Schedule K-1 (Form 1065): The Complete Resource Guide for Partners & Tax Professionals

Schedule K-1 (Form 1065) is a federal tax document issued by partnerships to each partner at the end of the tax year. It reports each partner's allocated share of the partnership's income, deductions, credits, and other tax items. Rather than paying taxes at the entity level, partnerships pass their financial results through to individual partners — a structure known as pass-through taxation. The Schedule K-1 is the mechanism that makes this possible.

Whether you're a general partner managing day-to-day operations or a limited partner who simply invested capital, you'll receive a K-1 if you hold any ownership interest in a partnership that filed Form 1065 with the IRS.

Table of Contents

What’s New for Schedule K-1

The IRS has made the following changes to Schedule K-1 (Form 1065)

Box 13 Code X – Extra Deduction for Production Expenses

Qualified sound recording production expenses can now be reported in Box 13, Code X, in addition to qualified film and television production expenses. This change allows eligible partnerships to pass through these deductible expenses to partners.

Box 19 – More transparent distribution reporting

The IRS has updated the instructions for Box 19 to clarify the reporting of different partnership distributions with separate codes. Partners can more easily identify the type of distribution they receive.

Box 20, Code ZZ – New Farmland Tax Election

In Box 20, a new code ZZ has been added for certain sales of qualified farmland to qualified farmers. Eligible partners can elect to pay the tax due on such gains in four equal annual installments rather than in one year.

Who Must File Form 1065 and Issue K-1s?

Any domestic partnership — including general partnerships, limited partnerships (LPs), limited liability partnerships (LLPs), and most multi-member LLCs taxed as partnerships — must file Form 1065 annually. As part of that filing, the partnership is required to prepare and distribute a Schedule K-1 to each partner, as well as submit copies to the IRS.

Entities that issue Schedule K-1 (Form 1065) include:

- General partnerships — Traditional business arrangements where all partners share management responsibilities and liability.

- Limited partnerships (LPs) — Structures with at least one general partner and one or more limited partners.

- Limited liability partnerships (LLPs) — Common among law firms, accounting firms, and medical practices.

- Multi-member LLCs (taxed as partnerships) — LLCs with two or more members that have not elected to be taxed as a corporation.

Single-member LLCs, S corporations, and trusts/estates use different K-1 variants — Schedule K-1 for Form 1120-S and Form 1041, respectively.

Why Schedule K-1 Matters for Partners

The K-1 is more than just an informational form — it directly affects each partner's personal tax return. Here's why it matters:

- Pass-through taxation: The partnership itself does not pay federal income tax. Instead, profits and losses "pass through" to partners, who report them on their individual returns (Form 1040), business returns, or corporate returns, depending on the partner's entity type.

- Self-employment tax: For general partners, guaranteed payments and certain ordinary income items from the K-1 may be subject to self-employment tax.

- Passive activity rules: Limited partners and certain LLC members must apply passive activity loss rules to income and losses reported on their K-1.

Line-by-Line Instructions for Schedule K-1 (Form 1065)

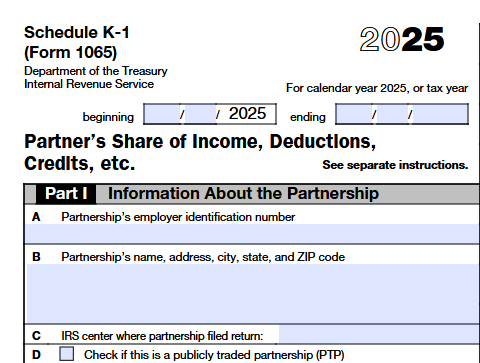

Part I – Information About the Partnership

Item A – Partnership's Employer Identification Number (EIN)

Enter the partnership's 9-digit Employer Identification Number (EIN) assigned by the IRS. Ensure the EIN matches the one reported on Form 1065.

Item B – Partnership's Name and Address

Enter the partnership's legal name and complete mailing address, including the city, state, and ZIP code. This information should match the partnership's tax return.

Item C – IRS Center Where Partnership Filed Return

Enter the IRS service center where the partnership filed Form 1065. This identifies the IRS location that processed the partnership's return.

