Form 990 Schedule J

Introduction

Schedule J, Compensation Information is used by tax-exempt organizations filing Form 990 to report compensation information for certain employees, including key employees, officers, and directors.

In this guide, we'll learn more about Schedule J, providing insights into its purpose, filing requirements, and commonly asked questions.

Table of Contents

What is Schedule J?

Schedule J, serves as a supplement to Form 990, providing a detailed breakdown of compensation offered to specific individuals within the organization, and information on certain compensation practices of the organization. The individual includes officers, directors, trustees, key employees, and other highly compensated staff.

Who must file Schedule J?

An organization that answered “Yes” on IRS Form 990, Part IV, Checklist of Required Schedules line 23, must complete and attach Schedule J along with its 990 return.

If an organization isn't required to file Form 990 but chooses to do so, it must file a complete return and provide all of the information requested, including the required schedules.

Ready to attach Schedule J along with your Form 990 return with TaxZerone?

Make the e-filing process simple by clicking the button below.

Schedule J Filing Requirements

All tax-exempt organizations with certain Officers, Directors, Trustees, Key Employees, and Highest Compensated Employees must complete and attach Schedule J

Below, we have provided Schedule J filing requirements for each part.

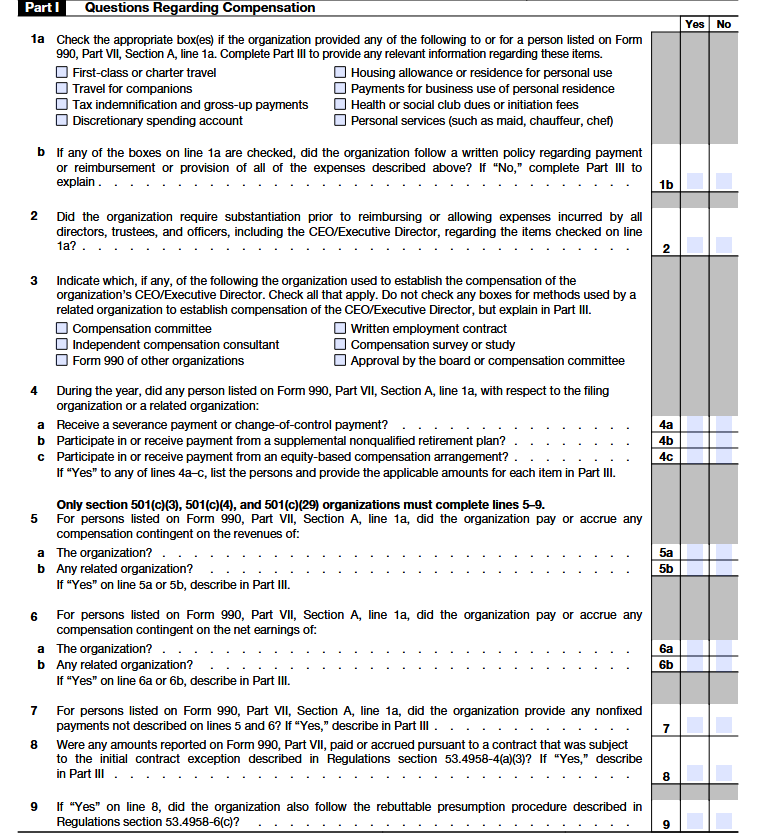

Part I - Questions Regarding Compensation

Line 1a

Check “Yes” for any box if the organization gives extra benefits or personal-type perks to people listed in Form 990, Part VII (officers, directors, key employees, etc.). Even if these benefits were already reported as pay on tax forms, they still must be checked here.

After checking the boxes, explain the details in Part III, including:

- What benefit was given,

- Who received it (or how many people received it), and

- Whether it was treated as taxable income.

Check First-class travel, Charter travel, Travel for companions, Tax payments (gross-ups), Discretionary spending account , Housing or residence, Use of personal home, Club dues, Personal services

Line 1b

- If any of these benefits were provided, answer “Yes” if the organization followed a written policy for approving or reimbursing them.

- If there was no written policy, explain in Part III who approved the benefits and how the decision was made.

Line 2

Answer “Yes” if the organization requires receipts or proper documentation before reimbursing any benefits or expenses listed in line 1a for officers, directors, or the top management official.

Line 3

Check the box(es) showing how the top management official’s pay was decided, such as: Compensation committee review, Outside compensation consultant advice, Comparison with other organizations Form 990s, Written employment contract Salary survey or study, Final approval by the board or compensation committee .

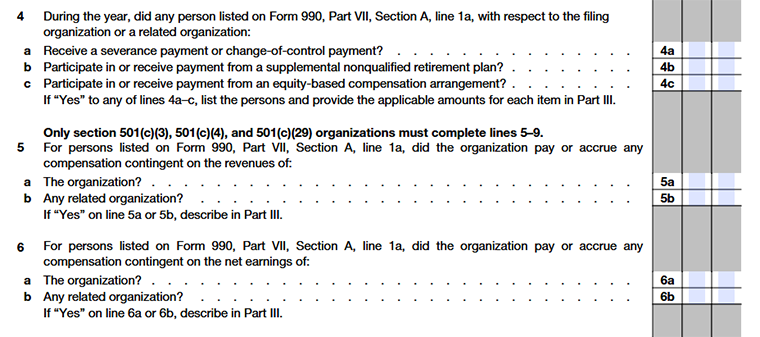

Line 4

In Part III, list the names of listed persons (officers, directors, key employees, etc.) who received payments under the arrangements in lines 4a–4c, the amounts paid, and explain the terms ofthose arrangements. Describe the arrangement even if no payment was made during the year.

Line 4a

Answer “Yes” if someone received payments because they left their job, were terminated, or their employment changed due to a change in organizational control (including settlements for wrongful termination).

