.

Line 19 - Personal-Use Credit Calculation

Multiply Line 18 by 30% (0.30) and enter the result on Line 19.

Line 20 - Maximum Personal-Use Credit

The maximum credit allowed for the personal-use portion of a qualified refueling property is $1,000.

Line 21 - Allowed Personal-Use Credit

- Enter the smaller value from either Line 19 or Line 20. This amount is the allowable personal-use credit for the property.

- Include this amount on Line 4 in Part II of Form 8911

Commonly Asked Questions

1. What qualifies as alternative fuel vehicle refueling property?

Alternative fuel vehicle refueling property includes equipment for charging electric vehicles, hydrogen fuel cell stations, and natural gas refueling installations that meet IRS eligibility criteria.

2. What is considered as a fuel cell property?

A Fuel cell property is an equipment that uses fuel cell technology to generate electricity through a chemical reaction rather than by burning fuel. To qualify for a tax credit, the property must meet applicable IRS requirements and performance standards.

3. How does Form 8911 apply to electric vehicles?

4. What is the maximum credit amount available on Form 8911?

- Business or investment-use property: Up to $100,000 per qualified property.

- Personal-use property installed at your main home: Up to $1,000 per qualified property.