Item D – Publicly Traded Partnership (PTP)

Check this box if the partnership is a publicly traded partnership (PTP). Leave it unchecked if the partnership is privately held.

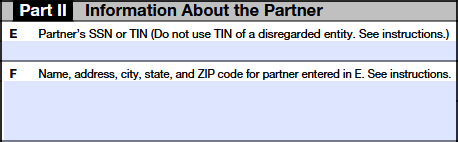

Part II—Information About the Partner (Item E & F)

Item E – Partner's SSN or TIN

- If the partner is an individual, enter their SSN or ITIN; for all other partners, enter their EIN. For a disregarded entity, report the beneficial owner’s TIN in Item E and address in Item F.

- If the partner is an IRA, enter the custodian’s identifying number . Only the last four digits may appear on the partner copy, but the partnership reports the full TIN to the IRS.

Item F – Partner's Name and Address

Enter the partner's full legal name and mailing address, including the city, state, and ZIP code. The information should match the taxpayer identification number entered on Item E.

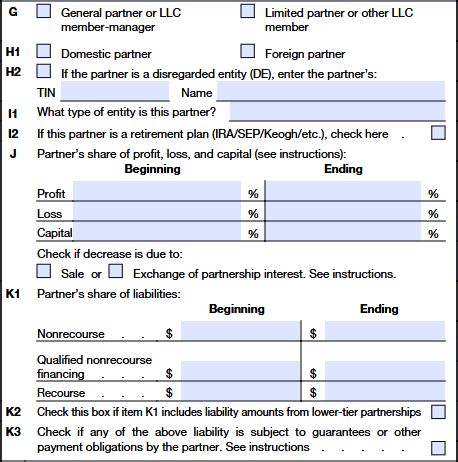

Part II—Information About the Partner (Item G – K3)

Item G – Partner Type

Select whether the partner is a General Partner or LLC Member-Manager or a Limited Partner or Other LLC Member. Choose the option that reflects the partner's role in the partnership.

Item H1 – Domestic or Foreign Partner

Check whether the partner is a domestic or foreign partner. Select only one option based on the partner's tax status.

Item H2 – Disregarded Entity Information

- Check the box only if the partner listed on Schedule K-1 is a disregarded entity, such as a single-member LLC that is not separately taxed.

- Enter the TIN and name of the owner of that disregarded entity, not the LLC’s own details.

Item I1 – Type of Entity

Enter the partner entity type, such as Individual, Corporation, Partnership, Trust, Estate, or LLC. Use the entity classification applicable for tax purposes.

Item I2 – Retirement Plan

Check this box if the partner is a qualified retirement plan, such as an IRA, SEP IRA, or Keogh plan. Otherwise, leave it blank.

Item J – Partner's Share of Profit, Loss, and Capital

- Enter the partner’s percentage share of profit, loss, and capital at both the beginning and end of the tax year. If ownership changes during the year, update the percentages to reflect the partner’s interest at year-end. If the capital account is zero or negative, enter 0 on the capital line.

- If the partner sold or exchanged any part of their partnership interest during the year, check the Sale or Exchangebox to show the reason for the decrease.

Item K1 – Partner's Share of Liabilities

Enter the partner’s share of nonrecourse liabilities, qualified nonrecourse financing, and recourse liabilities at the beginning and end of the tax year. If the partner disposed of their interest during the year, report the share immediately before disposition. These amounts are also used to determine the partner’s basis and, in some cases, at-risk amount.

Item K2 – Lower-Tier Partnership Liabilities

Check this box if the liability amounts reported in Item K1 include liabilities allocated from lower-tier partnerships.

Item K3 – Guaranteed Liabilities

Check this box if any liabilities reported in Item K1 are subject to guarantees or other payment obligations by the partner.

