Form 4562 Depreciation and Amortization

Introduction

IRS Form 4562 is used to report Depreciation and Amortization deductions for business property placed in service during the tax year. It is also used to claim Section 179 deductions, special depreciation allowances, and expenses related to the business use of vehicles and other listed property.

For tax-exempt organizations filing Form 990-T, Form 4562 plays an important role in reporting depreciation expenses related to unrelated business income activities, which may directly affect the organization’s taxable income and overall tax liability.

This resource guide explains the purpose of Form 4562, who must file it, the deductions it covers, and other important filing requirements businesses and tax-exempt organizations should understand.

Table of Contents

What’s New?

For the 2025 tax year, the IRS has updated Form 4562 with several important changes related to depreciation reporting, Section 179 deductions, and bonus depreciation rules.

- New lines 19h and 20e were added to report 50-year property depreciation under General Depreciation System (GDS) and Alternative Depreciation System (ADS) methods.

- Line 23 is now split into lines 23a and 23b for reporting Section 263A capitalized costs.

- A new line 24c was added for taxpayers claiming depreciation on aircraft.

- The Section 179 deduction limit increased to $2,500,000,with a $4,000,000 phase-out threshold. The SUV deduction limit is now $31,300.

- The One Big Beautiful Bill Act reinstated 100% bonus depreciation for certain qualified property acquired after January 19, 2025.

- New rules also apply to qualified production property, solar and wind energy property, and domestic and foreign research expenditures.

What is Form 4562?

Form 4562is an IRS tax form used to claim depreciation and amortization deductions for business assets and certain intangible property. Businesses and tax-exempt organizations use this form to report depreciation on assets such as buildings, machinery, vehicles, equipment, computers, and other propertyused in business activities.

The form is also used to amortize intangible assets, including goodwill, patents, copyrights, start-up costs, and research-related expenses. In addition, Form 4562 allows taxpayers to claim Section 179 expense deductions, bonus depreciation, and depreciation deductions calculated under the Modified Accelerated Cost Recovery System ( MACRS).

By filing 4562 form, taxpayers can determine allowable deductions for qualifying property and reduce their overall taxable income.

Who must file Form 4562?

Form 4562 is used to report depreciation and amortization deductions for assets used in a business or to produce income.

You may need to file Form 4562 if you:

- Own a business or are self-employed

- Own rental property

- Operate a corporation or partnership

- Represent a trust, estate, or certain tax-exempt organization

The form is used to report depreciation on assets such as machinery, equipment, buildings, vehicles, computers, and rental property. It is also required for taxpayers claiming Section 179 deductions, bonus depreciation, or amortization of qualifying intangible assets and business-related costs.

Organizations filing the 990-T form may need to file Form 4562 to report depreciation expenses connected to unrelated business income activities.

Complete and file Form 4562 if you are claiming:

- Depreciation for property placed in service during the 2025 tax year

- A Section 179 expense deduction, including any carryover from prior years

- Depreciation for vehicles or other listed property

- Vehicle expense deductions reported on forms other than Schedule C (Form 1040)

- Depreciation on a corporate income tax return, other than Form 1120-S

- Amortization of costs that begin during the 2025 tax year

Generally, a separate 4562 form should be filed for each business or activity that requires depreciation or amortization reporting.

Ready to attach Form 4562 along with your 990-T return with TaxZerone?

Make the e-filing process simple by clicking the button below.

How to file Form 4562?

Form 4562 “Depreciation and Amortization (Including Information on Listed Property)” and is attached to your tax return to report depreciation, amortization, Section 179 deductions, and business-use property information. Taxpayers must enter the following basic details at the top of the form:

Name(s) shown on return

Enter the name exactly as it appears on the related tax return. This may be an individual name, business name, corporation, partnership, trust, or organization name.

Business or activity to which this form relates

Provide the specific business activity or operation connected to the depreciation or amortization being claimed.

Identifying number

Enter the taxpayer identification number associated with the return, such as a Social Security Number (SSN), Employer Identification Number (EIN), or Individual Taxpayer Identification Number (ITIN).

