Form 990 Schedule F

Introduction

Schedule F, "Statement of Activities Outside the United States," is an integral part of the annual information return filed by tax-exempt organizations in the United States. Schedule F focuses on disclosing the activities and financial transactions of tax-exempt organizations conducted outside the United States at any time during the tax year.

In this resource guide, we will explain the purpose of Schedule F and address common queries to provide clarity and guidance for 990 filers.

Table of Contents

What is Schedule F?

Schedule F, is used by an organization that files Form 990 to provide information on its activities conducted outside the United States by the organization at any time during the tax year. It requires detailed reporting on foreign investments, grants, activities, and other transactions.

The schedule aims to provide transparency regarding international operations, ensuring that tax-exempt organizations comply with IRS regulations and accurately report their global activities.

Who must file Schedule F?

Tax-exempt organizations that engage in activities or financial transactions outside the United States are generally required to file Form 990 Schedule F.

Organizations that answered “Yes” on Form 990, Part IV,Checklist of Required Schedules, line 14b, 15, or 16, must complete the appropriate parts of Schedule F (Form 990) and attach Schedule F (Form 990) to Form 990.

Embark on a stress-free tax journey with TaxZerone – your gateway to effortless filing!

Your journey to seamless tax compliance begins here!

Schedule F Filing Requirements

All Section 501(c)(3) organizations that file Form 990 must complete and attach Schedule F

Below, we have provided Schedule F filing requirements for each part.

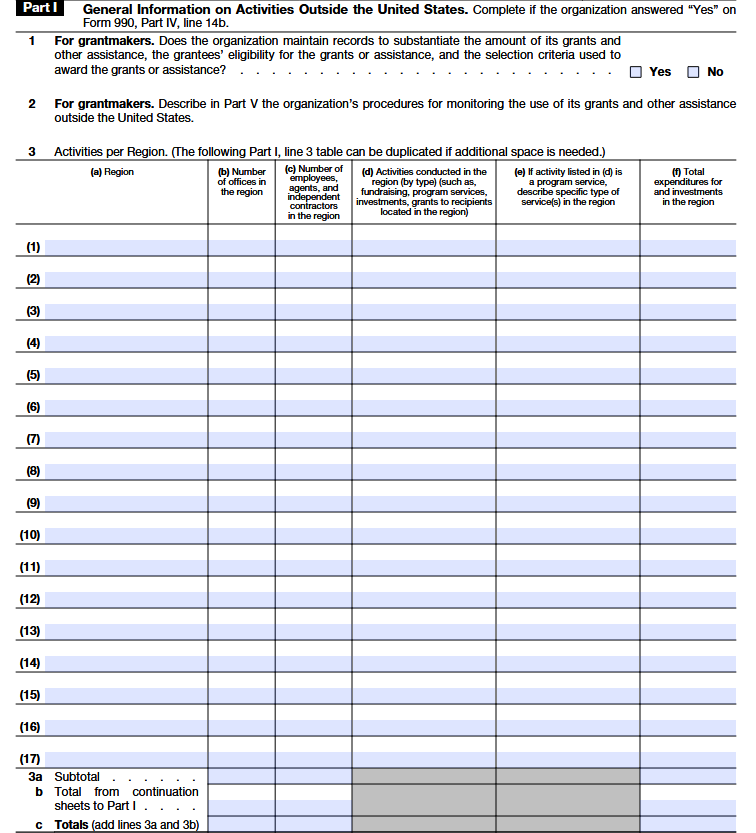

Part I - General Information on Activities Outside the United States.

Line 1

This asks if your organization keeps proper records for grants or assistance given outside the U.S., including who received it, how much was given, and how they were chosen.

Line 2

This asks how you make sure the funds or assistance sent abroad are used correctly, such as reviewing reports or checking how the money is spent.

