Introduction

Form 990 Schedule D, also known as the "Supplemental Financial Statements," is an essential component of the annual information return filed by tax-exempt organizations in the United States. This schedule provides detailed information about the organization's assets, liabilities, revenue, and expenses, offering transparency to stakeholders and regulatory bodies.

In this resource guide, we have provided a concise overview of Schedule D, offering valuable insights into its purpose, the entities required to file, and the filing requirements.

Table of Contents

What is Schedule D?

Schedule D, Supplemental Financial Statements is a supplementary schedule that accompanies the standard Form 990 and is filed annually by tax-exempt and nonprofit organizations.

This schedule aims to provide the required reporting for donor-advised funds, conservation easements, certain art and museum collections, escrow or custodial accounts or arrangements, endowment funds, and supplemental financial information.

Who must file Schedule D?

An exempt organization that answered “Yes” to any of lines 6 through 12a on Form 990, Part IV, Checklist of Required Schedules, must complete the appropriate part(s) of Schedule D and attach the schedule to Form 990

Choose TaxZerone to complete your Schedule D filing requirements.

Your journey to staying tax-compliant starts here!

Schedule D Filing Requirements

All Section 501(c)(3) organizations that file Form 990 must complete and attach Schedule D return.

Below, we have provided Schedule D filing requirements for each part.

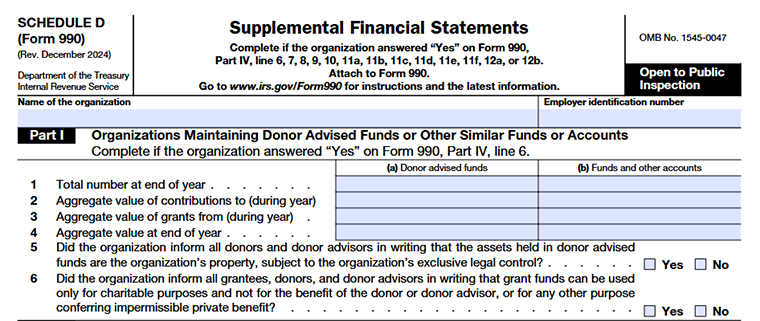

Part I - Organizations Maintaining Donor-Advised Funds or Other Similar Funds or Accounts

If your organization acts as a sponsoring organization that manages Donor Advised Funds (DAFs), you must complete this section to report how those funds were handled during the tax year.

A donor advised fund is generally a charitable fund or account where:

- Contributions are linked to one or more specific donors,

- The fund is legally owned and fully controlled by your organization, and

- The donor or a donor advisor can recommend how the money should be invested or distributed as grants because they made the donation.

Even though donors may provide recommendations, the organization must retain final legal authority and control over all assets and decisions.

Funds That Are Not Considered Donor Advised Funds

Some funds or accounts are not treated as donor advised funds, even if donors are connected to them. These include:

- Funds that distribute money only to one specific charity or government organization.

- Scholarship or grant programs where donors participate only as committee members chosen by the organization and don’t control grant decisions.

- Funds for the Internal Revenue Service (IRS) are specifically exempt because donors don’t control advisory decisions or because the fund supports a single charitable purpose.

When determining donor control, related persons such as family members or entities controlled by the donor are also considered.

Column Reporting Requirements

You’ll report information in two columns:

Column (a)

All donors advised funds held at any time during the tax year.

Column (b)

Other similar funds or accounts where donors had advisory privileges, but which don’t meet the donor’s advised fund definition (including IRS-approved exceptions).

Line 1

Enter the total number of donors advised funds your organization maintained at the end of the tax year. If applicable, also include the number of similar advisory funds or accounts that are not classified as donor advised funds.

Line 2

Report the total amount of contributions added during the year. Include all donations received during the reporting period.

Line 3

Report the total amount distributed from these funds during the year.

This includes:

- Grants paid to outside charitable organizations, and

- Transfers used for charitable activities within your organization.

Line 4

- Enter the total ending balance or fair market value of all donors advised funds and similar advisory accounts as of the end of the tax year.

- Your organization must confirm whether required written notices were provided.