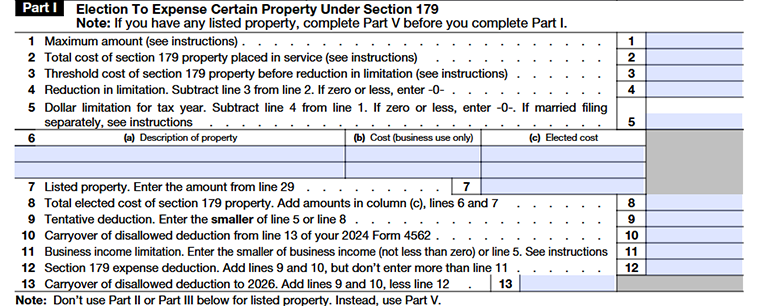

Part I-Election to Expense Certain Property Under Section 179

Line 1 - Maximum Amount

- For tax year 2025, the maximum Section 179 expense deduction is $2,500,000 for eligible Section 179 property, including qualified real property placed in service during the year.

- Taxpayers may use Worksheet 1 in the IRS instructions to calculate the allowable deduction amount. If the property is not used more than 50% for business purposes before the end of its recovery period, the previously claimed Section 179 deduction may need to be recaptured and reported as other income.

- Additional recapture rules may apply to certain disaster assistance property and other specially designated property if it no longer meets the required usage or location conditions

Line 2 - Total Cost

Enter the total cost of all Section 179 property placed in service during the 2025 tax year, including qualified real property elected to be treated as Section 179 property.

- Listed property reported in Part V

- Property placed in service by your spouse, even if filing separately

Line 3 - Threshold Cost

The Section 179 deduction begins to phase out if the total cost of qualifying Section 179 property placed in service during 2025 exceeds $4,000,000.

For partnerships and S corporations, these limits apply both at the entity level and the individual partner or shareholder level. Controlled group members are treated as a single taxpayer when applying these limitations.

Line 4 - Reduction Limit

Subtract Line 3 from Line 2 to calculate the reduction in the Section 179 deduction limit. If the result is zero or less, enter “0.”

Line 5 – Dollar Limitation

- Enter the remaining Section 179 deduction available after applying any phase-out reduction on this line.

- If the amount on Line 5 is zero, no Section 179 deduction can be claimed for the current tax year. In that case, skip Lines 6 through 11, enter zero on Line 12, and report any allowable carryover deduction from 2024 on Line 13.

- Taxpayers filing separately as married individuals must allocate the Section 179 deduction limit between spouses, either equally or based on an agreed percentage allocation totaling 100%.

Line 6 - Business Income Limitation

Enter the Section 179 expense deduction elected for qualifying business property. Do not include listed property on this line. Listed property, such as certain vehicles and other assets reported in Part V, must be entered separately on Line 26, column (i).

Column (a) – Description of Property

Enter a brief description of the property for which the Section 179 deduction is being claimed.

Column (b) – Cost

Enter the business-use cost of the property. If the asset was acquired through a trade-in, include only the excess amount paid over the value of the traded property. Do not include any carryover basis from the exchanged asset.

Column (c) – Elected Cost

Enter the amount of the property cost you choose to expense under Section 179. Any remaining amount not claimed under Section 179 may still qualify for depreciation using MACRS or other applicable depreciation methods.

If you are reporting a Section 179 deduction received from a partnership or S corporation, enter “From Schedule K-1 ( Form 1065 )” or “From Schedule K-1 (Form 1120-S) ” across columns (a) and (b).

Line 7 - Current Year Deduction

Enter the amount elected for listed property from Line 29. Listed property generally includes certain vehicles and other assets used for both personal and business purposes. Additional details for listed property reporting can be found in Part V of Form 4562.

Line 8 - Total Elected Expense Deduction

Add the amounts reported in column (c) of Lines 6 and Line 7. This total represents the combined Section 179 expense deduction elected for all qualifying property during the tax year.

Line 9 - Tentative Deduction

Enter the smaller amount between Line 5 and Line 8. This amount represents the tentative deduction before applying business income limitations.

Line 10 - Carryover From Prior Year

Enter any Section 179 deduction carryover from 2024 that was not allowed because of the business income limitation. If you filed Form 4562 for 2024, use the amount reported on Line 13 of that return.

This carryover allows taxpayers to claim previously disallowed Section 179 deductions in future tax years if sufficient business income is available.

Line 11 - Business Income Limitation

The Section 179 deduction cannot exceed taxable income earned from the active conduct of a trade or business during the tax year. Taxpayers are considered to actively conduct a business only if they meaningfully participate in its operations or management. Passive investors generally do not qualify.

