File California Form 565 Online

California partnerships have a state-level filing obligation that's entirely separate from the IRS. TaxZerone makes it simple to complete and submit Form 565 to the FTB — accurately, on time, and without the guesswork.

- FTB-Compliant Filing

- Built-in Accuracy Checks

- Automatic Schedule K-1 (565) Generation

- Trusted by Partnership Owners & CPAs Across California

File California Form 565 for Just $69.99

One flat fee. No hidden charges. Your complete Form 565 e-filing includes Schedule K-1 (565) preparation for all partners and direct submission to the California Franchise Tax Board.

What Is California Form 565?

California Form 565—officially Partnership Return of Income—is the annual state tax return filed by partnerships with the California Franchise Tax Board (FTB). It reports the partnership’s California-source income, deductions, credits, and other required tax information for the year.

Partnerships doing business in California or receiving California-source income generally must file Form 565 annually, even if they operated at a loss or had limited activity. The return also serves as the basis for issuing Schedule K-1 (565) to each partner to report their share of California partnership income.

California vs. Federal — What's Different?

Many partnership owners assume their federal 1065 filing covers everything. It doesn't. Here's what makes Form 565 unique:

| Federal Form 1065 | California Form 565 | |

|---|---|---|

| Filed with | IRS | California FTB |

| Annual tax | None | $800/year (LPs, LLPs, REMICs) |

| Due date (calendar year) | March 16, 2026 | March 16, 2026 |

| QBI deduction (§199A) | Allowed | Not applicable in California |

| Opportunity zone deferral | Allowed | California does not conform |

| Apportionment | N/A | Schedule R required for multi-state income |

| Partner K-1 form | Schedule K-1 (1065) | Schedule K-1 (565) |

California does not always conform to federal tax law. Deductions allowed on your Form 1065 may not be recognized on Form 565 — which is why a dedicated California filing matters.

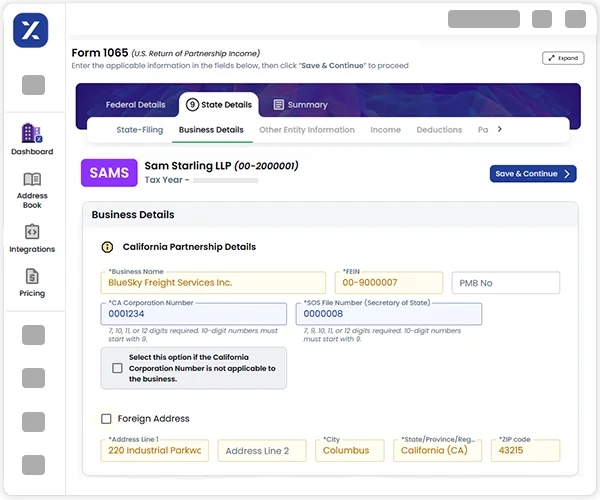

What You'll Need to File

Form 565

Gather these details before you start:

- Partnership Details: Name, FEIN, California Secretary of State file number, and type of partnership (GP, LP, LLP, or REMIC)

- Income & Deductions: California-sourced revenue, cost of goods sold, operating expenses, and applicable deductions

- Partner Information: Name, TIN, ownership percentage, and distributions for each partner

- K-1 Allocations: Each partner's pro-rata share of California income, losses, deductions, and credits

- Balance Sheet Data: Assets, liabilities, and capital accounts at the beginning and end of the tax year

- Apportionment Details: If the partnership operates in multiple states, Schedule R data will be needed

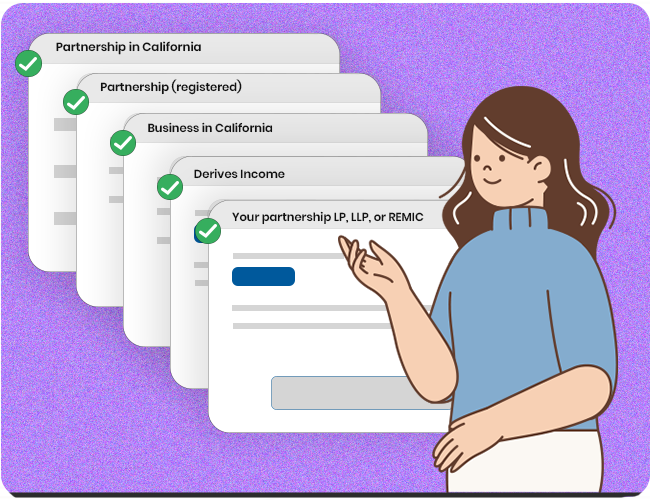

Eligibility Checklist — Does Your Partnership Need to File Form 565?