Line 5

Indicate whether donors and donor advisors were informed in writing that:

- Contributions made to donor advised funds become the organization’s property, and

- The organization has full legal control over those assets.

Line 6

Indicate whether donors, donor advisors, and grant recipients were informed in writing that:

- Grant funds must be used only for charitable purposes, and

- Funds cannot provide personal benefit to donors, advisors, or related parties.

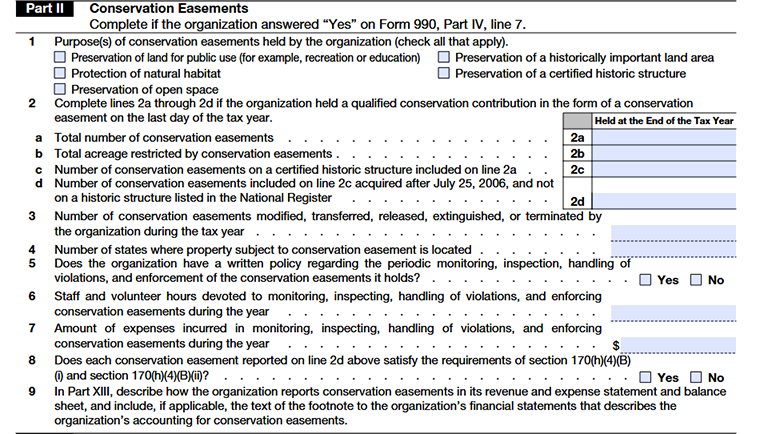

Part II – Conservation Easements

Complete Part II only if your organization answered “Yes” to conservation easement reporting in Form 990, Part IV.

Along with conservation easements, you should also include other real property interests that function in a similar way under state law and are created to support conservation or preservation purposes. Examples may include certain restrictive covenants or equitable servitudes that permanently protect land or property.

Do not include utility easements in this section.

Line 1

- Select the box or boxes that best describe why your organization held conservation easements during the tax year.

- Some easements may serve more than one purpose. For example, a property might protect open space while also preserving natural habitat or historical significance. In those situations, choose every option that applies.

- Your selection should reflect the primary conservation or preservation goal of the easement, such as public access, environmental protection, maintaining open land, or protecting historically important property or structures.

Line 2

- Complete Lines 2a through 2d only if your organization continues to hold one or more qualified conservation easements on the last day of the tax year.

- These questions help report the organization’s conservation easement activity as it stood at year-end. Use information from your official records to make sure the details entered reflect the actual status of the easements at that time.

Line 2a

- Enter the total number of conservation easements your organization held as of the end of the tax year.

- Count each easement separately based on your records. This number should represent the exact total and should not be estimated or rounded.

Line 2b

- Report the total acreage covered by conservation easements as of the end of the tax year.

- Add together all land areas protected under each easement. Do not include acreage connected to certified historic structures when calculating this total.

- If any property involves partial acreage, decimals may be used. For example, two and one-half acres should be entered as 2.5 acres.

Line 2c

- Enter how many of the easements reported on Line 2a apply to certified historic structures.

- A certified historic structure generally includes buildings listed in the National Register of Historic Places, or structures officially recognized as historically significant within a registered historic district.

Line 2d

From the number reported on Line 2c, enter how many conservation easements were acquired after July 25, 2006, and are not connected to a structure listed in the National Register.

Line 3

Enter the total number of conservation easements that were modified, transferred, released, extinguished, or terminated, either fully or partially, during the tax year.

Example: If two easements were modified and one easement was terminated during the tax year, enter 3.

- A modification includes any change to the easement terms. Transfers involve assigning or disposing of the easement, and releases or terminations occur when legal protection ends. Explain each change in Part XIII.

Line 4

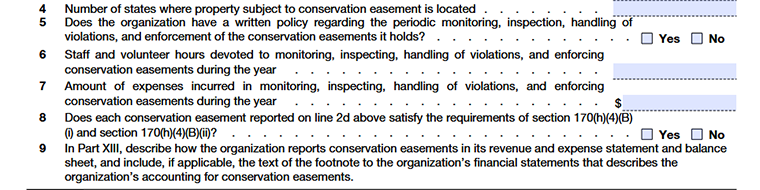

Enter the number of different states where your organization holds conservation easement properties during the tax year.