The calculation for this limitation varies depending on the type of taxpayer:

- Individuals generally, the limitation is based on taxable income earned from actively participating in a trade or business, including certain wages and compensation received as an employee.

- Partnerships must use the partnership’s active trade or business income and expense items under Section 702(a).

- S corporations must calculate the limitation based on active business income reported under Section 1366(a).

- Corporations other than S corporations must use taxable income before applying Section 179 deductions, net operating losses, and special deductions.

The allowable deduction is the smaller of the business income limitation or the amount on Line 5.

Line 12 - Allocated Section 179 Deduction

- The limits apply to the taxpayer as a whole, rather than separately to each business activity. Taxpayers with multiple businesses may allocate the allowable Section 179 deduction among different activities.

- To do this, prepare a separate Form 4562 marked “Summary” in Part I to report the combined totals from all businesses or activities. Then, enter the allocated deduction amount on Line 12 of each separate Form 4562 prepared for individual businesses or activities

Line 13 - Section 179 Carryover to 2026

To calculate the deduction carryover to 2026, add the amounts from Lines 9 and 10, then subtract the amount on Line 12.

Part II-Special Depreciation Allowance and Other Depreciation

Line 14 - Special Depreciation Allowance

Report the special depreciation allowance (bonus depreciation) for qualified property placed in service during the tax year. This deduction is claimed after any Section 179 deduction and before calculating regular MACRS depreciation.

For 2025, certain qualified property may be eligible for 100% bonus depreciation. Eligible assets generally include:

- Tangible business property with a recovery period of 20 years or less

- Qualified computer software

- Water utility property

- Certain film, television, theatrical, and sound recording productions

- Certain plants bearing fruits and nuts

- Qualified production property

Some property acquired before January 20, 2025, may qualify for a reduced 40% or 60% bonus depreciation rate.

Taxpayers can also elect out of bonus depreciation for a specific class of property by attaching a statement to the tax return.

Line 15 - Other Depreciation

Enter depreciation expenses calculated using non-MACRS methods, including the unit-of-production method and other approved depreciation methods.

Taxpayers must attach a separate statement describing the property, depreciation method used, and adjusted depreciable basis after applying deductions, credits, and bonus depreciation adjustments.

Line 16 - Depreciation for Special Property

Report depreciation for property subject to special depreciation rules or older recovery systems. This may include:

- Property placed in service before 1981

- ACRS property

- Certain films, sound recordings, and videotapes

- Property using the income forecast method

- Certain intangible assets and computer software

- Patents, copyrights, and mortgage servicing rights

The total depreciation claimed cannot exceed the adjusted depreciable basis of the property.

Part III-MACRS Depreciation

Section-A

Line 17 - MACRS Depreciation for Prior-Year Property

- Line 17 is used to report current-year depreciation deductions for tangible property placed in service before 2025 and depreciated under MACRS.

- The depreciation deduction is calculated based on the asset’s recovery period, depreciation method, and applicable convention under MACRS rules.

- These rules are especially important when reporting partial asset dispositions or property improvements.

Line 18 – General Asset Account Election

Elect a General Asset Account (GAA) under MACRS to group similar business assets and depreciate them as a single account rather than tracking each asset separately.

Assets included in the same account must:

- Be placed in service during the same tax year

- Use the same depreciation method

- Have the same recovery period and convention

Assets used for both personal and business purposes cannot be included in a General Asset Account.

When an asset within the account is sold or disposed of, the overall depreciation basis and reserve of the account generally remain unchanged, and the amount received is usually treated as ordinary income.

Special rules may apply to passenger automobiles, foreign-use property, personal-use conversions, and like-kind exchanges.

To make the election, check the box on Line 18 and file the return on time, including extensions. Once made, the election is generally irrevocable.

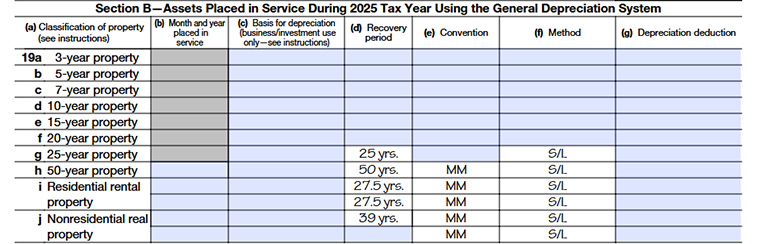

Section B-Assets Placed in Service During 2025 Tax Year Using the General Depreciation System

Section B applies to property acquired through a like-kind exchange or involuntary conversion, such as property replaced after theft, casualty, or condemnation.

