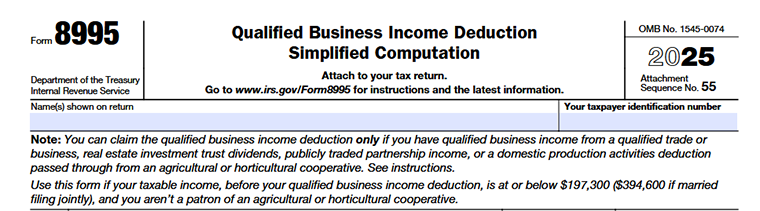

Form 8995, Qualified Business Income Deduction Simplified Computation

Introduction

Form 8995 is a tax form used to calculate the qualified business income (QBI) deduction for pass-through entities, such as sole proprietorships, partnerships, S corporations, and trusts. Tax-exempt organizations that file Form 990-T use the 8995 attachment to calculate and claim the QBID for unrelated business taxable income (UBTI).

In this resource guide, we will learn about the key aspects of Form 8995, from its purpose to filing requirements and commonly asked questions.

Table of Contents

What is Form 8995?

Form 8995, Qualified Business Income Deduction Simplified Computation, is used by eligible individuals, trusts, and estates to calculate and claim the Qualified Business Income Deduction. The QBID allows certain taxpayers to deduct up to 20% of their qualified business income (QBI) from partnerships, S corporations, sole proprietorships, and some trusts and estates.

The deduction is limited to those whose taxable income falls below the specified threshold and is subject to further limitations based on the nature of the business and wages paid.

Who must file Form 8995?

Taxpayers who meet the following criteria must file Form 8995:

- Individuals, trusts, and estates: Those with taxable income below the threshold (currently $197,300 for single filers and $394,600 for joint filers in 2025) and with income from qualified businesses or pass-through entities.

- Owners of partnerships, S corporations, or sole proprietorships: Those who receive qualified business income (QBI) from these entities.

- Tax-exempt organizations filing Form 990-T: Organizations with unrelated business taxable income (UBTI) may use Form 8995 to claim a QBID for their unrelated business activities.

If your taxable income exceeds the threshold, you may need to file Form 8995-A, the expanded version of this form, to calculate the QBID.

Streamline Your 990-T Filing with TaxZerone!

Make your e-filing process simple by clicking the button below.

How to File Form 8995?

In this Form 8995, Enter your name exactly as shown on your tax return. If you are filing jointly, include both spouses’ names.

Next, provide your Taxpayer Identification Number (TIN), like:

- Social Security Number (SSN) OR

- Employer Identification Number (EIN).

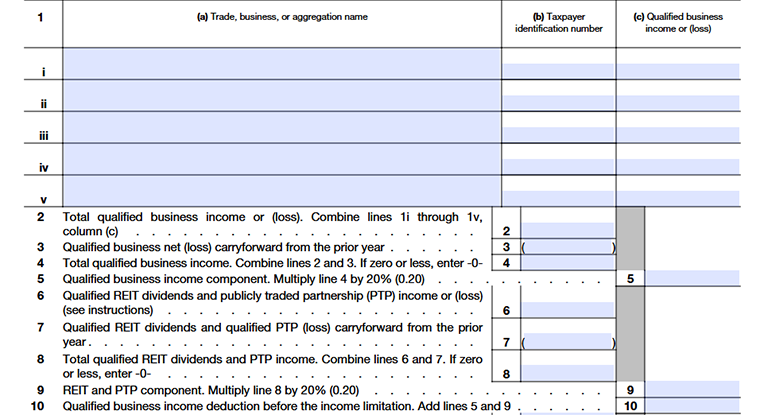

Line 1

- On Line 1(a), enter the name of your qualified trade or business. If you combine multiple businesses into one aggregation, enter the aggregation name instead, such as “Aggregation 1” or “Aggregation 2,” and leave Line 1(b) blank if applicable.

- If you are using the rental real estate safe harbor under Rev. Proc. 2019-38, enter the enterprise name exactly as listed on your safe harbor statement, such as “Enterprise 1.”

- On Line 1(b), enter the business EIN. If you do not have an EIN, use your SSN or ITIN instead. Single-member LLC owners should enter the LLC’s EIN, if available.