Line 5

Indicate whether your organization has written policies explaining how it will monitor easement properties, conduct site inspections, and handle violations. If you answer “Yes,” you must briefly summarize these policies in Part XIII, and Confirm whether the same procedures are included in your easement documents.

Line 6

Report the total number of hours your organization spent during the year monitoring properties, visiting sites, and handling any easement violations. Include time worked by employees, volunteers, contractors, or agents.

Line 7

Enter the total costs related to managing and protecting easements, such as staff time, travel for inspections, professional services, or legal expenses.

Line 8

Answer “Yes” if all façade easements accepted after July 25, 2006, protect the entire outside of historic buildings and include a written agreement confirming your organization has the resources and commitment to enforce those restrictions.

Line 9

Explain in Part XIII how conservation easements are recorded in your accounting records and financial statements. Your reporting should be consistent across your books and all required filings with the Internal Revenue Service.

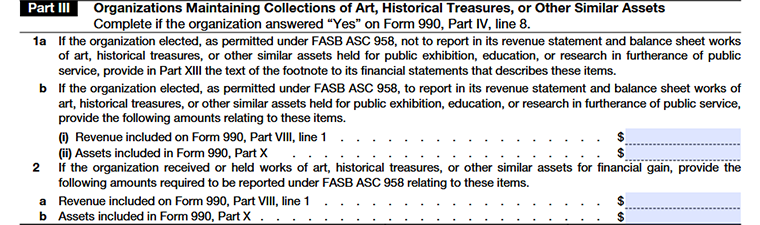

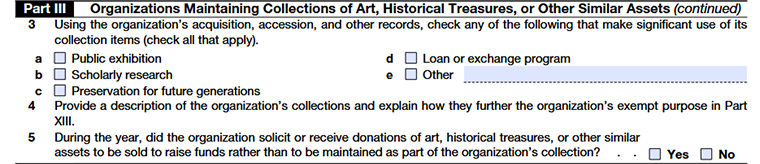

Part III - Organizations Maintaining Collections of Art, Historical Treasures, or Other Similar Assets

Line 1a

If your organization chooses not to record the collection as an asset, include in Part XIII the footnote that explains financial statements that describes these collection items.

Line 1b

If your organization records the collection as an asset:

Line 1b(i)

Report any revenue related to the collection already reported in Part VIII of Form 990.

Line 1b(ii)

Report the total value of the collection included as part of your organization’s assets.

Line 2

This line applies if your organization holds collections mainly to generate income or investment value.

Line 2a

Report the revenue earned from these collections (already included in total revenue on Form 990).

Line 2b

Report the asset value assigned to these collections, which must also be included in total assets on Form 990 Part X.

Line 3

Check all the boxes that show how your organization mainly uses its art, historical items, or similar collections, based on your records.

You can select:

- Public exhibition

- Scholarly research

- Preservation for future generations

- Loan or exchange program

- Other

Line 4

In Part XIII, explain:

- What your collection includes, and

- How it supports your nonprofit mission, such as education, research, or public service.

Line 5

Answer “Yes” if your organization received donated artwork or historical items mainly to sell them and raise money instead of keeping them. Answer “No” if the donated items were kept as part of your permanent collection.

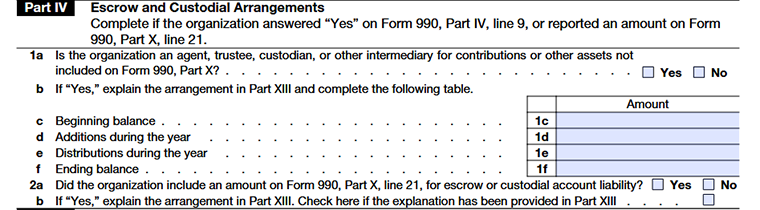

Part IV - Escrow and Custodial Arrangements

Line 1a

- Select “Yes” if your organization collects, manages, or temporarily holds money or contributions for others and does not treat those funds as its own assets or liabilities on Form 990.