In most cases, the carryover basis of the acquired property must continue to be depreciated using:

- The same depreciation method

- The same convention

- The remaining recovery period of the old property

If additional money is paid as part of the exchange, that excess basis is treated as new property and depreciated separately.

Taxpayers may also elect out of these rules and instead treat the old property as disposed of at the time of the exchange. In that case, the replacement property is treated as newly placed in service on the acquisition date and depreciated accordingly.

Lines 19 - MACRS Depreciation Under GDS

Lines 19a through 19j of Form 4562 are used to report depreciation for assets placed in service during the 2025 tax year under the General Depreciation System (GDS) of MACRS.

These lines apply to most business property except automobiles and other listed property reported in Part V.

Each line represents a different property classification based on the asset’s recovery period.

Column (a)- Classification of Property

Enter the correct MACRS classification based on the type of property and applicable recovery period.

The classification determines the depreciation method and recovery period used to calculate depreciation.

Column (b)- Month and Year Placed in Service

Enter the month and year the property was placed in service and ready for business use.

If property converted from personal use to business use, enter the conversion date.

Column (c)- Basis for Depreciation

Enter the business or investment-use portion of the property’s cost or adjusted basis.

Reduce the basis by:

- Section 179 deductions

- Bonus depreciation

- Energy-related deductions and credits

- Other applicable basis adjustments

Only the remaining adjusted basis is used for depreciation calculations.

Column (d)- Recovery Period

Enter the applicable recovery period for the asset based on IRS MACRS classifications.

Column (e)- Convention

Enter the applicable depreciation convention used for the property. The convention determines how much depreciation is allowed in the first and final year.

The three main conventions are:

- HY (Half-Year Convention)

- MQ (Mid-Quarter Convention)

- MM (Mid-Month Convention)

Most business property uses the half-year convention unless the mid-quarter rules apply.

Column (f)- Method

Enter the depreciation method used for the property.

Common methods include:

- 200 DB – 200% Declining Balance

- 150 DB – 150% Declining Balance

- S/L – Straight-Line Method

The applicable method depends on the property classification and IRS rules.

Column (g)- Depreciation Deduction

Enter the allowable current-year depreciation deduction for the property.

The deduction is calculated using:

- Adjusted depreciable basis

- Recovery period

- Convention

- Depreciation method

- Applicable IRS depreciation tables or formulas

If property was sold or disposed of during the year, special depreciation calculation rules may apply.

Line 19a

Report depreciation for assets classified as 3-year property under MACRS.

Examples may include:

- Certain racehorses

- Qualified rent-to-own property

- Certain livestock assets

These assets are generally depreciated over a 3-year recovery period using the applicable MACRS depreciation method.

Line 19b

Report depreciation for assets classified as 5-year property under MACRS.

Common examples include:

- Automobiles

- Computers and office equipment

- Copiers and calculators

- Appliances and furniture used in rental activities

- Certain farming machinery and equipment

Most 5-year property uses the 200% declining balance method unless another method is elected.

Line 19c

Report depreciation for assets classified as 7-year property under MACRS.

Examples include:

- Office furniture

- Office equipment

- Railroad track

- Certain agricultural machinery and fencing

These assets are generally depreciated over 7 years under MACRS rules.

Line 19d

Report depreciation for assets classified as 10-year property under MACRS.

This may include:

- Vessels and barges

- Certain agricultural or horticultural structures

- Trees and vines bearing fruits or nuts

- Certain smart electric property

These assets are depreciated over a 10-year recovery period.

Line 19e

Report depreciation for assets classified as 15-year property under MACRS.

Examples include:

- Qualified improvement property

- Municipal wastewater treatment plants

- Telephone distribution property

- Certain land improvements and utility property

These assets generally use the 150% declining balance depreciation method.

Line 19f

Line 19f is used to report depreciation for 20-year property.

Examples include:

- Farm buildings

- Certain municipal sewer systems

- Utility land improvements

These assets are depreciated over a 20-year recovery period.

Line 19g

Report depreciation for qualifying water utility property with a 25-year recovery period under MACRS.

This includes property used in:

- Water collection

- Water treatment

- Commercial water distribution systems

- Certain municipal sewer systems

These assets are depreciated over 25 years.

Line 19h

Report depreciation for qualifying 50-year property under the General Depreciation System (GDS).

