Form 990 Schedule R

Introduction

Schedule R, "Related Organizations and Unrelated Partnerships" is a required attachment to

IRS Form 990 for tax-exempt organizations that have relationships with other organizations or certain partnerships. It provides the IRS with details about related organizations, ownership interests, and reportable transactions to promote transparency and ensure compliance.

If you're preparing the 990 IRS tax form and need guidance on Form 990 Schedule R, this resource explains who must file, reporting requirements, related organization classifications, and how to accurately complete the schedule as part of your Form 990 filing.

Table of Contents

What is Schedule R?

Form 990 Schedule R serves as a supplementary document attached to Form 990. It provides the IRS with detailed information on:

- Related Organizations: This includes tax-exempt organizations with shared governance or control, or entities treated as disregarded entities of the filing organization.

- Transactions with Related Organizations: It captures details about financial transactions (sales, loans, etc.) between the filing organization and its related organizations.

- Unrelated Partnerships:For certain partnerships where the organization conducts a significant portion of its activities, Schedule R requires disclosure of the partnership's structure and activities.

Who must file Schedule R?

We have formulated a table that indicates which organizations must complete all or a part of Schedule R and attach Schedule R to Form 990.

| Type of filer | If you answer “Yes” to… | Then you must complete… |

|---|---|---|

| All organizations | Form 990, Part IV, line 33 (regarding disregarded entities) | Schedule R, Part I. |

| All organizations | Form 990, Part IV, line 34 (regarding related organizations) | Schedule R, Parts II, III, IV, and V, line 1, as applicable. |

| All organizations | Form 990, Part IV, line 35b (regarding payments from or transactions with controlled entities) | Schedule R, Part V, line 2. |

| Section 501(c)(3) organization | Form 990, Part IV, line 36 (regarding transfers to exempt noncharitable related organizations) | Schedule R, Part V, line 2. |

| All organizations | Form 990, Part IV, line 37 (regarding the conduct of activity through unrelated partnership) | Schedule R, Part VI. |

Complete your Schedule R filing requirements and e-file your Form 990 with TaxZerone.

It’s as simple as that!

Schedule R Filing Requirements

Below, we have provided Schedule R filing requirements for each part.

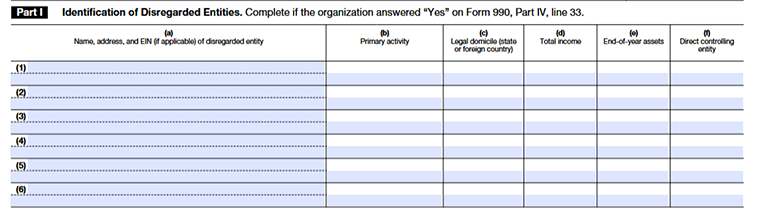

Part I - Identification of Disregarded Entities.

If the organization answered “Yes” on Form 990, Part IV, line 33, it must complete Part I of Schedule R.

Provide the details of each disregarded entity on separate lines of Part I.

- Column (a) - Name, address, and EIN (if applicable) of a disregarded entity

Enter the full legal name and mailing address of the disregarded entity. Also enter the employer identification number (EIN) of the disregarded entity, if it has one. - Column (b) - Primary activity

Briefly describe the primary activity of the disregarded entity. - Column (c)- Legal domicile (state or foreign country)

List the U.S. state (or U.S. territory) or foreign country in which the disregarded entity is organized - Column (d) - Total income

Enter the amount of the filing organization's total revenue reported in Form 990, Part VIII, line 12, column (A), attributable to the disregarded entity. - Column (e) - End-of-year assets

Enter the amount of the organization's total assets reported in Form 990, Part X, line 16, column (B), attributable to the disregarded entity - Column (f) - Direct controlling entity

Enter the name of the entity that directly controls the disregarded entity.

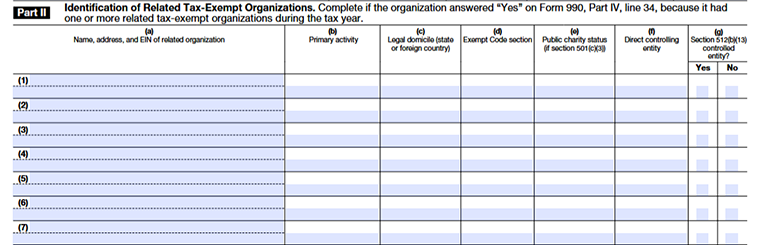

Part II - Identification of Related Tax-Exempt Organizations.