For example, this may happen if you collect payments and later send them to creditors, beneficiaries, or partner organizations. - If your organization only handles its own funds, select “No.”

Line 1b

If you answered “Yes,” give a short explanation in Part XIII describing:

- Who the money belongs to, and

- How does your organization receive and distribute it.

Just briefly explain how the process works.

Lines 1c to 1f

If these funds are kept in an escrow or custodial account, you simply need to show how the balance moved throughout the year:

Lines 1c

The amount in the account at the start of the year.

Lines 1d

Any money received or added during the year.

Lines 1e

Money paid out or sent to the correct recipients during the year.

Lines 1f

Enter the amount of money left in the account at the end of the year after all deposits have been added, and payments or transfers have been made.

Lines 2a

- Answer “Yes” if your organization holds money for others and reported that amount as a liability.

- Answer “No” if your organization did not report any such amount.

Lines 2b

If you answered “Yes,” provide an explanation in Part XIII describing:

- Why your organization is holding the money,

- Who the funds belong to, and

- What responsibility, your organization must distribute or manage those funds.

If this explanation is already included in Part XIII, check the box to confirm it.

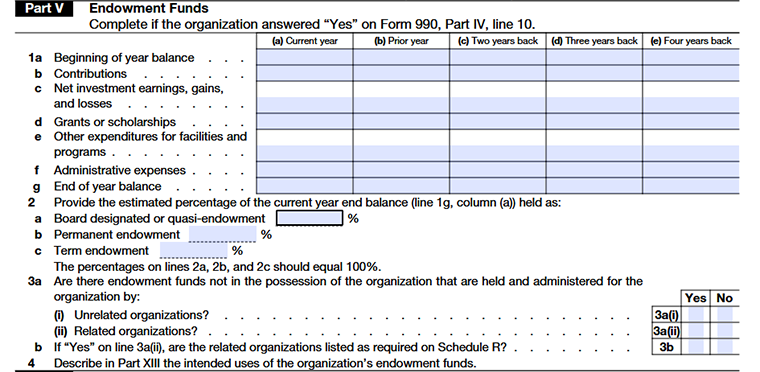

Part V - Endowment Funds

Line 1a

Enter the total value of your organization’s endowment funds at the start of each year. This includes permanent endowments, term endowments, and any board-designated endowment funds.

Line 1b

Report all amounts added to the endowment during the year. This can include donor gifts, grants, transfers, or funds your governing board decided to set aside to function like an endowment.

Line 1c

Enter the total investment results for the year, including income earned from investments as well as any gains or losses in value.

Line 1d

Report amounts paid out from the endowment as scholarships or direct grants to individuals.

Line 1e

Enter the amounts distributed for facilities and programs. Amounts should include withdrawn amounts, and amounts disinvested from an organization's endowments to reduce or eliminate capital investment.

Line 1f

Report any costs related to managing or overseeing the endowment. These may include the expenses spent to manage and maintain the endowment investments

Line 1g

Enter the total value of the endowment funds at the end of the year after accounting. This shows how much money remained in the endowment after everything that happened during the year.

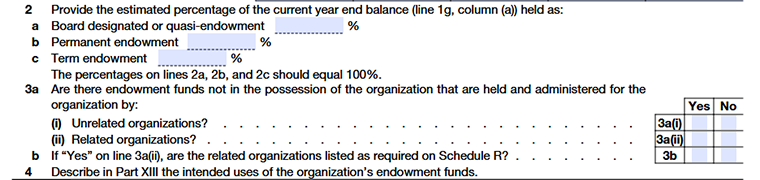

Line 2

This line is to show how your total endowment funds are divided at the end of the current year. Use the ending balance you reported on Line 1g (current year) and estimate what percentage belongs to each type of endowment. The total of all three percentages must be equal to 100%.

Line 2a

- Enter the percentage of funds that were set aside by your organization’s board to function like an endowment.

- These funds are not restricted by donors, and the board can decide to use them whenever needed.

Line 2b

Enter the percentage of funds that donors require to be kept invested forever. Only the income earned from these funds can normally be used.

Line 2c

Enter the percentage of funds that must remain invested until a certain time ends, or a specific condition is met, as required by the donor.