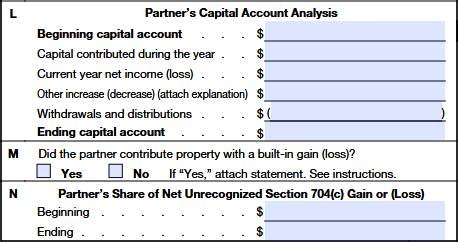

Part II—Information About the Partner (Item L – N)

Item L – Partner's Capital Account Analysis

Report the partner’s beginning and ending capital accounts using the tax-basis method, including contributions, income or loss, distributions, and other adjustments (excluding liabilities). The capital account may differ from the partner’s tax basis, which the partner must track separately for tax reporting purposes.

Item M – Built-In Gain or Loss Property

Check Yes if the partner contributed property with a built-in gain or loss to the partnership. If applicable, attach the required supporting statement. This information is for reporting purposes and may affect your tax liability and certain Schedule K-1 allocations.

Item N – Net Unrecognized Section 704(c) Gain or (Loss)

Report the partner’s net unrecognized section 704(c) gain or loss at the beginning and end of the tax year. This arises from contributed property with built-in gain or loss or partnership book-up/book-down adjustments. The amount is informational and may change due to dispositions or special allocations.

Part III – Partner's Share of Current Year Income, Deductions, Credits, and Other Items

Box 1 – Ordinary Business Income (Loss)

- Enter the partner's share of ordinary business income or loss from the partnership's operations. Do not include separately stated items reported in other fields.

- If you materially participated, report it on Schedule E (Form 1040), Part II. If you did not materially participate, follow passive activity rules (Form 8582) before reporting. If it is a publicly traded partnership (PTP), special rules apply.

Box 2 – Net Rental Real Estate Income (Loss)

- Enter the partner's share of net income or loss from rental real estate activities reported by the partnership.

- If you are a real estate professional who materially participated, it is not passive and is reported on Schedule E (Form 1040), Part II. Otherwise, passive income/loss rules apply (Form 8582), and special limits may allow certain losses if you meet eligibility conditions. If it is a PTP, special reporting rules apply.

Box 3 – Other Net Rental Income (Loss)

- Enter the partner's share of rental income or loss from rental activities other than real estate.

- If Box 3 shows a loss, apply the passive loss rules under Form 8582 before reporting it on Schedule E (Form 1040). If it shows income, report it on Schedule E. If the partnership is a PTP, follow the special PTP reporting rules instead.

Box 4a – Guaranteed Payments for Services

Enter guaranteed payments made to the partner for services provided to the partnership. These payments are generally not passive income and are typically reported on Schedule E (Form 1040), Part II.

Box 4b – Guaranteed Payments for Capital

Enter guaranteed payments made to the partner for the use of capital contributed to the partnership. Report these amounts on Schedule E (Form 1040), Part II.

Box 4c – Total Guaranteed Payments

Enter the total guaranteed payments by combining the amounts reported on Lines 4a and 4b.

Box 5 – Interest Income

Enter the partner's share of taxable interest income earned by the partnership during the tax year.

Example: If the partnership earned $2,000 of taxable interest from a business savings account and the partner’s share is 25%, enter $500 in Box 5.

Box 6a – Ordinary Dividends

Enter the partner's share of ordinary dividend income received by the partnership. Individuals generally report this amount on Form 1040 or 1040-SR, line 3b.

Box 6b – Qualified Dividends

Enter the partner's share of qualified dividends that may be eligible for preferential tax rates. Individuals generally report this amount on Form 1040 or 1040-SR, line 3a.

Box 6c – Dividend Equivalents

Enter any dividend equivalent payments allocated to the partner, if applicable. This information is mainly provided for non-U.S. persons and certain domestic partnerships that may need to treat these amounts as U.S. source dividends.

Box 7 – Royalties

Enter the partner's share of royalty income received by the partnership from intellectual property, natural resources, or similar assets. Report royalties on Schedule E (Form 1040), line 4

Box 8 – Net Short-Term Capital Gain (Loss)

Enter the partner's share of net short-term capital gain or loss from assets held for one year or less. Report the partner’s net short-term capital gain or loss on Schedule D (Form 1040), line 5.

Box 9a – Net Long-Term Capital Gain (Loss)

Enter the partner's share of net long-term capital gain or loss from assets held for more than one year. Report the net long-term capital gain (loss) on Schedule D (Form 1040), line 12.