This generally includes railroad grading and tunnel bore improvements used for railroad track construction or improvement.

Line 19i

Line 19i is used to report depreciation for residential rental property where at least 80% of the rental income comes from dwelling units.

Residential rental buildings are generally depreciated over 27.5 years using the straight-line method and mid-month convention.

Line 19j

Report depreciation for nonresidential real property, such as office buildings, retail stores, warehouses, and other commercial properties.

These properties are generally depreciated over 39 years using the straight-line method and mid-month convention.

Section C-Assets Placed in Service During 2025 Tax Year Using the Alternative Depreciation System

Line 20 - MACRS Depreciation Under ADS

Lines 20a through 20e of Form 4562 are used to report depreciation for assets placed in service during the 2025 tax year and depreciated under the Alternative Depreciation System (ADS).

ADS generally uses the straight-line depreciation method over a longer recovery period compared to GDS.

Property that must generally be depreciated under ADS includes:

- Property used predominantly outside the United States

- Tax-exempt use property

- Tax-exempt bond financed property

- Certain imported property

- Certain farming business property

- Property held by an electing real property trade or business

- Certain property held by an electing farming business

Taxpayers may also elect to use ADS instead of GDS for certain property classifications by completing Section C.

Line 20a

- Report depreciation for assets placed in service during the 2025 tax year that are depreciated under the Alternative Depreciation System (ADS) and have an established class life.

- Under ADS, depreciation is generally calculated using the straight-line method over the asset’s ADS recovery period. Property reported on this line may include business equipment, machinery, or other assets with a defined class life under IRS rules.

Line 20b

This line applies to property depreciated under the Alternative Depreciation System (ADS) that does not have a specific IRS-assigned class life and must be depreciated using the applicable ADS recovery period.

Line 20c

- Line 20c is used to report ADS depreciation for residential rental property.

- Residential rental property placed in service after 2017 generally uses a 30-year ADS recovery period. This line is commonly used by electing real property trades or businesses required to depreciate rental property under ADS.

Line 20d

Report ADS depreciation for nonresidential real property, such as office buildings, retail stores, and warehouses.

Line 20e

Report ADS depreciation for water utility property and railroad grading or tunnel bore property.

MACRS Recapture

If MACRS property is later sold, exchanged, or disposed of, part of the gain may need to be reported as ordinary income through depreciation recapture.

Recapture may include:

- Section 179 deductions claimed on the property

- Special depreciation allowance claimed

- Certain environmental compliance deductions

Generally, residential rental property and nonresidential real property are not subject to recapture unless special depreciation allowance was claimed on the property.

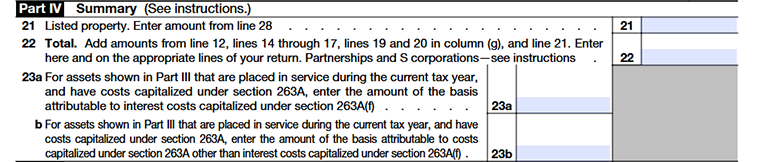

Part IV-Summary

Line 21 - Total MACRS and Other Depreciation

- Enter the total depreciation deduction for listed property from line 28.

- Listed property generally includes assets such as vehicles, computers, and other property used for both business and personal purposes. The amount entered on this line should match the total calculated in Part V.

Line 22 - Listed Property and Other Property Total

- Line 22 is used to report the total depreciation and Section 179 deduction claimed for the current tax year.

- Partnerships and S corporations should not include the Section 179 deduction amount from line 12 on this line. Instead, the deduction is separately passed through to partners or shareholders on Schedule K-1.

Lines 23 - Capitalized Costs

Lines 23a and 23b are used by taxpayers subject to the uniform capitalization rules under Section 263A. These rules require certain direct and indirect costs related to property production or acquisition to be added to the asset’s basis instead of being immediately deducted.

These lines apply to assets reported in Part III that were placed in service during the current tax year.

Line 23a

- Enter the increase in basis related to interest costs that must be capitalized under Section 263A(f).

- This generally applies to businesses that are required to capitalize interest expenses connected to the production of certain property.

Line 23b

Enter the increase in basis from other capitalized costs required under Section 263A, excluding interest costs reported on line 23a.

These costs may include certain production, construction, storage, handling, or indirect business expenses that must be added to the basis of the asset.