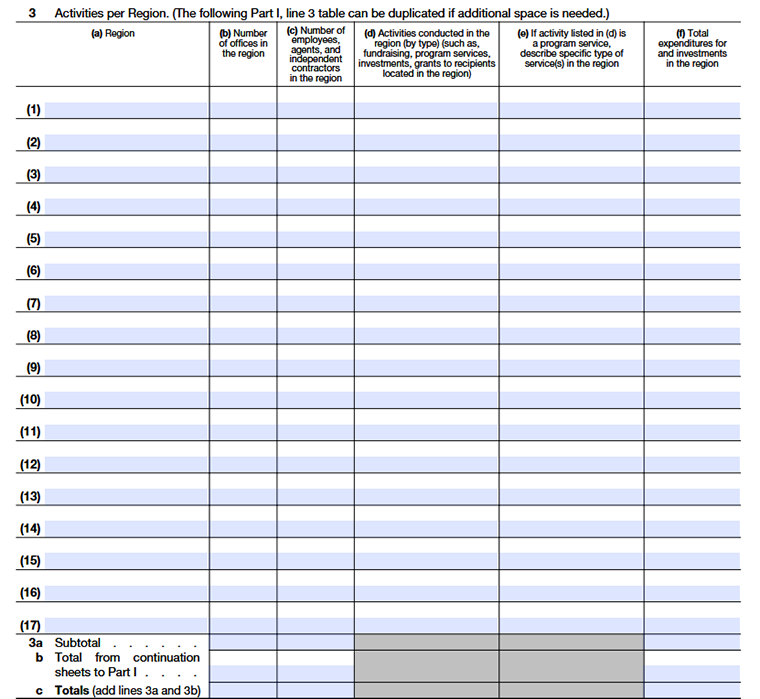

Line 3

This section asks you to report all activities your organization carried out outside the United States during the tax year, grouped by world region (for example: Africa, Europe, Asia, South America, etc.).

Column (a)

Write to the foreign region where the activity happened.

Column (b)

Enter how many offices your organization had in that region (if any).

Column (c)

Enter the number of employees, agents, or contractors working there (don’t include volunteers).

Column (d)

Mention what you did there, such as:Grants,Program services,Fundraising,Business activities, or Investments.

Column (e)

Complete this only if you selected program services. Briefly explain what service was provided.

Column (f)

Report:

- Total money spent for activities in that region, or

- Total value of investments at year-end.

(Amounts can be rounded to the nearest $1,000.)

Line 3a

Add up all the amounts you reported on Part I for each region on the main form (not including continuation sheets).

Line 3b

Add any amounts reported on extra pages if you listed more regions or activities than fit on the main form.

Line 3c

Combine 3a + 3b to get the overall total expenditures and investments for all foreign activities.

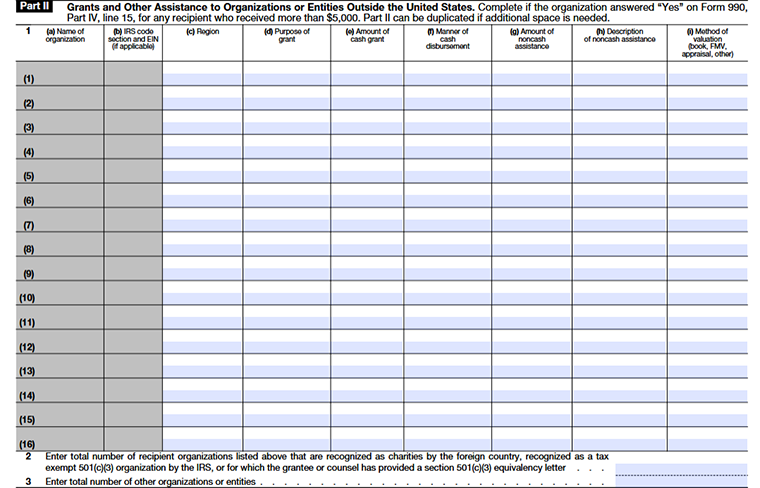

Part II - Grants and Other Assistance to Organizations or Entities Outside the United States.

Line 1

Report each recipient organization that got more than $5,000 from your organization during the year. Include cash and noncash grants, no matter the source of the funds. List each recipient on a separate line.

Column (a)

Write the full name of the recipient organization.

Column (b)

Include the recipient’s tax status (like 501(c)(3)) and their Employer Identification Number.

Column (c)

Indicate the foreign region where the recipient’s main office is, or where the grant funds are used.