Line 4b

Answer “Yes” if a listed person participated in or received payments from a special retirement plan meant only for executives or highly paid employees, not available to all staff.

Line 4c

Answer “Yes” if a listed person received or participated in stock-type or ownership-based compensation (such as stock options or similar arrangements).

Line 5

This line asks whether the organization paid or promised compensation to certain listed individuals that depends on how much revenue is generated.

Line 5a

Indicate whether the organization paid compensation that was based on the organization’s own revenue.

Line 5b

Indicate whether the compensation was based on the revenue of a related organization. If the answer is “Yes” to either line 5a or 5b, provide additional details in Part III.

Line 6

Answer “Yes” if a listed person’s pay or bonus was based on the organization’s net earnings or profits. Describe the details in Part III.

Line 7

Answer “Yes” if a listed person received non-fixed payments, meaning payments where the amount or approval involved discretion (not a set amount or fixed formula in a contract). Example: Expense reimbursements or bonuses decided case-by-case. Explain the arrangement in Part III.

Line 8

Answer “Yes” if payments reported in Form 990, Part VII were made under an initial written contract with someone who was not a disqualified person before the contract started. (Fixed payments under these contracts may qualify for a special exception.) Describe the details in Part III.

Line 9

Answer “Yes” if the initial contract in line 8 was properly reviewed and approved using the organization’s formal approval process (rebuttable presumption procedure).

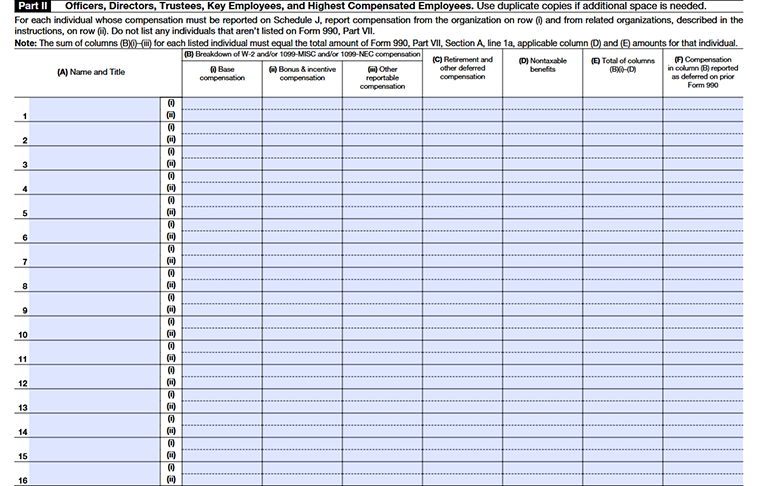

Part II - Officers, Directors, Trustees, Key Employees, and Highest Compensated Employees

Schedule J Part II requires detailed compensation information for individuals for whom the organization answered “Yes” on Form 990, Part IV, line 23.

For each individual whose compensation must be reported on Schedule J, report compensation from the organization on row (i) and from related organizations, described in the instructions, on row (ii). Do not list any individuals that aren’t listed on Form 990, Part VII.

Column(A)

Name and Title

Column(B)

Breakdown of W-2 and/or 1099-MISC and/or 1099-NEC Compensation

- Base Compensation

- Bonus & incentive compensation

- Other reportable compensation

Column(C)

Retirement and other deferred compensation

Column(D)

Nontaxable benefits

Column(E)

Total of columns (B)(i) – (D)

Column(F)

Compensation in column (B) reported as deferred on prior Form 990

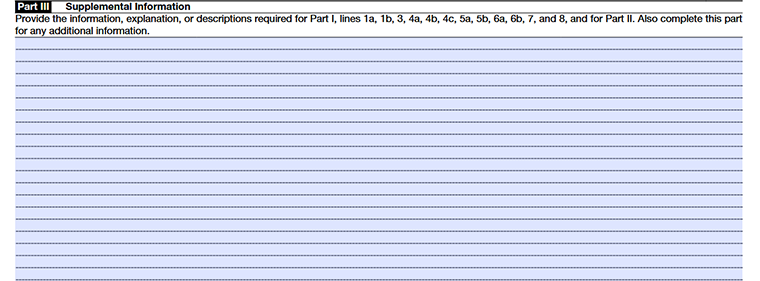

Part III - Supplemental Information

Use Part III to provide narrative information, explanations, or descriptions required for Part I, lines 1a, 1b, 3, 4a, 4b, 4c, 5a, 5b, 6a, 6b, 7, and 8, and for Part II.

Also, list here the name of each unrelated organization that provided compensation to persons listed in Form 990, Part VII, Section A; the type and amount of compensation the unrelated organization paid or accrued; and the person receiving or accruing such compensation.

Choose TaxZerone to complete your Schedule J filing

Navigate the complexities of e-filing Form 990 with TaxZerone, an IRS-authorized e-file service provider. Our intuitive platform and dedicated support team will guide you seamlessly through every step, ensuring a stress-free and efficient filing experience.

Here’s how your Form 990 return with Schedule J attachment is transmitted to the IRS in 3 simple steps!

- Provide Organization Details - Choose the tax year for which you want to file a return, and provide your organization’s details.

- Preview the Return - Complete Schedule J and preview the information provided in the return for accuracy before transmitting.

- Transmit to the IRS - Transmit Schedule J and your 990 return to the IRS and get the acceptance in just a few hours.

With TaxZerone, you stay informed with instant updates on your return’s filing status, eliminating guesswork and anxiety.

Even if the IRS rejects your Form 990 return, our platform allows you to make necessary corrections and resubmit it for FREE!

Simplify Your Tax Compliance Journey with TaxZerone

Make the e-filing process simple by clicking the button below.