Line 3a(i)

Answer “Yes” if another organization that is not connected or affiliated with your organization holds or manages some of your endowment funds on your behalf.

For example, an independent foundation or financial institution managing funds for you.

Line 3a(ii)

Answer “Yes” if a related or affiliated organization (such as a parent organization, subsidiary, or supporting organization) holds or administers any of your endowment funds.

Line 3b

If you answered “Yes” to Line 3a(ii), you must confirm that all those related organizations are listed on Schedule R (Form 990). This schedule reports relationships between organizations.

Line 4

In Part XIII, explain how your organization plans to use its endowment funds. You should describe the main purposes the funds support.

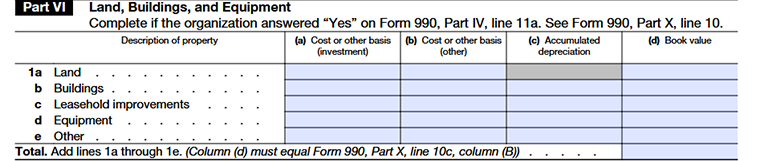

Part VI - Land, Buildings, and Equipment

Line 1

You need to complete Part VI only if your organization answered “Yes” on Part IV, line 11a of Form 990 and reported an amount on Part X, line 10a. This section shows the value of property and equipment your organization owns.

Column (a)

Enter the cost or original value of assets held for investment purposes.

Examples include:

- Rental properties, or

- Property owned mainly to earn income.

Column (b)

Enter the cost or original value of property and equipment used for your organization’s normal activities.

Examples include:

- Office buildings,

- Program facilities,

- Equipment used for charitable or educational work.

The total of Columns (a) and (b) must match the amount reported on Form 990 Part X, line 10a.

Column (c)

Enter the total depreciation recorded for these assets over time. Depreciation reflects normal wear and tear or reduction in value. Do not enter depreciation for land because land is not depreciated.

Column (d)

Calculate the final value of assets by:

- Adding Column (a) and Column (b), and

- Subtracting Column (c).

This gives the current recorded value of your assets. The total must match the amount reported in Part X of Form 990.

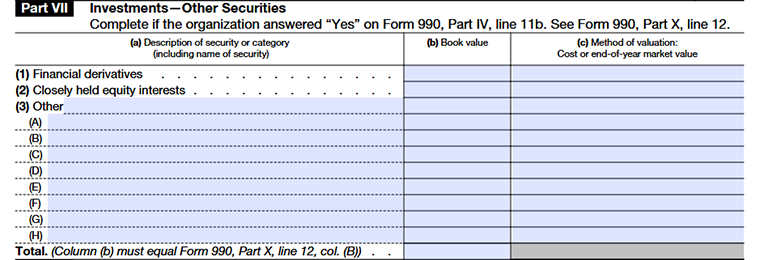

Part VII - Investments—Other Securities

Column (a)

- Use this column to say what the investment actually is. Write a clear description, such as financial derivatives, closely held shares, or any other security.

- If you are reporting publicly traded stock that meets the reporting rules, include the company name, type (class) of stock, and how many shares the organization owns.

Column (b)

Write the year-end value of the investment exactly as it appears in your organization’s financial records. This should match the amount shown in your accounting books and the balance reported on Form 990.

Column (c)

Use this column to state how you arrived at the value entered in Column (b). Simply indicate whether the investment is shown at:

- the original purchase cost, or

- The fair market value at the end of the year.

If you report market value, make sure it is based on standard and commonly accepted valuation practices so the information can be clearly understood and reviewed by the Internal Revenue Service.

Line 1

This line is used to report investments in financial derivatives, such as options, futures, or similar financial contracts held by the organization.

Line 2

Here, the organization reports investments in closely held businesses, meaning ownership interests in companies that are not publicly traded.

Line 3

This line is used to list any other types of securities that don’t fall under derivatives or closely held equity interests.