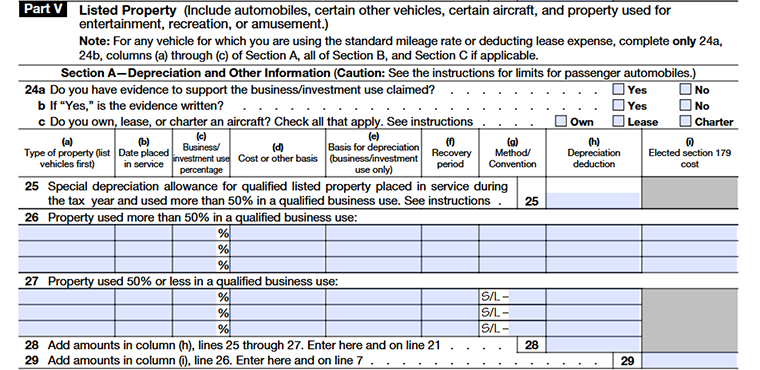

Part V-Listed Property

Section A is used to provide details about listed property and its business use percentage.

The IRS requires taxpayers to maintain proper records supporting the business use of listed property, especially for vehicles and mixed-use assets.

Line 24 – Business Use Evidence and Aircraft Information

Provide information about the records and documentation supporting the business use of listed property.

Line 24a

Indicate whether you have evidence supporting the business or investment use claimed for the listed property.

Line 24b

If you answered “Yes” on line 24a, line 24b asks whether the supporting evidence is written.

Line 24c

- Line 24c is used to indicate whether you owned, leased, or chartered an aircraft during the tax year. Check all applicable boxes based on how the aircraft was used.

- This information helps determine whether the aircraft qualifies business-use depreciation and other deductions under IRS rules for business aircraft.

Line 25 - Special Depreciation Allowance

- Line 25 is used to report the total special depreciation allowance claimed for qualified listed property placed in service during the tax year.

- This may include certain qualified property acquired after January 19, 2025, as well as certain qualified property acquired after September 27, 2017, and before January 20, 2025.

- The special depreciation allowance is subject to the overall depreciation and Section 179 deduction limits applicable to passenger automobiles, trucks, and vans.

Line26 - Depreciation for Listed Property Used More Than 50%

Use Line 26 to report depreciation for listed property used more than 50% for qualified business purposes during the tax year. Property reported on this line may qualify for the Section 179 expense deduction and special depreciation allowance, subject to IRS limitations.

A qualified business use generally includes property used directly in your trade or business. However, the following uses are not considered qualified business use:

- Investment use,

- Personal use,

- Certain related-party or employee use not properly reported as taxable income, and

- Non-deductible use under Section 274.

For business aircraft, taxpayers must satisfy both the 50% business-use test and the 25% qualified business-use test to claim accelerated depreciation or bonus depreciation. Proper records must be maintained to support business travel and usage.

Column (a) - Type of Property

Enter the make, model, or description of each listed property item, such as vehicles or other listed assets.

Column (b) - Date Placed in Service

Enter the date the property was first used for business purposes.

Column (c) - Business/Investment Use Percentage

Enter the percentage of business use based on mileage, time used, or other appropriate usage methods.

Column (d) - Cost or Other Basis

Enter the original cost or adjusted basis of the property, including sales tax.

Column (e) - Basis for Depreciation

Enter the depreciable business-use basis after reductions for credits, Section 179 deductions, or special depreciation allowances.

Column (f) - Recovery Period

Enter the applicable MACRS recovery period based on the property classification.

Column (g) - Method/Convention

Enter the depreciation method and convention used, such as 200 DB, 150 DB, S/L, HY, MQ, or MM.

Column (h) - Depreciation Deduction

Enter the allowable depreciation deduction for the current year, subject to passenger automobile limitations.

Column (i) - Elected Section 179 Cost

Enter the amount elected under Section 179 for qualifying property used more than 50% in business.

Line 27 - Depreciation for Listed Property Used 50% or Less

Use Line 27 to report depreciation for listed property used 50% or less in a qualified business use during the tax year. Property reported on this line does not qualify for the Section 179 expense deduction or special depreciation allowance.

Such property must generally be depreciated using the straight-line method under the Alternative Depreciation System (ADS).

Columns (a) through (h) are completed in the same manner as Line 26 . However, the following special rules apply:

- Property used 50% or less for qualified business purposes must be depreciated using the ADS straight-line method.