Column (a)

Enter the full legal name and mailing address of the disregarded entity. Also enter the employer identification number (EIN) of the disregarded entity, if it has one.

Column (b)

Briefly describe the primary activity of the disregarded entity.

Column (c)

List the U.S. state (or U.S. territory) or foreign country in which the disregarded entity is organized

Column (d)

Enter the IRS code section that explains the related organization’s tax status, such as 501(c)(3) or 501(c)(6). If it’s a government entity without a 501(c) letter, leave it blank.

Column (e)

- If the organization is a 501(c)(3), list its public charity classification from Schedule A.

- If it’s a private foundation, write “PF.”

- If it’s a supporting organization, include its type (Type I, II, or III).

Column (f)

Enter the name of the organization that directly controls the related organization. If none, write “N/A.”

Column (g)

Indicate whether your organization controls this related entity under section 512(b)(13) by checking Yes or No.

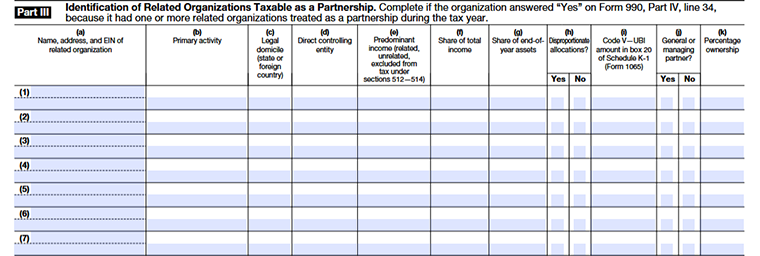

Part III - Identification of Related Organizations Taxable as a Partnership

Column (a)

Enter the full legal name and mailing address of the disregarded entity. Also enter the employer identification number (EIN) of the disregarded entity, if it has one.

Column (b)

Briefly describe the primary activity of the disregarded entity.

Column (c)

List the U.S. state (or U.S. territory) or foreign country in which the disregarded entity is organized

Column (d)

- Enter the name of the organization that directly controls the partnership.

- If no one controls it, write “N/A.”

- If your organization controls it, enter your organization’s name.

Column (e)

- State the main type of income the partnership earns.

- Choose whether most of its income is related, unrelated, or excluded from tax.

Column (f)

Enter the amount of income your organization’s share of the partnership earned during the year, based on Schedule K-1.

Column (g)

Enter your organization’s share of the partnership’s total assets at the end of the year, including its capital account and share of liabilities.

Column (h)

Indicate whether your share of income, losses, or distributions was different from your ownership percentage at any time during the year.

Column (i)

Enter the unrelated business income amount shown as Code V in box 20 of Schedule K-1. If none is reported, write “N/A.”

Column (j)

State whether your organization served as a general partner or managing member of the partnership at any time during the year.

Column (k)

Enter your organization’s ownership percentage in the partnership, using whichever is higher profits interest or capital interest.

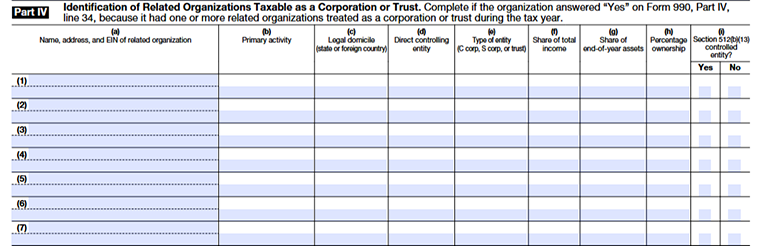

Part IV - Identification of Related Organizations Taxable as a Corporation or Trust

Column (a)

Enter the full legal name and mailing address of the disregarded entity. Also enter the employer identification number (EIN) of the disregarded entity, if it has one.

Column (b)

Briefly describe the primary activity of the disregarded entity.

Column (c)

List the U.S. state (or U.S. territory) or foreign country in which the disregarded entity is organized

Column (d)

Enter the name of the entity that directly controls the disregarded entity.