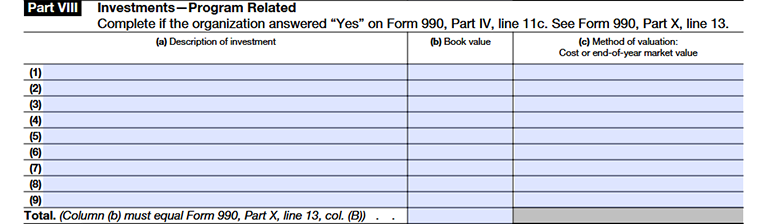

Part VIII - Investments—Program Related

Column (a)

List each investment separately. Give a short and clear explanation of what the investment is. Also mention whether it is a loan or an ownership (equity) investment. If the investment is made in a U.S. organization, include that organization’s name.

Column (b)

Enter the value of each investment based on your organization’s accounting records at the end of the year. The total amount reported here should match the amount shown on Form 990, Part X, to keep your filing consistent with the records reviewed by the Internal Revenue Service.

Column (c)

In this column, just mention how you decided the value entered in Column (b). You can indicate whether the investment is shown at its original cost or at the fair market value at the end of the year.

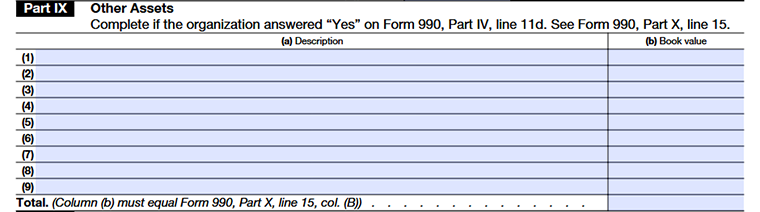

Part IX - Other Assets

Column (a)

Write a clear and simple description of each item included under “Other Assets.” You can group or classify these assets in any reasonable way that makes sense for your records for example, security deposits, prepaid expenses, or other similar items not listed elsewhere on the balance sheet.

Column (b)

Enter the value recorded in your accounting records for each asset listed in Column (a). When you add all the amounts in this column together, the total must match the amount reported on Form 990, Part X, line 15.

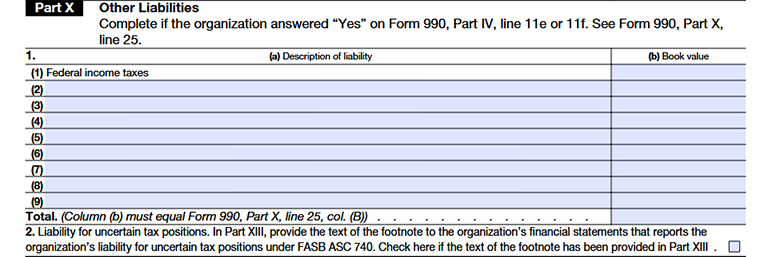

Part X - Other Liabilities

Line 1

Use this line to report any amounts your organization still owes that were not already listed in the earlier liability lines on Form 990, Part X (lines 17–24). Think of this as a place to include remaining obligations that don’t fit anywhere else on the form.

Column (a)

Write a short, clear note about what the organization owes and why. Just use simple wording that matches your records, for example- unpaid bills or money received in advance.

Column (b)

Write the value recorded in your accounting records for each liability listed. When you add them together, the total should be the same as the Other Liabilities amount reported in Form 990, Part X.

Line 2

- If your organization completes Part X, include the tax-related note or footnote from your financial statements that explains any tax situations that may still be uncertain or could change later.

- These rules follow accounting guidance issued by the Financial Accounting Standards Board (FASB) and similar standards.

- Add the full note in Part XIII, even if there is no uncertain tax liability reported. If the note covers several organizations together, you can briefly summarize only your organization’s portion.

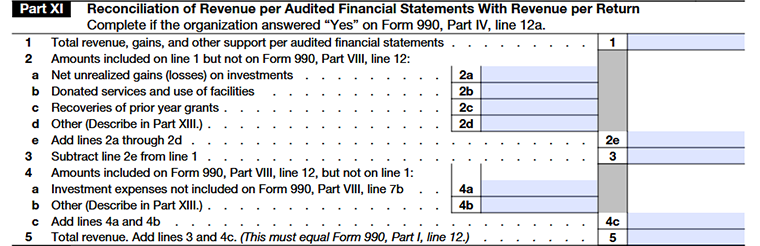

Part XI-Reconciliation of Revenue per Audited Financial Statements with Revenue per Return

Line 1

Total income, gains, and other support shown in the audited financial statements.

