Form 990 Schedule L

Introduction

Schedule L, a crucial component of the Form 990 /990-EZ return, serves as a disclosure form for non-profit organizations. It provides detailed information about transactions and arrangements between the organization and certain individuals or entities known as "interested persons."

In this resource guide, we aim to brief on Schedule L, providing valuable insights into its purpose, the entities obligated to file, the filing requirements, and addressing common queries.

Table of Contents

What is Schedule L?

Schedule L, Transactions With Interested Persons is a supplementary schedule that accompanies the standard Form 990/990-EZ and is filed annually by tax-exempt and nonprofit organizations.

This schedule aims to enhance transparency and accountability within the non-profit sector by providing detailed information on financial dealings between organizations and their affiliated parties.

Who must file Schedule L?

Non-profit organizations that file IRS Form 990 or IRS Form 990-EZ are generally required to complete Schedule L if they have engaged in any transactions or arrangements with interested persons during the tax year. This includes transactions such as loans, compensation payments, sales or purchases of assets, and leases.

Choose TaxZerone - Your Gateway to Seamless Tax Filing

Complete your exempt information return and Schedule L filing requirements with ease!

Schedule L Filing Requirements

All Section 501(c)(3) organizations that file Form 990/990-EZ must complete and attach Schedule L.

Below, we have provided Schedule N filing requirements for each part.

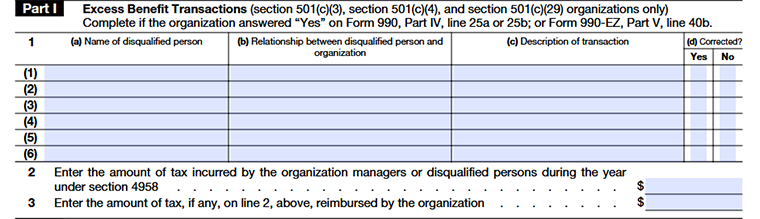

Part I - Excess Benefit Transactions

Line 1

For each excess benefit transaction with a 501(c)(3), 501(c)(4), or 501(c)(29) organization, provide the following:

Column (a)

Who got the benefit – List the disqualified person or say “substantial contributor” / “related to substantial contributor” to protect privacy.

Column (b)

Relationship- Describe how that person is connected to the organization (e.g., officer, family member).

Column (c)

Transaction - Explain what the excess benefit transaction was.

Column (d)

Correction- Say if the issue is fixed.

Line 2

Enter the total excise tax that disqualified persons or organization managers owe for the excess benefit transactions reported on Line 1, even if the IRS hasn’t assessed it yet (unless the tax was waived). This tax is reported and paid using Form 4720.

Line 3

Enter the amount of that tax that the organization reimbursed to the disqualified persons or managers, if any.

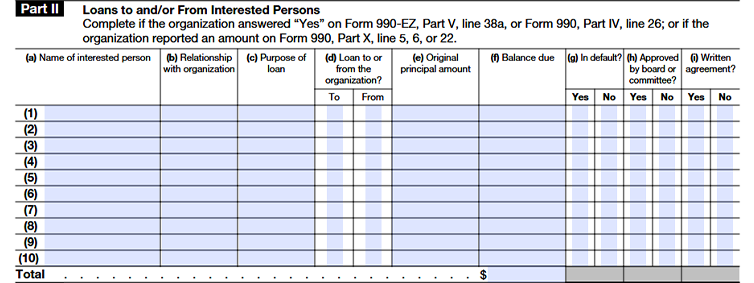

Part II - Loans to and/or From Interested Persons

Report any loans or advances between the organization and “interested persons” (like officers, directors, key employees, or substantial contributors) that are still outstanding at the end of the year. Each loan is reported separately. Certain common transactions (like normal pledges, ordinary employee pay, or loans on standard terms from banks or credit unions) are not reported.

Column (a)

Name of the interested person involved in the loan.

Column (b)

Relationship of that person to the organization.

Column (c)

Reason or purpose for the loan.

Column (d)

Shows whether the loan was given by the organization (To) or received by the organization (From).

Column (e)

Original loan amount.

Column (f)

The amount is still unpaid at the end of the tax year.

Column (g)

Whether any payment was overdue or the loan was in default.

Column (h)

Whether the board or governing body approved the loan.