Box 9b – Collectibles (28%) Gain (Loss)

Enter the partner's share of gain or loss from collectibles subject to the 28% capital gains tax rate Worksheet (Schedule D (Form 1040) Instructions, line 18).

Box 9c – Unrecaptured Section 1250 Gain

Enter the partner's share of unrecaptured Section 1250 gain related to depreciable real property. Report your share of unrecaptured section 1250 gain on the Schedule D (Form 1040) Unrecaptured Section 1250 Gain Worksheet (line 19)

Box 10 – Net Section 1231 Gain (Loss)

- Enter the partner's share of Section 1231 gain or loss from the sale or exchange of qualifying business property.

- If it is a gain or non-passive loss, report it on Form 4797, line 2 (column g). If it is a passive loss, apply Form 8582 limits before reporting. If it is from multiple activities, the partnership will provide a separate statement.

Box 11 – Other Income (Loss)

Report any other separately stated income or loss of items not included on previous lines. Refer to IRS instructions for more details.

Box 12 – Section 179 Deduction

Enter the partner's share of the Section 179 deduction allocated by the partnership for qualifying business property. complete Part I of Form 4562 (Depreciation and Amortization). Your share of qualified enterprise zone or qualified real property will be shown in an attached statement from the partnership.

- If the deduction is from a passive activity, report it using Form 8582 instructions.

- If it is not passive, report it in Schedule E (Form 1040), line 28, column (j).

- If Item D of Schedule K-1 is checked, follow the rules for Publicly Traded Partnerships (PTPs)instead.

Box 13 – Other Deductions

Report the partner's share of separately stated deductions using the applicable IRS codes. Refer to IRS instructions for more details.

Box 14 – Self-Employment Earnings (Loss)

Enter the partner's share of self-employment earnings or loss that may be subject to self-employment tax. Use the applicable IRS codes.

Box 15 – Credits

Report the partner's share of tax credits allocated by the partnership. Use the applicable IRS codes and refer to IRS instructions.

Box 16 – Schedule K-3 Attached

- Check this box if Schedule K-3 is attached to provide additional international tax information to the partner.

- If the box is unchecked, the partnership will provide a separate statement with the Schedule K-1 indicating that Schedule K-3 is issued only upon request.

Box 17 – Alternative Minimum Tax (AMT) Items

Report any items that affect the partner's Alternative Minimum Tax (AMT) calculation. Refer to the IRS instruction for applicable codes and amounts.

Box 18 – Tax-Exempt Income and Nondeductible Expenses

Report the partner's share of tax-exempt income and nondeductible expenses separately. These items may affect the partner's basis and other tax calculations.

Box 19 – Distributions

Enter the total cash and property distributions made to the partner during the tax year. These amounts may reduce the partner's basis in the partnership. The amounts reported using codes for more details see IRS instructions.

Box 20 – Other Information

Report any additional tax information required by the IRS using the applicable codes. Refer for more details see IRS instructions.

Box 21 – Foreign Taxes Paid or Accrued

Enter the partner's share of foreign taxes paid or accrued by the partnership. This information may be used to claim a foreign tax credit or deduction.

Box 22 – More Than One Activity for At-Risk Purposes

Check this box if the partnership has multiple activities that require separate at-risk calculations. For more details, refer to the At-Risk Limitations rules.

Box 23 – More Than One Activity for Passive Activity Purposes

Check this box if the partnership has multiple passive activities. Use the attached statement to determine how each activity should be reported on the partner's tax return. For more details, refer to the Passive Activity Limitations rules.

Schedule K vs. Schedule K-1: What's the Difference?

Partners often confuse these two related schedules. Schedule K is the summary schedule attached to Form 1065 that reports the partnership's total share of income, deductions, and credits across all partners combined. Schedule K-1, on the other hand, is the individual statement that breaks out each specific partner's allocated portion. Think of Schedule K as the whole pie, and each K-1 as an individual slice — they must reconcile to the same totals.