- The depreciation deduction is generally calculated by dividing the depreciable basis by the ADS recovery period.

- Passenger automobile depreciation limits continue to apply.

Line 28 - Total Listed Property Depreciation

Add the depreciation amounts reported in column (h) for lines 25 through 27. Enter the total on this line and also report it on Line 21.

Line 29 - Total Deduction for Listed Property

Add the Section 179 expense amounts reported in column (i) on Line 26 . Enter the total on this line and also report it on Line 7.

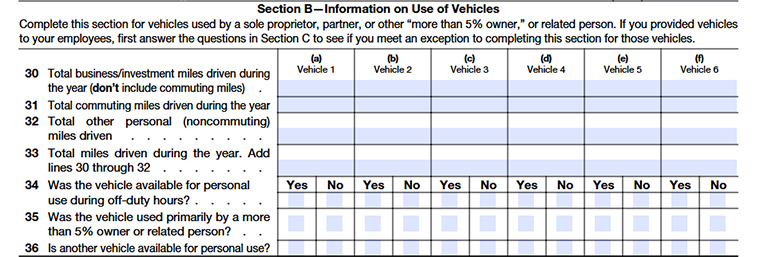

Section B-Information on Use of Vehicles

Complete Lines 30 through 36 for each vehicle listed in Section A, unless an exception applies. Employees must provide this information to employers for any employer-provided vehicle used during the tax year.

Complete Lines 30 through 36 for each vehicle listed in columns (a) through (f). Each column represents a separate vehicle.

Exception: Employers do not need to complete Lines 30-36 for vehicles used by employees who are not more than 5% owners or related persons if any question on Lines 37 through 41 is answered “Yes.”

Line 30 - Total Business/Investment Miles

- Enter the total number of miles driven during the year for business or investment purposes.

- Do not include commuting miles.

Line 31 - Total Commuting Miles

Enter the total miles driven between home and work during the tax year. These miles are considered commuting miles and are not treated as business use.

Line 32 - Total Personal Noncommuting Miles

Enter the total personal miles driven during the year that are not commuting miles.

Line 33 - Total Miles Driven During the Year

Enter the total miles driven during the year for all purposes by adding Line 30 through Line 32.

Line 34 - Vehicle Available for Personal Use

Indicate whether the vehicle was available for personal use during off-duty hours.

Line 35 - Vehicle Used by 5% Owner or Related Person

Check whether the vehicle was primarily used by a person who owns more than 5% of the business or by a related person.

Line 36 - Availability of Another Personal Vehicle

Indicate whether another vehicle was available for personal use during the tax year.

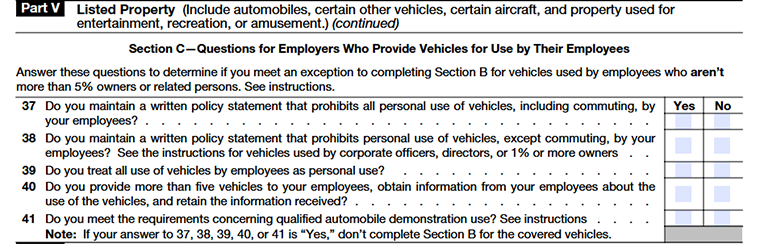

Section C-Questions for Employers Who Provide Vehicles for Use by Their Employees

Employers can satisfy the vehicle substantiation requirements under IRC Section 274(d) by maintaining a written policy that either:

- Prohibits all personal use of employer-provided vehicles, including commuting, or

- Prohibits personal use except for commuting

When these policy requirements are properly met, employees generally are not required to maintain separate mileage records for those vehicles.

Line 37 - Policy Prohibiting Personal Use

Check “Yes” if the employer maintains a written policy that completely prohibits personal use of the vehicle, including commuting.

The policy must meet all of the following conditions:

- The employer owns or leases the vehicle for business use

- The vehicle is normally kept at the employer’s business premises when not in use

- Employees using the vehicle do not live at the business location

- Personal use is prohibited except for minimal incidental use

- The employer reasonably believes employees are not using the vehicle personally beyond minimal use.

LLine 38 - Policy Allowing Commuting Only

Check “Yes” if the employer maintains a written policy that prohibits personal use of the vehicle except for commuting. This rule does not apply if the employee using the vehicle is an officer, director, or 1% or greater owner.