Line 2

Amounts included in the financial statements but not reported as revenue on Form 990.

Line 2a

Unrealized gains or losses from investments.

Line 2b

Value of donated services or donated use of property or facilities.

Line 2c

Funds recovered from grants given in earlier years.

Line 2d

Other adjustments (explain the details in Part XIII).

Line 2e

Total of lines 2a through 2d.

Line 3

Subtract line 2e from line 1.

Line 4

Amounts reported as revenue on Form 990 but not included in the audited financial statements.

Line 4a

Investment income included on Form 990 but not in the financial statements.

Line 4b

Other differences (described in Part XIII).

Line 4c

Total of lines 4a and 4b.

Line 5

Final total revenue after reconciliation (must match Form 990 total revenue).

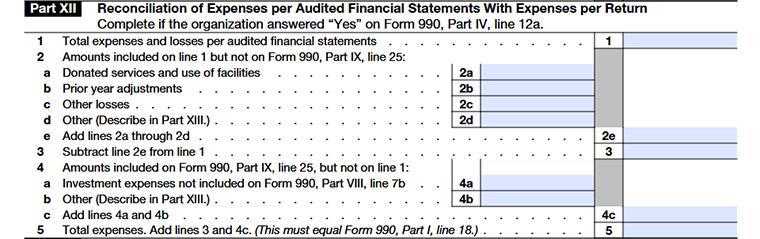

Part XII-Reconciliation of Expenses per Audited Financial Statements with Expenses per Return

Line 1

Total expenses and losses shown in the audited financial statements.

Line 2

Expenses included in the financial statements but not reported on Form 990.

Line 2a

Donated services or donated use of facilities.

Line 2b

Adjustments related to prior years.

Line 2c

Other expense differences.

Line 2d

Additional adjustments explained in Part XIII.

Line 2e

Total of lines 2a through 2d.

Line 3

Subtract line 2e from line 1.

Line 4

Expenses reported on Form 990 but not included in the financial statements.

Line 4a

Investment expenses reported on Form 990 but not in the audited statements.

Line 4b

Other differences (explain in Part XIII).

Line 4c

Total of lines 4a and 4b.

Line 5

Final total expenses after reconciliation (must match Form 990 total expenses).

Part XIII - Supplemental Information

Use Part XIII to give extra explanations or details requested in different parts of Schedule D, such as conservation easements, collections, escrow accounts, endowments, uncertain tax notes, and revenue or expense reconciliations. You can also use this section to clarify or add more information anywhere needed.

Choose TaxZerone to complete your Schedule D filing

Embrace the future of tax filing with TaxZerone, your IRS-authorized e-file service provider. At TaxZerone, we believe that e-filing should be simple, not stressful.

That's why we've designed our platform to be intuitive and user-friendly, guiding you through every step with unwavering support.

Here’s how your Form 990 return with Schedule D attachment is transmitted to the IRS - just 3 simple steps!

- Provide Organization Details - Choose the tax year for which you want to file a return, and provide your organization’s details.

- Preview the Return - Complete Schedule D and preview the information provided in the return for accuracy before transmitting.

- Transmit to the IRS - Transmit Schedule D and your 990 return to the IRS and get the acceptance in just a few hours.

We'll keep you in the loop with instant updates on your form’s filing status, ensuring a hassle-free experience from start to finish.

But that's not all. If the IRS rejects your 990 return, we'll help you rectify any errors and resubmit it without additional cost.

Ready to attach Schedule D along with your 990 return with TaxZerone?

Make the e-filing process simple by clicking the button below.

Commonly Asked Questions

1. What is the purpose of filing Schedule D?

2. What is a "donor-advised fund" in the context of Schedule D?

- That is separately identified by reference to contributions of a donor or donors,

- That is owned and controlled by a sponsoring organization, and

- For which the donor or donor advisor has or reasonably expects to have advisory privileges in the distribution or investment of amounts held in the donor-advised fund or account because of the donor's status as a donor.