Column (i)

Whether there is a signed written loan agreement or promissory note.

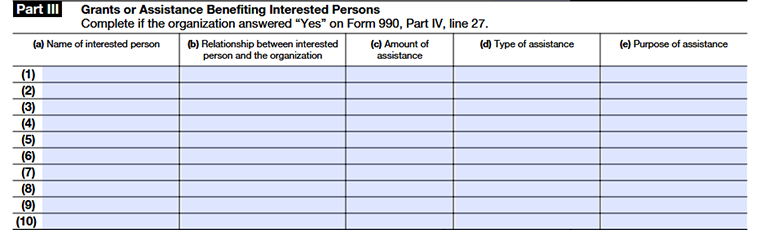

Part III - Grants or Assistance Benefiting Interested Persons

This part is used to report any grants, help, or benefits the organization gave to an interested person during the tax year. This includes things like scholarships, awards, discounts, internships, prizes, goods, services, or use of facilities no matter the amount.

(Some items like loans, compensation, or certain charity-wide assistance programs don’t need to be reported here.)

Column (a)

Name of the interested person who received the grant or assistance.

Column (b)

The relationship between that person to the organization.

Column (c)

Total value or dollar amount of assistance given during the year.

Column (d)

Type of help provided.

Column (e)

Reason or purpose for giving assistance.

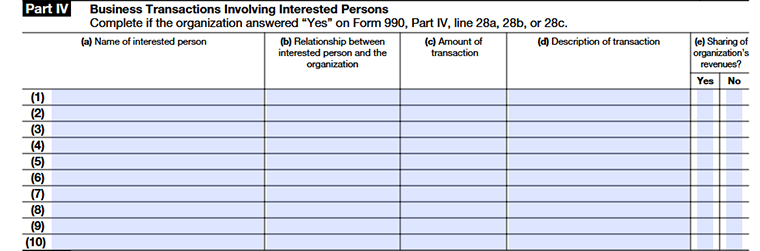

Part IV - Business Transactions Involving Interested Persons

This part is used to report business dealings between the organization and an interested person when the payments meet certain reporting limits. Generally, transactions must be reported if payments are large enough

Column (a)

Name of the interested person or entity involved in the business transaction.

Column (b)

Relationship of that person or entity to the organization (officer, director’s family member, key employee, 35%-owned entity, etc.).

Column (c)

Total amount paid or invested by the organization during the year (cash or fair market value).

Column (d)

Type of business transaction

Column (e)

Check “Yes” if payment was based on a percentage of the organization’s revenue (for example, a fee calculated as a share of income). Otherwise, check “No”.

Part V - Supplemental Information

This Part is used by organizations to explain or provide additional information regarding a transaction. Schedule L Part V can also be duplicated by the organization in need of additional space to report information.

Choose TaxZerone to complete your Schedule L filing

Embrace the future of tax filing with TaxZerone, your IRS-authorized e-file service provider. At TaxZerone, we believe that e-filing should be simple, not stressful.

That's why we've designed our platform to be intuitive and user-friendly, guiding you through every step with unwavering support.

Here's how your Form 990/990-EZ return with Schedule L attachment is transmitted to the IRS - just 3 simple steps!

- Provide Organization Details -Choose the tax year for which you want to file a return, and provide your organization's details.

- Preview the Return - Complete Schedule L and preview the information provided in the return for accuracy before transmitting.

- Transmit to the IRS - Transmit Schedule L along with your 990/990-EZ return to the IRS and get the acceptance in just a few hours.

We'll keep you in the loop with instant updates on your form's filing status, ensuring a hassle-free experience from start to finish.

But that's not all. In the unlikely event that the IRS rejects your exempt return, we'll help you rectify any errors and resubmit it without any additional cost.

Embrace the Future of Tax Filing – Choose TaxZerone Today!

Make your e-filing process simple by clicking the button below.

Commonly Asked Questions

1. What is the purpose of filing Schedule L?

2. What is an "interested person" in the context of Schedule L?

An interested person is an individual or entity that has a close relationship with the non-profit organization, such as officers, directors, major donors, or business entities controlled by such individuals.

3. What types of transactions must be reported on Schedule L?

A wide range of transactions with interested persons must be disclosed on Schedule L, including loans, compensation payments, sales or purchases of assets, leases, and any other transactions that exceed certain thresholds.