Column (e)

Specify what kind of entity it is for tax purposes:

- C for a C corporation

- S for an S corporation

- T for trust.

Column (f)

List your organization's portion of the year's income based on your ownership share or the total from Schedule K-1.

Column (g)

State your organization's portion of the final asset values for the year, calculated using your ownership percentage.

Column (h)

State what percentage of the entity your organization owns at year-end. This shows your actual stake in the entity.

Column (i)

Select Yes if your organization has control under section 512(b)(13) or No if it does not.

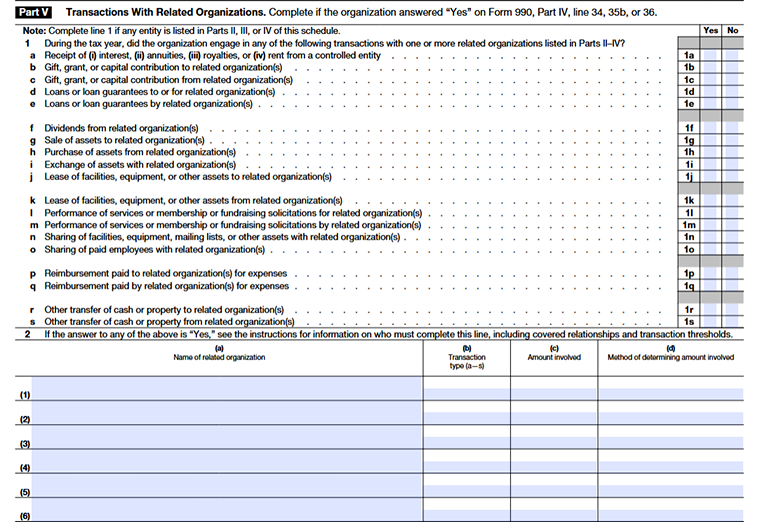

Part V - Transactions With Related Organizations

Line 1

This section is used to report any financial or asset transactions your organization had with related organizations during the tax year (other than fully disregarded entities). A single transaction can appear in more than one line if it fits multiple categories.

Line 1a

Income received from a related organization, like interest, rent, royalties, or annuities.

Line 1b

Gifts, grants, or capital contributions your organization gave to related organizations.

Line 1c

Gifts, grants, or capital contributions your organization received from related organizations.

Line 1d

Loans or loan guarantees your organization made to related organizations.

Line 1e

Loans or loan guarantees your organization received from related organizations.

Line 1f

Dividends received from related organizations.

Line 1g

Sale of assets your organization sold to related organizations.

Line 1h

Purchase of assets your organization bought from related organizations.

Line 1i

Exchange of assets with related organizations.

Line 1j

Leasing out your facilities, equipment, or other assets to related organizations.

Line 1k

Leasing facilities, equipment, or other assets from related organizations.

Line 1l

Services, fundraising, or membership work your organization performed for related organizations.

Line 1m

Services, fundraising, or membership work performed by related organizations for your organization.

Line 1n

Sharing resources like facilities, equipment, or mailing lists with related organizations.

Line 1o

Sharing paid employees with related organizations.

Line 1p

Reimbursing related organizations for expenses they paid on your behalf.

Line 1q

Receiving reimbursement from related organizations for expenses your organization paid.

Line 1r

Any other transfer of money or property your organization gave to related organizations that doesn’t fit above categories.

Line 1s

Any other transfer of money or property your organization received from related organizations that doesn’t fit above categories.

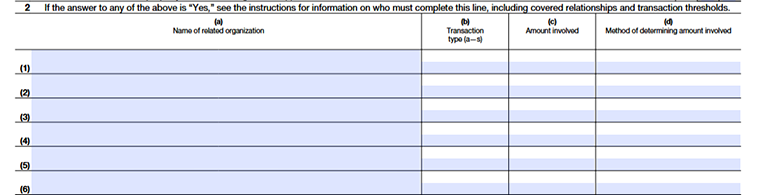

Line 2

This line is for reporting transactions with controlled entities under section 512(b)(13) or with certain related tax-exempt organizations if amounts are significant.

Column (a)

Write the full legal name of the related organization involved in the transaction. If it’s a split-interest trust (like a charitable remainder or lead trust), you can simply use the type of trust instead of the name and include the number of trusts in parentheses if there are multiple.