- On Line 1(c), enter the net qualified business income (QBI) or loss for that business. Do not include suspended losses or deductions that are not allowed in the current tax year.

Line 2

If you have more than five qualified trades or businesses, attach a separate statement listing:

- the business name,

- taxpayer identification number, and

- related income or loss.

Include the totals from those additional businesses on Line 2.

Line 3

- Enter any qualified business loss carry-forward from prior years that is allowed in the current tax year. This applies even if the business no longer exists.

- Do not include losses or deductions that are still suspended under other IRS rules, as those must be tracked separately until they become allowable.

Line 4

- If your total qualified business income results in a net loss for the year, you generally cannot claim the QBI deduction unless you also have qualified REIT dividends or qualified PTP income.

- The loss will carry forward to the next tax year and may reduce future QBI deductions.

Line 5

For Line 5, multiply the amount on Line 4 by 20% (0.20). This calculates your qualified business income component for the QBI deduction.

Line 6

Enter all qualified REIT dividends and qualified publicly traded partnership (PTP) income or loss on this line.

- Report income as a positive number.

- Report losses as a negative number.

Line 7

- Enter any qualified PTP loss carry-forward from prior years that is allowed in the current tax year. This applies even if you no longer own the PTP or if the partnership no longer exists.

- Do not include losses or deductions that are still suspended under other IRS rules. Those amounts must be tracked separately until they become deductible.

Line 8

- If the total on Line 8 is negative, the loss will carry forward to the next tax year.

- This carry-forward only affects your future QBI deduction calculation and does not change how the loss is treated under other tax rules.

Line 9

Multiply the figure on Line 8 by 20% (0.20) to determine your REIT and PTP component.

Line 10

Combine the figures on Lines 5 and Line 9 to determine your qualified business income deduction before the income limit.

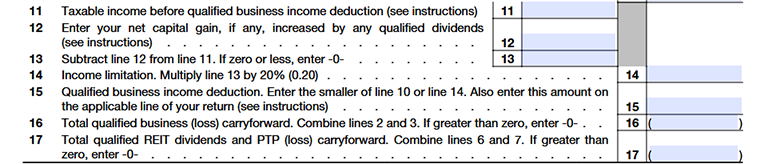

Line 11

Enter your taxable income figured before the QBI deduction. The figure should come from your tax form and be reduced by your applicable deductions according to the instructions of the Internal Revenue Service. For instance, Forms 1040, 1041, and 990-T.

Line 12

- Enter your qualified dividends and net capital gain. The amount you use depends on the form you file, such as: Form 1040 or 1040-SR, Form 1041, Form 1041-N, or Form 990-T.

- If your net capital gain is zero or less, include only the qualified dividends amount.

Line 15

Enter the final qualified business income (QBI) deduction amount on the applicable line of your tax return, such as:

- Form 990-T – Line 9

- Form 1040, 1040-SR, or 1040-NR – Line 13a

- Form 1041 – Line 20

- Form 1041-N – Line 9

- ESBT S-corporation portion – Line 11

Line 16

- If you have a qualified business loss, this amount must be carried forward to the next tax year.

- The carryforward will reduce future QBI deductions, even if the business that generated the loss no longer exists.

Line 17

- Any unused qualified REIT or PTP loss must also be carried forward to the next year.

- This amount will offset future qualified REIT dividends or PTP income, even if the partnership no longer exists.

Embark on a Smooth Form 8995 Filing Journey with TaxZerone

Complete your 8995 filing requirements with ease!

E-file NowCommonly Asked Questions

1. What is the QBI deduction and who is eligible for it?

The QBI deduction is a tax deduction that allows pass-through entities to deduct a portion of their qualified business income. This deduction can reduce the taxable income of these entities.

Sole proprietorships, partnerships, S corporations, and trusts are generally eligible for the QBI deduction.

2. What is the income threshold for using Form 8995?

In 2025, the income threshold for using the simplified Form 8995 is $197,300 for single filers and $394,600 for joint filers.

If your income exceeds these amounts, you may need to use Form 8995-A, Qualified Business Income Deduction to calculate the deduction.