To qualify, the policy must meet all of the following conditions:

- The employer owns or leases the vehicle for business use

- The employee is required to commute in the vehicle for valid business reasons

- Personal use other than commuting or minimal incidental use is prohibited

- The employer reasonably believes the vehicle is not used personally beyond commuting

- The employer includes the value of commuting use in the employee’s taxable income

Line 39 - Employee Vehicle Use Treated as Personal Use

Indicate whether the employer treats all employee use of company-provided vehicles as personal use for tax reporting purposes.

Line 40 - Exception for Employers With More Than Five Vehicles

Employers providing more than five vehicles to employees who are not 5% owners or related persons are not required to complete Section B for those vehicles.

Instead, employers must:

- Obtain the required vehicle-use information from employees, and

- Retain those records for tax documentation purposes

Line 41 - Qualified Demonstration Use Vehicles

Check “Yes” if the vehicle qualifies for demonstration use under a written employer policy.

The policy must:

- Restrict vehicle use to full-time automobile salespersons

- Prohibit personal vacation use

- Prohibit storing personal belongings in the vehicle

- Limit mileage outside normal working hours

Part VI-Amortization

Part VI is used to claim Amortization deductions for certain capital expenses that are recovered gradually over a fixed number of years instead of being deducted all at once.

Attach any statements or supporting information required under the applicable IRS Code sections and regulations when making an amortization election.

Column (a) – Description of Costs

Enter a description of the costs being amortized. Common examples include:

- Geological and Geophysical Costs – Section 167(h)

- Pollution Control Facilities – Section 169

- Bond Premium – Section 171

- Research and Experimental Expenditures – Sections 174 and 174A

- Lease Acquisition Costs – Section 178

- Reforestation Costs – Section 194

- Optional Write-Off of Tax Preference Items – Section 59(e)

- Section 197 Intangibles

- Startup and Organizational Costs

- Creative Property Costs

Column (b) – Date Amortization Begins

- Enter the date the amortization period starts based on the applicable IRS Code section.

- For pollution control facilities, the amortizable amount must be reduced by any special depreciation allowance claimed on line 14 for that property.

Column (c) – Amortizable Amount

Enter the total amount eligible for amortization after applying any required adjustments or limitations.

Column (d) – Code Section

Enter the applicable IRS Code section authorizing the amortization deduction, such as:

- Section 167

- Section 169

- Section 174

- Section 197

- Section 195

reframe

Column (e) - Amortization Period or Percentage

Enter the applicable amortization period or the percentage used to calculate the amortization deduction for the cost being amortized. The period or percentage depends on the specific IRS Code section that applies to the expense.

Column (f) – Amortization Deduction for the Year

Calculate the current-year amortization deduction by using either of the following methods:

- Divide the amount in column (c) by the total number of months in the amortization period, then multiply it by the number of months applicable to the 2025 tax year, or

- Multiply the amount in column (c) by the applicable percentage shown in column (e).

Line 42 - Current-Year Amortizable Costs

Complete Line 42 only for amortizable costs whose amortization period begins during the tax year starting in 2025.

Line 43 - Prior-Year Amortization Reporting

If you are claiming amortization for costs that began before the 2025 tax year-other than research or experimental expenditures-and you are not otherwise required to file IRS tax form 4562, report the deduction directly on the “Other Deductions” or “Other Expenses” line of your return instead of filing Form 4562.

Under Revenue Procedure 2025-28, taxpayers may elect to deduct the remaining unamortized domestic research expenditures in full or amortize them over a 2-year period beginning after December 31, 2024. Any election made must be reported on Line 43 with the required supporting statement.

For foreign research expenditures under Section 174, attach a statement showing the amount being amortized over the required 15-year period and report the deduction on Line 43.

Line 44 - Total Amortization Deduction Reporting

Enter the total amortization deduction for the year, including current-year and prior-year amortization, research expenditure amortization, and allowable reforestation amortization in column(f).

Report the total on the appropriate “Other Deductions” or “Other Expenses” line of your tax return.

Commonly Asked Questions

1. What is the difference between depreciation and amortization?

2. What is the Modified Accelerated Cost Recovery System (MACRS) on Form 4562?

MACRS is the most common method of depreciation used on Form 4562. It allows for faster depreciation of property in the early years of its useful life, which can lead to larger deductions and tax savings upfront.

Under MACRS, all assets are divided into classes which dictate the number of years over which an asset's cost will be recovered. Each MACRS class has a predetermined schedule that determines the percentage of the asset's costs which is depreciated each year.