Your partnership must file Form 565 if any of the following apply:

- Your partnership is organized in California

- Your partnership is registered with the California Secretary of State

- Your partnership is actively doing business in California

- Your partnership derives income from California sources

- Your partnership is a Limited Partnership (LP), Limited Liability Partnership (LLP), or REMIC classified as a partnership

💡 "Doing business" in California includes partnerships whose California sales exceed $757,070 (or 25% of total sales), whose California property exceeds $75,707 (or 25% of total property), or whose California payroll exceeds $75,707 (or 25% of total payroll) — even without a physical office in the state.

Even if your partnership was inactive during the year, LPs, LLPs, and REMICs registered in California are still required to file and pay the $800 annual tax.

The $800 Annual Tax — Don't Miss It

Unlike the IRS, California imposes an $800 annual tax on all LPs, LLPs, and REMICs subject to the franchise tax. This applies even if your partnership:

- Had zero revenue

- Operated at a net loss

- Was inactive for the entire year

- Filed a short-period return of less than 12 months

This $800 must be paid by the original due date — March 16, 2026 for calendar-year filers — even if you've filed an extension. Missing this payment triggers late payment penalties and interest on top of the amount owed.

Cancellation Exception: If your LP or LLP timely files a final return, stops doing business in California after the final taxable year, and files dissolution documents with the California SOS within 12 months of that final return, the $800 annual tax will not be assessed for subsequent years.

Example: An LP files a timely 2025 final return on March 16, 2026, pays the $800 for 2025, does no business after 2025, and files its cancellation paperwork with the SOS before March 15, 2027. The LP owes no $800 tax for 2026.

Form 565 Filing Deadlines — 2025 Tax Year

These deadlines apply to partnerships using a calendar year(January 1 – December 31, 2025):

| Filing Type | Deadline |

|---|---|

| Original return | March 16, 2026 |

| Partner K-1 (565) distribution | March 16, 2026 |

| With automatic extension | October 15, 2026 (7-month extension) |

For Fiscal-Year Partnerships:

The original due date is the 15th day of the 3rd month after your fiscal year closes. The extended deadline is 7 months after the original due date.

Examples:

Fiscal year ends June 30, 2025 → Original due date: September 15, 2025 → Extended due date: April 15, 2026.