Column (b)

Enter the code (1a–1s) that matches the type of transaction. Combine all transactions of the same type with the same organization.

Column (c)

Report the fair market value of what was provided or received, whichever is higher. This can include cash, services, or other assets.

Column (d)

Explain in plain terms how you calculated the value of the transaction reported in column (c). This can include the method used to determine the fair market value of cash, services, or other assets exchanged.

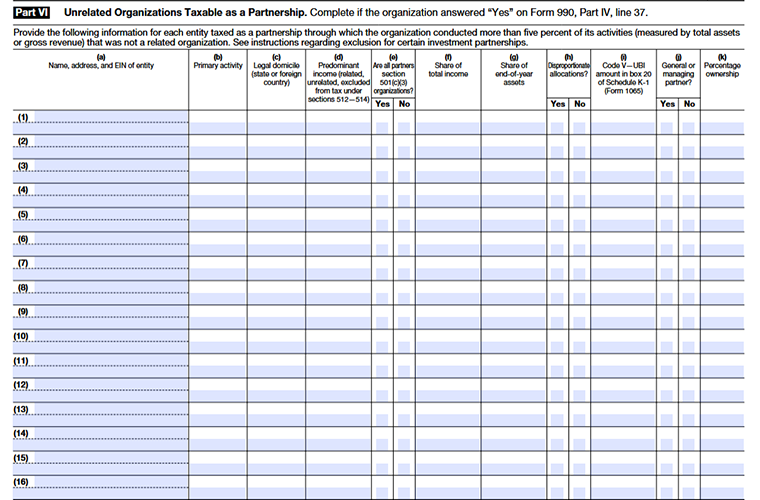

Part VI - Unrelated Organizations Taxable as a Partnership

Part VI is for reporting unrelated partnerships in which your organization is a partner or member, and significant activity is conducted through them.

Column (a)

Enter the full legal name and mailing address of the disregarded entity. Also enter the employer identification number (EIN) of the disregarded entity, if it has one.

Column (b)

Briefly describe the primary activity of the disregarded entity.

Column (c)

List the U.S. state (or U.S. territory) or foreign country in which the disregarded entity is organized.

Column (d)

State the main type of income the partnership earns.

Choose whether most of its income is related, unrelated, or excluded from tax.

Column (e)

Check Yes if all partners are 501(c)(3) organizations or government units; otherwise, check No.

Column (f)

Enter the amount of income your organization’s share of the partnership earned during the year, based on Schedule K-1.

Column (g)

Enter your organization’s share of the partnership’s total assets at the end of the year, including its capital account and share of liabilities.

Column (h)

Indicate whether your share of income, losses, or distributions was different from your ownership percentage at any time during the year.

Column (i)

Enter the unrelated business income amount shown as Code V in box 20 of Schedule K-1. If none is reported, write “N/A.”

Column (j)

State whether your organization served as a general partner or managing member of the partnership at any time during the year.

Column (k)

Enter your organization’s ownership percentage in the partnership, using whichever is higher profits interest or capital interest.

Part VII - Supplemental Information

Use this part if the organization needs space to provide additional information in response to questions in Schedule R (Form 990). In Part VII, identify the specific part and line number that each response supports in the order in which those parts and lines appear on Schedule R (Form 990).

Choose TaxZerone to complete your Schedule R filing

TaxZerone is an IRS-authorized e-file service provider; meaning you get instant updates on your 990 return filing status. We ensure help is available in every step to provide you with a smooth e-filing experience!

Here's how your 990-return filing with Schedule R is securely submitted to the IRS in 3 simple steps!

- Provide Organization Details - Choose the tax year for which you want to file a return, and provide your organization’s details.

- Preview the Return - Complete Schedule R and preview the information provided in the return for accuracy before transmitting.

- Transmit to the IRS - Transmit Schedule R and your 990 return to the IRS and get the acceptance in just a few hours.

Even if the IRS rejects your 990 information return due to any reason, you can correct and retransmit it with TaxZerone for FREE!

Ready to attach Schedule R along with your 990 return with TaxZerone?

Make the e-filing process simple and hassle-free by clicking the button below.

Commonly Asked Questions

1. What qualifies as a related organization in Schedule R?

2. What types of transactions need to be reported on Schedule R?

Additionally, certain non-financial transactions, such as shared facilities or personnel, may also need to be reported.