Column (d)

Explain exactly what this money is for, like a scholarship, emergency relief, or a specific project.

Column (e)

State the total amount of actual money given to the recipient.

Column (f)

Describe the method used to send the funds, such as a direct check, wire transfer, or a deposit to a school account.

Column (g)

If you give items instead of money (like equipment or supplies), list what those items are worth.

Column (h)

Briefly describe the specific items or services provided as noncash.

Column (i)

Note whether you used the original cost (book), the current market price (FMV), or a professional appraisal to decide what the items were worth.

Line 2

Count how many of the recipients you listed are officially recognized as charities by their country, are a U.S. 501(c)(3) nonprofit, or have a 501(c)(3) equivalency letter from a lawyer or the grantee.

Line 3

Count the rest of the recipients that don’t meet the above criteria.

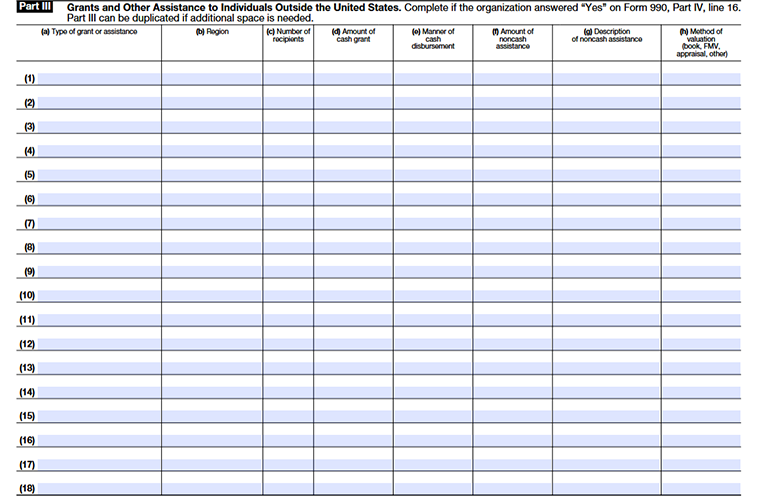

Part III - Grants and Other Assistance to Individuals Outside the United States

Use this section to report any international support over $5,000. This includes direct payments to individuals abroad or money sent to foreign organizations specifically meant to help certain people.

Column (a)

Say exactly what the help was for, like scholarships, food, clothing, medical supplies, shelter, disaster relief, or school materials.

Column (b)

Name the region where the recipients live, e.g., Africa, Asia, and South America.

Column (c)

How many people received this help. If you don’t know the exact number, estimate and explain in Part V.

Column (d)

Total cash given in U.S. dollars. Includes checks, wire transfers, money orders, or other payments.

Column (e)

Explain how the money actually got to the recipient. For example: by check, bank transfer, money order, or other methods. Keep it simple and clear.

Column (f)

Value of items or services provided instead of money.

Column (g)

Describe what was given, like blankets, books, medical equipment, or supplies.

Column (h)

Explain how you decided what the noncash items were worth. For example: you could say based on the current market price, estimated by a professional appraiser, recorded value from our books, or another reasonable way you determined the value.

Enter in this part the information for grants and other assistance made directly to foreign individuals, or directly to foreign organizations for the benefit of specified foreign individuals. Don't complete Part III for grants and other assistance to foreign individuals through a foreign organization unless the grant or assistance is earmarked for the benefit of one or more specific individuals.