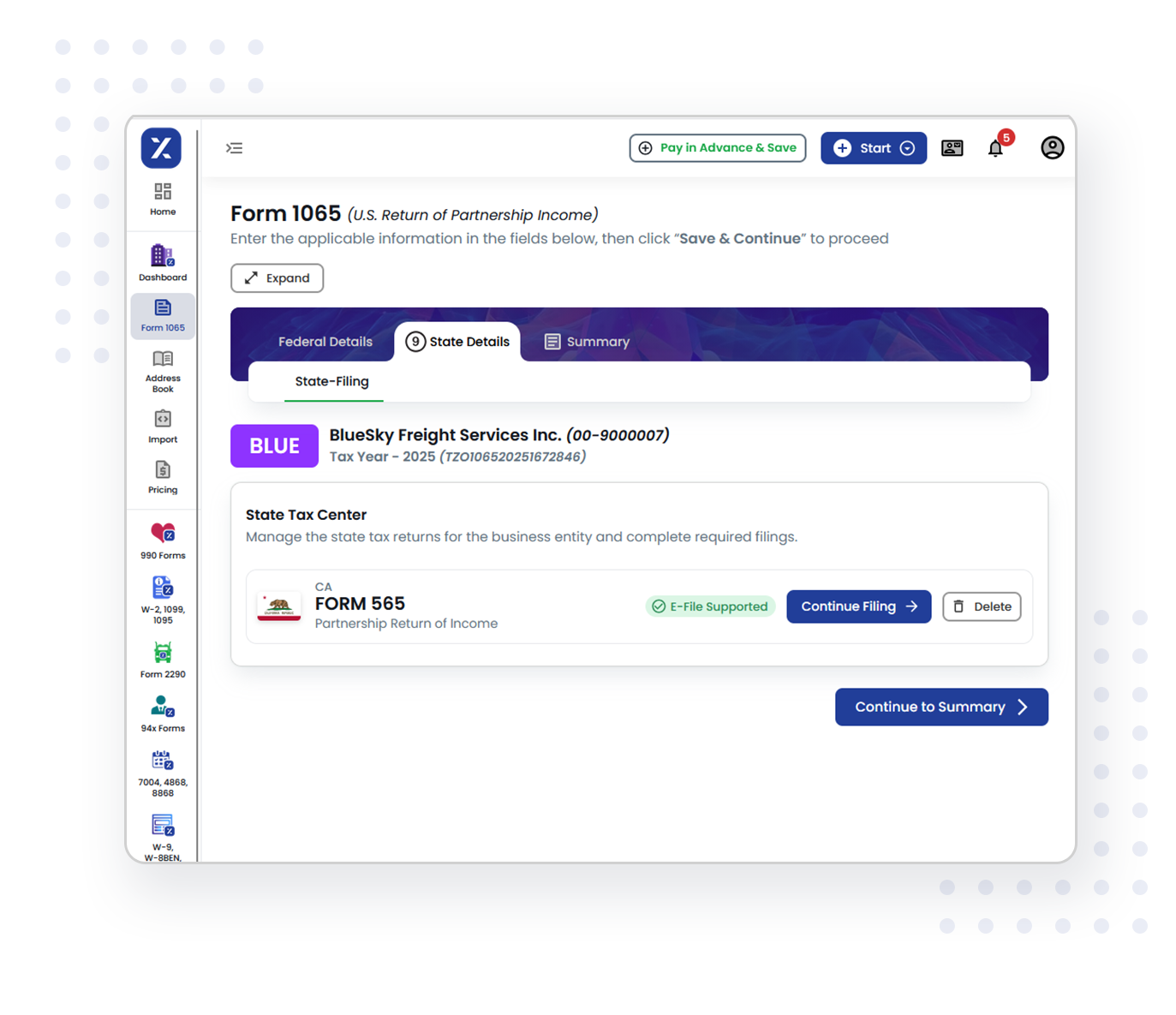

How to File Form 565 with TaxZerone

Step 1 — Create Your TaxZerone Account

Sign up and select California Form 565 from the business tax forms section.

Step 2 — Enter Partnership & Partner Details

Input your California Secretary of State file number, FEIN, tax year, partnership type, and partner information through our guided interface.

Step 3 — Report Income, Deductions & Credits

Enter your California-sourced income, allowable deductions, and applicable credits. TaxZerone automatically generates Schedule K-1 (565) for each partner.

Step 4 — Validate Before You File

Our built-in error checks scan for missing TINs, calculation mismatches, and common FTB rejection triggers — giving you a clean return before submission.

Step 5 — Submit to the FTB & Distribute K-1s

File directly with the California FTB through TaxZerone. After filing, securely distribute Schedule K-1 (Form 565) copies to partners digitally through ZeroneVault (secure portal) or by mail.

Why Choose TaxZerone for Form 565?

FTB-Compliant Filing

File directly with the California Franchise Tax Board on a platform built for state-level accuracy and compliance.

Guided Step-by-Step Workflow

Whether you're filing Form 565 for the first time or the tenth, our system walks you through every section — no tax expertise required.

Auto-Generated Schedule K-1 (565)

Partner K-1s are created automatically from your return data and ready for immediate digital or postal delivery.

Automatic Federal Data Import

If you filed your federal Form 1065 with TaxZerone, your information is automatically imported into your California Form 565, reducing manual data entry and helping you file faster.

Advanced Error Checks

We scan for missing information, calculation errors, and California-specific compliance issues before your return reaches the FTB.

Dedicated Support Team

Have a California-specific question? Our support team is available via chat, email, and phone to help you file with confidence.

Special Pricing for CPAs & Tax Professionals

Filing Form 565 for multiple California partnerships? TaxZerone offers exclusive bulk pricing, reusable client profiles, and dedicated support for tax professionals managing high-volume filings.

- Bigger filings = Bigger discounts

- Save time with reusable business profiles across clients

- White-glove support during peak filing season

📞 Contact Us Now to unlock your custom CPA pricing and make this California filing season your smoothest yet.