At-Risk Rules and Passive Activity Rules

Two additional limitations apply to partnership losses reported on a K-1 before they can be deducted on a partner's return:

At-Risk Rules (Section 465): Partners can only deduct losses to the extent they are "at risk" — meaning the amount they could actually lose. Amounts at risk generally include cash contributed, the adjusted basis of property contributed, and certain recourse debt. Nonrecourse debt (except qualified nonrecourse financing secured by real property) typically does not increase a partner's at-risk amount. Partners use Form 6198 to calculate and report at-risk limitations.

Passive Activity Loss Rules (Section 469): Losses from passive activities can only offset income from other passive activities. A partner is generally passive in a partnership if they do not materially participate in the partnership's activities. Limited partners are presumed passive. Excess passive losses are suspended and carried forward to future years when passive income is available or the activity is fully disposed of. These limitations are calculated using Form 8582.

These rules interact with each other and with basis limitations, meaning a loss reported on a K-1 may face multiple layers of limitation before it can actually reduce taxable income.

When to Expect Your Schedule K-1

Unlike W-2s and 1099s, which are due to recipients by January 31, Schedule K-1 forms for partnerships are tied to the partnership's tax filing deadline.

Partnerships filing on time must issue K-1s by March 15 (or the next business day if March 15 falls on a weekend or holiday — for the 2025 tax year, the deadline is March 16, 2026).

Partnerships that fail to file on time face a penalty of $255 per partner, per month (up to 12 months). A separate penalty of $330 per K-1 applies for failure to furnish Schedule K-1s to partners on time.

If the partnership files for an extension using Form 7004, the due date extends to September 15, which can significantly delay your ability to file your own personal return.

Because of this timing issue, many partners who are waiting on K-1s file for a personal tax extension using Form 4868 to extend their own filing deadline to October 15. This is a very common and completely acceptable practice.

What to do if your K-1 is late:

- Contact the partnership's managing partner or tax preparer directly.

- If you believe you should receive a K-1 and cannot obtain it, consult a tax professional about your options.

- Do not simply omit partnership income from your return — all pass-through income is reportable regardless of whether you received the K-1.

Common Mistakes to Avoid with Schedule K-1

- Ignoring the footnotes and supplemental schedules. Many K-1s come with attached statements that provide additional detail beyond what fits in the boxes. Missing this detail can lead to errors.

- Failing to apply basis, at-risk, and passive activity limitations. Simply entering the loss from Box 1 without checking whether you have sufficient basis, are at-risk, or qualify as an active participant can result in an incorrect deduction that may trigger an IRS notice.

- Not tracking basis from year to year. Basis tracking is the partner's responsibility, not the partnership's. Failing to maintain an accurate basis schedule makes it impossible to correctly determine the taxability of future distributions or the gain or loss on a future sale.

- Missing state K-1 requirements. Many states require separate state K-1s or adjustments. If the partnership operates in multiple states, partners may need to file nonresident state returns in those states. Do not assume the federal K-1 covers your state tax obligations.

- Confusing distributions with income. A distribution shown on the K-1 is not necessarily taxable income. Whether it's taxable depends on your basis. Conversely, allocated income is taxable even if you never actually received a cash distribution.

- Not reconciling with the prior year K-1. Changes in profit/loss percentages, capital account balances, and liability allocations from year to year should be reviewed and understood before filing.

Schedule K-1 and Real Estate Partnerships

Partnerships that own real estate generate K-1s with some unique characteristics. Rental real estate income or loss is reported in Box 2 of the K-1, and any income or loss from the IRS Form 8825 (Rental Real Estate Income and Expenses of a Partnership) flows through to this line. Real estate partnerships may also generate significant depreciation deductions — including bonus depreciation and cost segregation results — that are allocated to partners via the K-1. The interplay between at-risk rules, passive activity rules, and real estate professional status makes real estate K-1s particularly complex and warrants careful review.

Publicly Traded Partnerships (PTPs) and K-1s

Partners in Publicly Traded Partnerships (PTPs) — also called master limited partnerships (MLPs) — receive Schedule K-1s just like investors in private partnerships. However, PTP K-1s come with unique complexities:

- Passive loss rules apply at the PTP level, meaning losses from one PTP cannot offset income from another PTP or other passive income — they can only offset income from that same PTP.

- Section 751 "hot asset" issues are common with PTP dispositions and can convert what appears to be a capital gain into ordinary income.