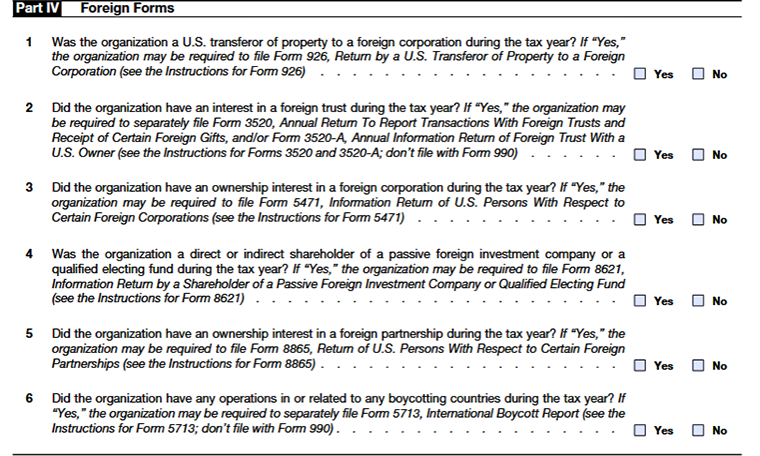

Part IV - Foreign Forms

Line 1

If your organization sends property or assets to a foreign corporation during the year, you may need to report this on Form 926. This ensures the IRS knows about transfers of U.S. property to foreign entities.

Line 2

If your organization had any interest in a foreign trust, you may need to file Form 3520 or 3520-A. These forms report transactions with foreign trusts and gifts received from abroad. These forms are filed separately from Form 990.

Line 3

If your organization owned part of a foreign corporation, you may need to file Form 5471. This reports information about U.S. persons with ownership in certain foreign corporations.

Line 4

If your organization was a shareholder in a passive foreign investment company (PFIC) or a qualified electing fund (QEF), you may need to file Form 8621. This reports on income and distributions from foreign investment funds.

Line 5

If your organization owned part of a foreign partnership, you may need to file Form 8865. This reports the organization’s share of the partnership’s income, expenses, and other activities.

Line 6

If your organization conducted any operations or had dealings with countries under boycott, you may need to file Form 5713. This reports participation in international boycotts and is filed separately from Form 990.

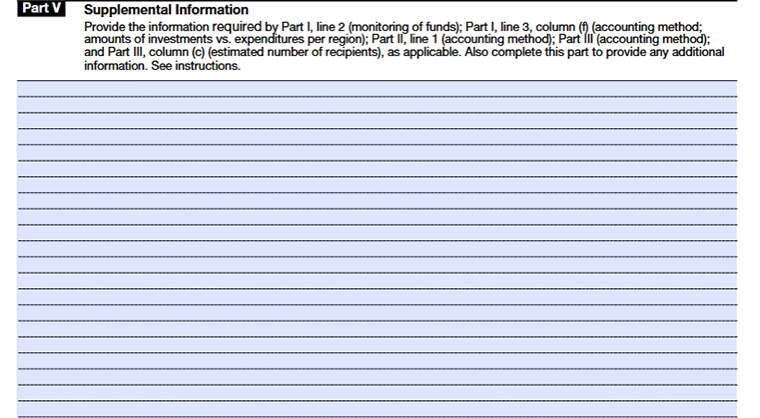

Part V - Supplemental Information

Part V is used to provide additional details and explanations that support other parts of the form. Use it to describe:

- Part I, line 2: How the organization monitors grants and other assistance given outside the U.S. to make sure funds are used properly.

- Part I, line 3, column (f): Explain how the organization keeps track of and records its expenses in its financial records.

- Part II, line 1: How the organization records cash and noncash grants on its financial statements.

- Part III: How the organization records cash and noncash assistance to foreign individuals on its financial statements.

- Part III, column (c): How the organization estimate the number of recipients when exact numbers aren’t available.

You can also use Part V to explain anything else that needs clarification. Always mention which part and line your explanation supports, so it’s easy for the IRS to understand.

Choose TaxZerone to complete your Schedule F filing

We at TaxZerone promise more than just updates – we promise instant insights into your annual information return filing status, putting you in control at every turn.

At TaxZerone, it's not just about filing; it's about a seamless e-filing experience crafted just for you!

Here’s how your Form 990 return with Schedule F attachment is transmitted to the IRS in 3 simple steps!

- Provide Organization Details - Choose the tax year for which you want to file a return, and provide your organization’s details.

- Preview the Return - Complete Schedule F and preview the information provided in the return for accuracy before transmitting.

- Transmit to the IRS - Transmit Schedule F and your 990 return to the IRS and get the acceptance in just a few hours.

Even if the IRS rejects your Form 990 return due to any reason, you can correct and retransmit it to the IRS for free!

Embrace the Future of Tax Filing – Choose TaxZerone Today!

Make your e-filing process simple by clicking the button below.