- State filing requirements can be extensive, as PTPs often operate in many states.

- K-1s from PTPs may arrive late and sometimes require amended K-1s.

Investors in PTPs through brokerage accounts should consult a tax advisor familiar with MLP taxation, as the complexity is significantly higher than with a standard partnership interest.

Frequently Asked Questions (FAQs)

1. Do I pay taxes on my K-1 income even if I didn't receive any cash distribution?

Yes. Partnership income is taxable in the year it is earned by the partnership, regardless of whether cash is actually distributed to you. This is a fundamental aspect of pass-through taxation.

2. Can a K-1 show a loss that I can deduct?

Potentially, but only after applying the basis limitation, at-risk rules, and passive activity rules. If you pass all three tests, the loss is deductible in the current year. If not, it carries forward.

3. What if I receive a K-1 after I've already filed my return?

You should file an amended return (Form 1040-X) to include the K-1 information. This is also why filing for a personal extension using Form 4868 when you're waiting on K-1s is often a wise move.

4. Is a K-1 the same as a 1099?

No. A 1099 reports payments made directly to you (interest, dividends, freelance income, etc.). A K-1 reports your share of a pass-through entity's income, deductions, and credits — items that were earned at the partnership level but are taxable to you as a partner.

5. Do I need to file in every state where the partnership operates?

Possibly. If a partnership earns income in multiple states, partners may have nonresident filing obligations in those states. The K-1 or supplemental schedules should include state-specific information, but consulting a tax professional with multi-state experience is advisable.

6. How do I find the cost basis of my partnership interest?

You must track your basis yourself using historical K-1s, your initial investment records, and records of any additional contributions or distributions. The capital account shown on the K-1 is not the same as tax basis, though it can be a useful starting point if reported on a tax basis.

7. What is the difference between Schedule K and Schedule K-1?

Schedule K summarizes the total income, deductions, and credits of the entire partnership. Schedule K-1 allocates each individual partner's specific share of those totals. each individual partner's specific share of those totals.

8. Can my partnership e-file Form 1065?

Yes — in fact, the IRS generally requires e-filing for partnerships that file 10 or more returns of any type during the year (including W-2s and 1099s). Partnerships with more than 100 partners are also required to file electronically. TaxZerone makes it easy to e-file Form 1065 online, including automatic generation of Schedule K-1s for all partners.

Key IRS Resources for Schedule K-1 (Form 1065)

The IRS publishes official guidance that every partner and tax professional should be familiar with:

| Resource | Description | Link |

|---|---|---|

| Schedule K-1 (Form 1065) | Official IRS form | Download PDF |

| Instructions for Schedule K-1 (Form 1065) | Line-by-line IRS guidance | Download PDF |

| Form 1065 | U.S. Return of Partnership Income | Download PDF |

| Instructions for Form 1065 | IRS instructions for the partnership return | Download PDF |

| Publication 541 | IRS guide to partnership taxation | View on IRS.gov |

| Form 8995 / 8995-A | Qualified Business Income Deduction | About Form 8995 |

| Form 6198 | At-Risk Limitations | About Form 6198 |

| Form 8582 | Passive Activity Loss Limitations | About Form 8582 |

TaxZerone Internal Resources for Partnerships

If you're navigating partnership tax compliance, the following TaxZerone resources provide additional guidance:

| Resource | Description |

|---|---|

| E-File Form 1065 Online | Securely e-file your partnership return and generate K-1s |

| Form 1065 Instructions | Step-by-step walkthrough of the partnership return |

| Form 1065 Filing Deadlines & Penalties | Key due dates and penalty guidance |

| Form 4797 | Reporting sales of business property |

| Form 4562 | Depreciation and Section 179 deduction |

| Form 8825 | Rental real estate income and expenses |

| Form 1125-A | Cost of goods sold |

| Form 1125-E | Compensation of officers |

| Form 1120-S vs. Form 1065 | S corp vs. partnership comparison |

| Form 7004 – Business Tax Extension | Request a 6-month extension for Form 1065 |

| Form 4868 – Personal Tax Extension | Extend your personal return while waiting for K-1s |